Two reasons for the Fed to cut

Outlook:

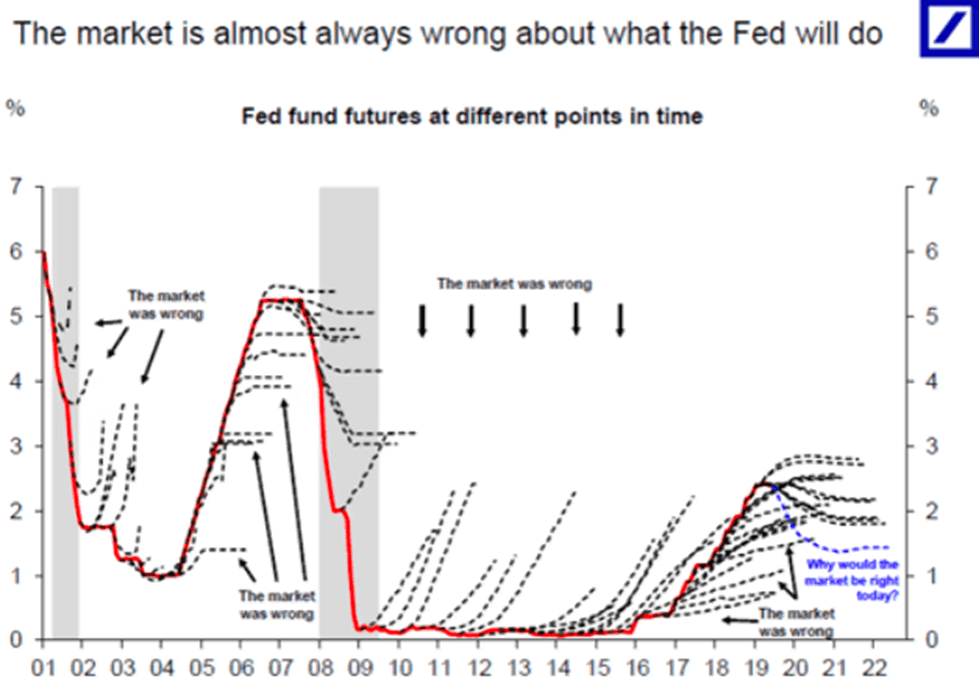

We get import/export prices today with the potential for another temper tantrum because the dollar is too strong. That gives us plenty of time to mull over the giant rift widening between the Fed rate cut camp vs. the no-cut camp. Deutsche Bank has now joined Goldman Sachs in predicting no rate cuts this year. The Wolf Report reports the Deutsche Bank analysis of the Fed funds market-- “The market is almost always wrong about what the Fed will do.” See the chart, via Bloomberg.

This time the nay-sayers are particularly annoyed at commentators talking about as many as three or four cuts on zero evidence the Fed has any intention or interest in cutting even once. They have a point, but it misses the nearly equally strong point that when Trump is calling the Fed names and saying it’s a destructive institution and wrong and stupid, a cut really is on the table whether the Fed likes it or not. And if the Fed does not deliver a cut in July or maybe September, what happens to the equity rally? The conventional answer is a rout, but in truth, the economy is not in bad shape and well inside normal ranges for everything, even if unemployment is a bit low and some measures are a little soft (ISM, MPI). In the absences of a screeching warning horn, maybe the equity boys can find something else to peg their rally on.

Bottom line, we don’t buy the doom-and-gloom scenario. That means the benchmark 10-year bond yield is too low and “should” recover. That can happen if the Fed is exceptionally clear next week at the FOMC on June 19. The Fed has a hard time being totally clear… it should say the door is open to the option of a cut but data does not yet support the need for a cut. That would be true and useful. A statement like that—July off the table but Sept still on—would go a long way to pushing recovery in the yield and dollar. Unless everyone else recovers, too—from negatives, mind you—the dollar should get over this latest push down.

Ah, but that would be the normal (i.e., non-Trump) set of circumstances and outcomes. And the probability is high that Trump is going to fire Powell unless Powell commits to a rate cut. They may quarrel over the date, but a cut is coming. If it’s July, Trump won. If it’s September, Powell won. We have no hard information they are bargaining, but it’s a logical deduction, presumably through an intermediary, maybe Kudlow. Larry can’t keep a secret so we will find out in his memoir a few years from now.

Besides, and this is the game-changer, Trump is almost certainly going to impose tariffs on the next $300 billion of Chinese imports. That has the potential to throw the US to recession or at least a big, fat slowdown, and the Fed has already named the tariffs as a critical uncertainty factor. Well, once it’s a certainty, doesn’t that mean the Fed needs to cut? Yes, and the question is “how preemptively?”

It’s a little funny—if the Fed were to cut next week preemptively on the assumption Trump will impose those tariffs, it would be unseemly and indicate the Fed thinks Trump is nuts. The same thing applies to July—after the June 26 G20 meeting at which Xi is supposed to kneel down and kiss Trump’s ring—if we don’t have tariffs then, can the Fed cut on the presumption of tariffs?

So, we have two reasons for the Fed to cut, and neither of them is the current economy—Trump will fire Powell if the Fed doesn’t cut and the tariffs will harm the future economy. That makes Goldman and Deutsche Bank wrong on the failure to grasp Trump’s inner nature—Disrupter-in-Chief (and Disregarder of Facts and Norms).

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a free trial, please write to [email protected] and you will be added to the mailing list..

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat