UK CPI Preview: With Sterling higher inflation fears wane as rate hike nears

- With post-Brexit Sterling depreciation effect on the UK inflation dissipating, the UK inflation is set to normalize at lower levels in 2018.

- The headline inflation in the UK is forecast to decelerate to 2.7% y/y in March.

- With inflation still way above the Bank of England target, the rate hike forecast becomes a sure shot on May 10, 2018.

The GBP/USD is trading near its 2018 high of 1.4377 that also represents the highest level of Sterling since post Brexit referendum slump and this is the reason why inflation in the UK is set to decelerate near-term.

The same rationale applies to the figures from the Office for National Statistics for consumer price index (CPI) in March. The headline CPI is expected to rise 0.3% over the month in March bringing the year-to-year comparison lower to 2.6%, down from 2.7% y/y in February and down from inflation’s cyclical peak of 3.1% y/y back in November last year. At the same time core inflation strip[ping the consumer basket of food and energy prices is expected to remain steady rising 2.4% over the year in March, just off the peak of 2.7% y/y rolling constantly since August to December of last year.

Of course, there is a number of other inflation indices in the ONS report including retail price index (RPI), producer price indices (PPI) on both input and output side as well as the house price index (HPI), but in terms of the monetary policy, they are irrelevant.

The Bank of England has tolerated higher inflation in the UK in the post-Brexit economic environment as sharp Sterling’s depreciation resulted in higher prices, especially for imported goods, but now it is ready to act on rates. The Bank of England lifted the Bank rate for the first time in last decade in November last year and it actually turned a bit more hawkish in February this year saying there might be more than just two Bank rate adjustments in next three years.

Related stories

The major source of uncertainty for the central bank remains post Brexit relationship of the UK with the European Union and with the trade deal extension to December 2020 fear of hard-landing threat eased so the Bank of England might be willing to accept the scenario of inflation gradually decelerating while tight labor market will result in solid wage increases generating more fundamentally justified reason for the monetary policy precautionary tightening.

So the nominal wage growth might temporarily disappoint the market expectations and result in Sterling being sold off against the US Dollar from its post Brexit high, but the long-term driver of inflation decelerating promoting the real, inflation-adjusted wages to rise and Sterling to appreciate as the scenario of 25 basis points Bank rate increase become the central expectation for the market almost a month before the May Inflation Report is due on May 10, 2018.

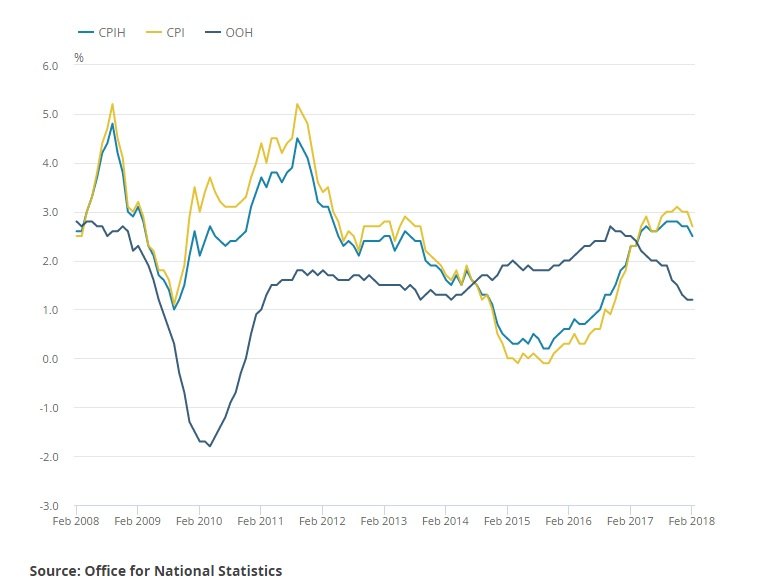

A decade of the UK inflation

Author

Mario Blascak, PhD

Independent Analyst

Dr. Mário Blaščák worked in professional finance and banking for 15 years before moving to journalism. While working for Austrian and German banks, he specialized in covering markets and macroeconomics.