This is a big data week

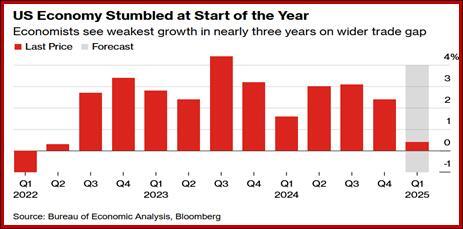

This is a big data week, with Q1 GBP at midweek plus the employment cost data. The Atlanta Fed bravely delivers its GDPNow ahead of the official data, on Tuesday. Last week it was -2.5%, but adjusted for gold, -0.4%. A minus either way. Some have positives—Bloomberg has +0.4%, the weakest in three years. The PCE deflator will not surprise, likely at 2.2% from 2.5%.and core to 2.5% from 2.8%. Then it’s payrolls on Friday, with a consensus estimate of 130.000. If unemployment remains the same 4.2%, yawn.

Note that we also get GDP and CPI for Germany on Wednesday. And late Wednesday night (in the US) it’s the Bank of Japan rate decision. Since last week’s March inflation is 2.6% (core, 2.4%), a hike has long been expected. But does it attract more capital home?

Note that Thursday is the International Workers holiday and markets in all of Europe (including London) are closed. It’s also a holiday in India.

The US does not yet show signs of stagflation distress. But since everyone from Nobel economists to the Average Joe expects stagflation, we need to worry about a self-fulfilling prophecy. You can bet the Fed is thinking about that very thing.

The near-universal forecast of stagflation shows up in the polls described above. Trump cares about polls, whatever his lackeys say on TV. Fox News writes he is trying to find a way to “climb down” from the Chinese tariffs. This is a phrase toned down for its audience in place of “de-escalation” used elsewhere (which we think is funny).

Assuming Trump finds a way to de-escalate, how much energy does it sap from the sell-dollars movement? Some, but not enough. He withdrew from the firing-Powell incident but many suspect it will arise again. .

Yale’s Stephen Roach has a scary essay about how the Covid supply chain inflation looks “almost quaint” compared to what Trump is going to deliver if the trajectory remains the same. It took 2 years to recover from that one but recover we did [and better than any other country]. This time “a more worrisome form of stagflation is in the offing, threatening severe and lasting consequences for the global economy and world financial markets.”

Forecast

Short-run, the dollar can correct to the upside. Long-run, it’s still toast.

We can’t call what we see today is a “relief rally” because it’s not a rally at all. We guess it’s a semi-relief rally because there’s just so much stress and anxiety traders can take. There’s also institutional limits on short dollar positions. And don’t forget the AI machinery that is confused now and can’t make a breakout decision.

Any tiny ray of light suffices to trigger a reversal. Or what seems like a reversal. You don’t want to be the greater fool who buys at the very top, so it’s still a good idea to identify and name a relief rally for what it is—a temporary thing that can persist only if there is a true, underlying reason for it to last.

This can be the demise of the previous cause of a crash, but it absolutely, positively needs to be True. We saw a relief rally in the pound after Brexit, but it was short-lived because all the doom-and-gloom about the consequences of Brexit were valid.

The Trump tariff war is a perfect example. Many traders seem to be expecting relief from Trump on auto parts or even China this week. On Friday the China talks Lie saw the Asian and European sessions willing to buy dollars on the story. But not the US session! And as of this morning, it’s clear we have to believe Trump or Xi, and the market is choosing Xi.

It is not out of the question that US data moves the dollar down or a new Trump action drives it up. Trump wants a weak dollar and the stock market is okay, sort of, so only the polls and the endless quest for the spotlight would be the motivator for Trump to do something Big. (About the spotlight: the press noted that everyone at the Pope’s funeral wore the traditional black except Trump, who wore blue in order to stand out. He also got a front row seat because the seating was by country in French, and in French, the US is “Etats.” So his seat was better than British royalty--United Kingdom.)

The short-term dollar recovery narrative also gets some traction in the form of Trump exhaustion. Brent Donnelly makes the amusing but true connection between the most negative Economist covers and the subsequent rise in the Nasdaq. This is different from a relief rally because it can be more long-lasting. It’s going to take several months before we see hard data demonstrating stagflation. Before then the markets can reject the worst of the worst narrative as overdone and not proved.

This leads to a two-part forecast: first a possible but short-lived correction in favor of the dollar. Then a return to the primary trend sloping downward. But perhaps a longer-lasting correction until something comes along in line with the Trump performance so far and sets off the fire alarm again.

Bottom line: it’s not just the tariffs. It’s also Trump thumbing his nose at the courts and Constitution, kidnapping foreigners off the streets and saying he can send even US citizens to a foreign gulag, damaging the federal government willy-nilly, and saying stupid things like tariffs are raising so much money they would cover a tax cut (they don’t). So even if Trump pulls in his horns on some tariffs this week or even starts talks with China, it’s not enough to remove the stink from the dollar.

Tidbit: How much can the dollar lose as the numeraire and global reserve currency before it no longer delivers to the US the extraordinary privilege that so powerfully allows cheaper borrowing?

According to The Economist, the dollar has lost 7% of its share of central bank reserves during Q1 2007 to Q4 2024. Its share now is 57.8% You have to wonder why the magazine picked a 17-year timespan to measure, but never mind. The biggest gainer is the yen, now 5.8% of the total, and the next biggest gainer is the Chinese yuan. The rest are as you would expect—GBP, CAD, AUD, euro, Swiss Franc.

We are not sure this passes the “so what?” test. It’s a process long in the making. The real issue is not the falling share of world reserves, but the falling reputation of the US and the dollar. Because of the economy’s size, asset variety, etc., some will have to hold their nose and buy US Treasuries whether they like it or not. That’s unless and until Trump does something even more stupid, like selective default (on China, presumably) or a Mar-s-Lago Accord that not a single other country will agree to. Then the exodus will accelerate.

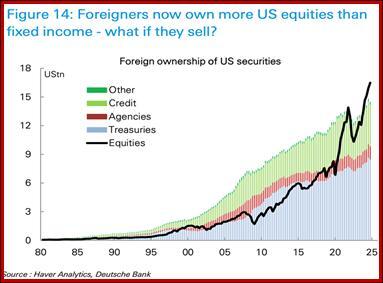

In other words, the potential beginning of a crisis but not yet a true Crisis. Heisenberg brings up a killer chart from Deutsche Bank—foreign ownership of US equities is even bigger than of Treasuries. This is scary if we ignore that many managers have a mandate to maintain a proportion of their portfolios commensurate with world shares. In other words, they can hedge but they cannot sell.

Even so, the dollar is still at tremendous risk of losing it all. And the outcome depends on a single guy who is “compromised, contemptible, dim-witted or all three. Insult to injury is the administration's programmatic effort to consolidate power in an autocratic executive that runs roughshod over the rule of law…” (Heisenberg). To expect Trump to change is silly. Tigers and stripes.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat