Trade war: There is a limit to how much bullying China will take

Outlook:

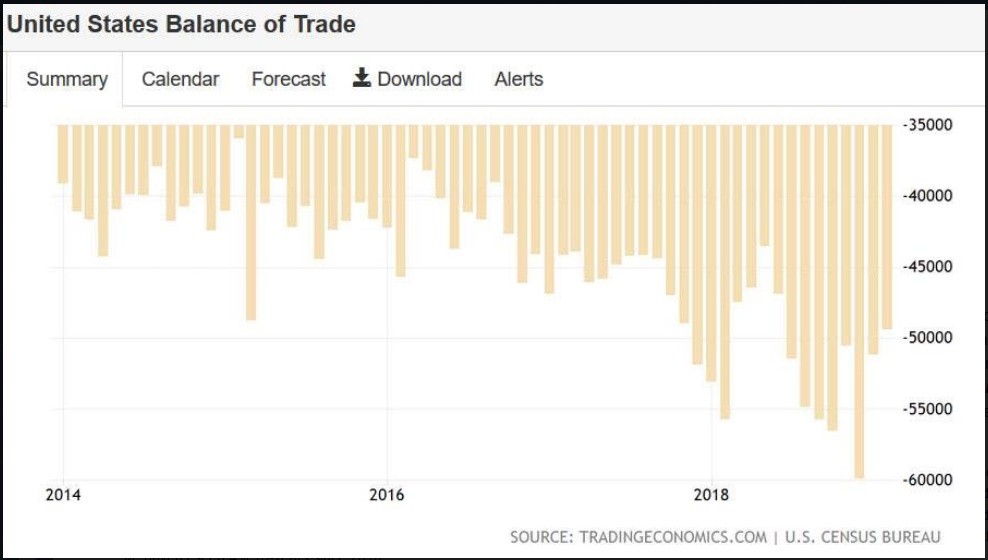

We get the trade balance on May 9 (tomorrow). The last release was $49.4 billion deficit for Feb, less than forecast, and the March forecast is a deficit of $50.1-50.2 billion. In other words, all the Trump noise and tariffs will not have delivered improvement—yet. It’s not clear Trump understands the numbers, anyway. He complains we are “losing $600-700 billion on trade” and losing “$500 billion to China,” but both numbers exaggerate. The US deficit with China was $419 billion in 2018, from $375 billion in 2017 and $347 billion in 2016. The chart shows the overall deficit… and it does show a worsening since Trump took office.

And as noted above, the cause of all this stock market misery, the US resuming the trade war with China, goes into drive tomorrow as talks resume. Many observers imagine the renewed US bully stance is only a negotiating ploy, but we think it’s more likely the inexperienced Trump team—refusing to take guidance from State Dept China hands—misjudged China. China considers itself a victim of past abuses by Western powers and Xi promises to make sure that doesn’t happen again. There is a limit to how much bullying China will take this time. The risk of China walking out is rising by the day. The Trump team think China needs the US, but using the most recent data we can find, Chinese exports to the US are 5.41% of GDP ($539.5 billion in exports divided into $12.24 trillion in GDP).

JP Morgan CEO Dimon stuck his oar in last night, telling Bloomberg he sees the odds of a deal at 80%. If not, global growth really does “go south.” Trump overstates in his tweets and then pulls back in real-time. Dimon was speaking on the sidelines of a JPMorgan’s annual China summit in Beijing. The odds of something bad have doubled. But he’d rather see no deal than a bad deal. Huh? In the end, his somewhat inconsistent remarks seem to add up to voting for delay. Bloomberg notes JP Morgan recently got approval for a majority stake in a securities venture. Separately, Dimon said yields at 4% would not be bad with growth at 2.5%. Bloomberg notes we haven’t seen 4% 10-years since 2010.

Never mind. Trump is not wrong that the US deficit is scary big and arises at least in part on others engaging in bad acts, like subsidies and dumping that drive domestic producers out of business, theft of intellectual property, and so on. Even the most traditional of political economists secretly enjoys the US telling the world “We’re mad as hell and not going to take it anymore.” (Go watch the movie “Network” again.)

Not that anyone respects or admires the way he is going about it.

Stock markets just about everywhere are is disarray and falling back on the prospect of the awful consequences of a full-bore trade war between the US and China. But it’s unreasoning panic and not a realistic forecast. Right off the bat, a full-bore trade war doesn’t serve the self-interest of Xi or Trump. Neither can afford to risk a recession. In the US, Trump needs to worry he will be aiming for re-election just as the recessionary effect from a trade war starts to hit. In China, the debt problem plus a trade war is not a political risk, but it sure is a management risk.

If Dimon is right that Trump is overstating the problems and exaggerating the true US response, he is also right that the hysterical stock market reaction is unwarranted. He doesn’t say the classic analysis is to buy just as things are looking their most dire, but claims to be unfazed by the global stock market rout.

The US has three choices. First, cut the 10% tariff back to zero, as China prefers. Probability—zero. Second, do not raise the tariffs from 10% to 25%. Probability--50/50. Third, raise the tariffs to 25% and promise to cvut them back to 10% after a year if China obeys US rules. Probability—51%.

China will have to commit to non-retaliation, which will only drive it underground. Maybe China will refuse to sell 5G to the US, cutting off its nose to spite its face and turning the situation upside down (Western countries banning Chinese 5G). We don’t really understand why China’s 5G is so much better than the American version—it extends over a bigger distance, for one thing, but why can’t we develop that? Anyway, whether it’s 5G or something else, you can bet China has plenty of non-tariff rabbits in its hat.

Here’s the problem: among developed countries, the biggest hit is not to the US, but rather to the EU and specifically Germany, which supplies China with machinery. China will, of course, lose exports to the US as competitors step in, but the substitution of machinery buying by (say) Viet Nam for buying by China will not fully compensate.

And here’s an off-the-wall idea—preferred conditions for US lenders in China. China has a debt problem, including a gigantic shadow banking system it struggles to contain. China can offer US banks and other financial institutions seeming benefits to substitute for rickety Chinese banks. Since all the big Chinese banks are state-owned, it will look like liberalization… but in fact it would be dumping bad paper on the newly licensed banks. US financial institutions won’t fall for it, of course; they know how to judge the credit-worthiness of borrowers. But to play in the Chinses banking field, they can be forced to hold some percentage of corporate loans and just pray they don’t go bad before they can package them up as some kind of derivative and sell them on. Just like the subprime mortgages in the US. Who is qualified to judge such a trade-off? TreasSec Mnuchin. And maybe Jamie Dimon, too.

Bottom line, Trump may be erratic and impulsive, but he needs the China trade deal to keep his promise to his base and besides, he knows which side of the bread his butter is on. China will outsmart the US in the end, of course, but in the meanwhile, the US has a chance to reduce that awful trade deficit.

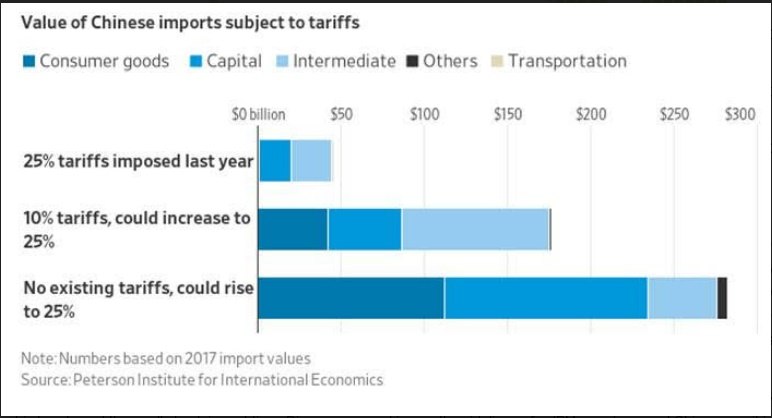

With any luck, we will know some of these answers by end of day Friday. In the meanwhile, we await US inflation and trade data, plus a few more comments by regional Feds, plus any fresh information on Brexit in the UK, plus developments in the US Constitutional Crisis. Our current scenario is a partial trade war solution that removes risk-aversion upward pressure on the dollar plus low inflation that will seem to support the dovish Fed outlook. An offset to the upcoming CPI data on Friday—one way to get inflation is to impose tariffs, which are paid by the consumer, not the exporter. See the chart from the WSJ. But that’s down the road. Before we see that effect, or more of that effect, inflation this week is likely tame.

The dollar “should” fall. But you can’t count on it.

Tidbit: On the political front, the important news is over 700 former Dept of Justice lawyers, including high-level prosecutors, all signed a letter contradicting Attorney General Barr, Trump and Senate leader McConnell (“it’s over”). The letter says that given the evidence in the Mueller report, each of them would prosecute the subject if he were not the president and protected by a Justice Dept rule. This is unprecedented. And the signatories are from both parties and accustomed to leaving their politics at the door, so it’s not partisan. Take that, Fat Donny. No wonder he is kicking up a storm to deflect attention.

Fun Tidbit: Trump can’t negotiate his way out of a paper bag. Former Citi loan officers were glad to rat out Trump (in private) as a pathetic loser during the 1980’s, and now we have a NYT story showing he lost so much money between 1985 to 1994--over $1 billion--he was able to avoid paying income taxes for eight of the 10 years. Moreover, the NYT reports, “The numbers show that in 1985, Mr. Trump reported losses of $46.1 million from his core businesses — largely casinos, hotels and retail space in apartment buildings. They continued to lose money every year, totaling $1.17 billion in losses for the decade.

“In fact, year after year, Mr. Trump appears to have lost more money than nearly any other individual American taxpayer, The Times found when it compared his results with detailed information the I.R.S. compiles on an annual sampling of high-income earners. His core business losses in 1990 and 1991 — more than $250 million each year — were more than double those of the nearest taxpayers in the I.R.S. information for those years.” In addition, in the following year 1995, “The New York Times previously found that Mr. Trump declared an adjusted gross income in 1995 of negative $915.7 million.”

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a free trial, please write to [email protected] and you will be added to the mailing list..

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat