This is a week for central banks

Outlook: This is a week for central banks, starting with the Fed on Wednesday and the SNB and BoE on Thursday. The Fed and BoE were each expected to do 25 bp and the SNB has signaled 50 bp, but all that was before the Credit Suisse crisis. The FT notes there is discussion about the BoE perhaps pausing. About the SNB, one opinion has it that the lender-of-last-resort role is fundamentally different from monetary policy aimed at the business cycle, so the SNB will go ahead with the 50 bp.

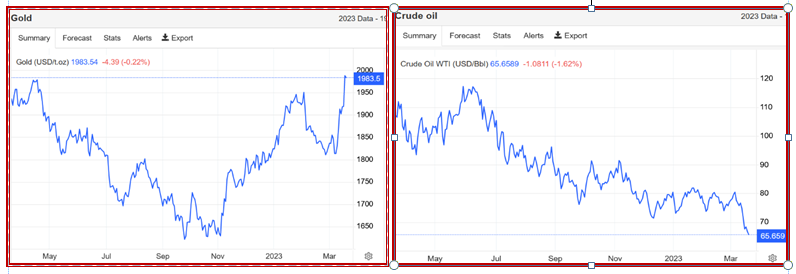

We know the crisis isn’t over because gold rose to over $2000, if backing off a bit now but still very close to $2000. This is an indicator from the last century but aside from the US 10-year, what else do we have in one place? Oil is similar but in the opposite direction, with Brent down over 38% y/y and WTI under $65.

A top asset manager at JPMorgan says it’s too soon to see the ending. The perspicacious Yardeni says the banking turmoil may cause a recession if it sets off a credit crunch (Bloomberg). As noted above, opinion is divided on whether the Fed goes ahead with 25 bp this week (signaling no anxiety/panic is called for) or pause until the dust settles. Note that the crisis was not due to banks making bad loans, but rather having invested in assets that lost mark-to-market value as central banks raised rates—not true value.

The Economist writes that the Fed has a dilemma—keep fighting inflation or seek financial market stability. Pausing this week instead of hiking has a sound base—it was higher rates that caused Silicon Valley to fail because it had not hedged properly. But lots of other firms, and not just banks, have notional mark-to-market losses than yet another hike will worsen. Besides, “instability is itself a drag on the economy. As confidence cracks, firms try to preserve capital. Banks lend less and investors pull back. Measures of financial conditions—which include interest rates, credit spreads and stock values—have tightened sharply in the past ten days. Eric Rosengren, a former president of the Fed’s Boston branch, has compared it to the aftermath of an earthquake. Before resuming normal life, it is prudent to see whether there are aftershocks and buildings are structurally sound. A similar logic applies to monetary policy after a financial shock. ‘Go slow, check for other problems,’ Mr Rosengren cautioned.”

But the Fed should already know who is sound and who is not. “A rate rise would also demonstrate that the Fed can chew gum and walk at the same time. In an ideal world officials should be able to manage financial stability while keeping inflation in check. With a combination of deposit guarantees, a new liquidity facility and support from bigger banks, a framework is now in place to shore up America’s financial institutions.”

Some exaggerate the banking crisis into something Historic and others say is just a blip: from somewhere in the mists of time has come the idea that the duration of the crisis itself is only about three weeks, and all the rest is fallout. The majority of the action occurs in the first 10 days and the slowpokes catch up during the next 10 days. Then it’s all over except the shouting. We have doubts.

This was not the case with the slower-moving subprime crisis that started in 2006 with the collapse of some lenders and hit a peak in Sept 2008 with the failure of Lehman. But still, if TreasSec Yellen is right that the US financial system is stable and not “fragile,” three weeks seems about right, at least for the stock market to get steadier on its feet. One mitigating factor—the size of the current bailouts and bankruptcies should not be used for the “historic” designation. Yes, the sizes are bigger but so is the economy (and the population, money supply, lending, etc.).

The status as of Saturday, according to Bloomberg: “Silicon Valley Bank died quickly, filing for bankruptcy, though it turned out that regulatory concern about the bank went back more than a year. After officials shuttered New York’s Signature Bank, worry that San Francisco-based First Republic was also on the verge of collapse prompted JPMorgan, Citigroup and others to inject $30 billion in deposits to quell investor panic.

“… US banks borrowed a combined $164.8 billion from two Federal Reserve backstop facilities over the span of one week—breaking a record from 2008 and the financial crisis. US Treasury Secretary Janet Yellen sought to reassure Congress, testifying that the banking system remains sound. But John Authers writes in Bloomberg Opinion that, with the era of easy money over, ‘anything that relied on low interest rates should fall into question, and that implies issues for the sprawling fields of private equity and private debt.’ The real question now, he says, is what the next crisis will be.” One idea, a long time coming, is commercial real estate.

There are two issues that could prolong the crisis long past the hypothetical three weeks. The first is that of the 14,000+ banks in the US, some 200+ are under investigation for bad management, especially for exactly the same thing that brought down Silicon Valley—holding T notes and bonds that are perfectly safe and will return full face value—but not until they mature, and before then, have to be marked down now that the Fed has raised interest rates. Rates up, prices down. Or the banks can swap Treasuries for cash with sister banks, or even swap depositors.

Then there is a basic distrust of the banking sector among the public. It’s not the Average Joe moving his checking account to JPMorgan, but even so, we can probably project the same mistrust of the public to the “financially literate.” See the chart. Gallup finds that less than 30% of those polled trust banks. According to 538.com, “And a slightly different but complementary question from Gallup shows Americans not only lack confidence in banks but also tend to have an unfavorable view of them: In a 2022 survey, just 36 percent of Americans said they had a very or somewhat positive view of the banking industry, down from 40 percent the year before. Compare that to the 60 percent of Americans who have a positive view of the restaurant industry, or 57 percent who have a positive view of the farming industry.

“It’s perhaps no surprise, then, that many Americans feel banks ought to be more regulated. A survey from Lake Research Partners/Chesapeake Beach Consulting last October asked Americans about bank regulation and specific policies, finding widespread support across the political spectrum. Sixty-six percent of Americans, including 77 percent of Democrats and 57 percent of Republicans, said there should be more regulation of ‘financial companies such as Wall Street banks, mortgage lenders, payday lenders, debt collectors and credit card companies.’ Over half of Americans said the influence of big banks in Washington is too high.” [No kidding.]

We may or may not be okay in the US, depending on whether any other shocks come along. But given the resolve of the feds to keep the wolf from the door, we are willing to feel optimistic. We are not so sure about other countries. Look at how long it took the Swiss to get Credit Suisse into safer hands at UBS—and the Swiss certainly know what they are doing and certainly know as much about banking as anyone on the planet. What about other big countries that lack transparency, have corrupt/incompetent regulators, and insufficient resolve? We can imagine bank runs (and frantic calls to the IMF) from any number of countries. Does that then circle back to the US and become “contagion”?

As noted here before, academics try to study financial contagion and as far as we can tell, have learned very little except to prevent it, strong action is required at the first sight. Once it gets going, like a real virus, it behaves just like a pandemic. One important question is whether the capital adequacy ratios are reasonable. This is a murky subject and one that is about to get attention. Basel says 8% is good enough. The US has 14.7%, the UK, 22.1% (it remembers Northern Trust), Japan, 15.72% and India, 9% for private and 12% for public banks.

And capital adequacy is not even listed among the top five bank ratios, which include net interest margin, loan-to-assets ratio and return-on-assets, and that’s not even mentioning the Big One, liquidity. Liquidity depends entirely on trust among peers and central banks as the last resort. Bottom line, none of us is equipped to judge whether the global banking system is safe from contagion, and central bankers and finance ministers everywhere are sweating bullets. According to Market Watch on Sunday night, the Fed has contacted the top five foreign central bankers to promise whatever dollar-funding they might need.

Forecast: We suspect that a global panic will be averted, but admit that might be wishful thinking. We also think the Fed will go ahead with the expected 25 bp this week, despite worrying about disagreeing with Goldman. To pause would be to admit there is still a banking crisis. The CME FedWatch tool shows 35.8% see the pause but 64.2% expect the 25 bp (as of 7:40 am ET). This changes almost by the minute, so dose of salt.

Bank Failure Tidbits: After Silicon Valley Bank CEO Becker lost his job over last weekend (although it’s not clear who fired him—one report says Biden himself but more likely, the FDIC), on Monday he and his wife flew first-class to Hawaii where they have a fancy, expensive house on the beach. We await news on the government clawing back bonuses Becker paid himself.

Banks have backstops and now lifelines, but hedge funds are unencumbered by any such thing. Bloomberg reports a fund named “Graticule, based in Singapore, becomes the first known high-profile hedge fund felled by wild swings in bond markets, which were triggered by the SVB’s collapse as traders pulled bets on further rate hikes by central banks. Some of the biggest hedge fund winners of last year from computer-driven hedge funds to money pools run by Rokos Capital Management, Graham Capital Management and Brevan Howard Asset Management have also seen losses.”

A third idea—that we can’t fact-check—has it that over thirty private jets landed at Omaha last Thursday and Friday, where Buffett lives. Really? Bloomberg reports the White House and Buffet are in talks, presumably about whether he would buy up a few banks.

About the FDIC: In a Politico article saying Roosevelt would have hated the current institutional response to the banking crisis, including the dithering.

There are only about 200 U.S. banks that are clearly vulnerable because of securities losses similar to those of Silicon Valley Bank. Regulators should have met with those banks individually last weekend, required them either to immediately come up with credible recapitalization commitments, or put them into conservatorship (beginning Monday morning). In conservatorship, they would have had limits placed on their activities until it was determined whether they could offer adequate recapitalization, or, if not, be placed in receivership. In the meantime, they could have been allowed to pay out all insured deposits, but only to pay out a fraction of uninsured deposits (based on the potential losses of uninsured depositors at each bank). This would have put pressure on those banks to resolve the problem quickly, and would have limited the illiquidity problem to a portion of the uninsured deposits at a small number of banks.

US Politics: It seems likely that Trump will be arrested and arraigned early this week (and released before trial) on charges of false business accounting and intent to defraud in the stripper hush money case (for which an associated person was already convicted and served time). A number of side issues are important, not least that the prosecutor will get death threats from the deranged Trump cultists and Trump will ramp up calls for street protests involving violence.

On the Smerconish TV show, the least likable Trump lackey, John Bolton, said that if the prosecutor fails to convict, we will get another four years of Trump. Adherents will say the failure proves it was a witch hunt. About Jan 6, Bolton said it was a riot, not an insurrection. “Trump doesn’t have the wits to conduct a coup.”

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat