The US won't default on $39 trillion debt: Why financial repression is coming and Gold is the only hedge

As the US national debt surges past $39 trillion, policymakers face an unsustainable economic trajectory that threatens the global financial system. With a formal default out of the question and fiscal austerity politically unfeasible, the US government is increasingly likely to rely on financial repression, artificially keeping interest rates below inflation to erode the real value of its debt.

This macroeconomic shift could trigger one of the biggest wealth transfers in history, structurally positioning Gold as a primary beneficiary and an essential policy hedge for investors.

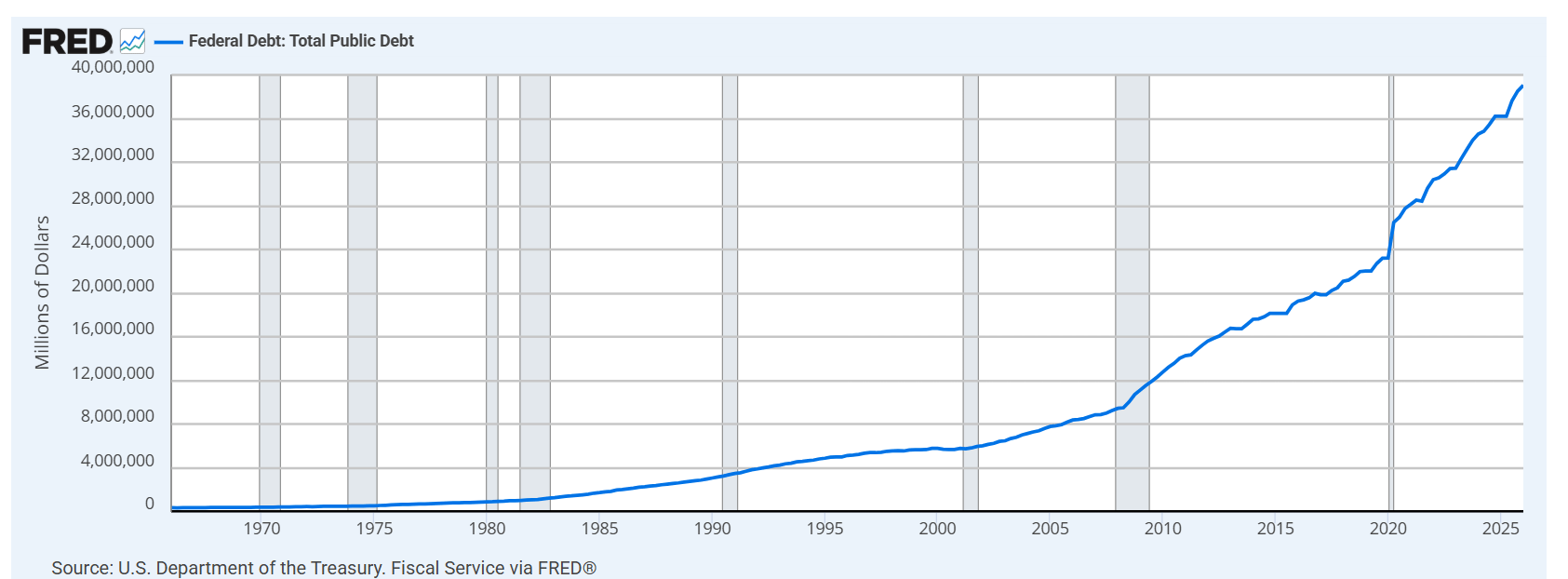

The scale of the $39 trillion problem

The US Federal Debt historical chart reached a staggering $39 trillion in Q1 2026. Debt has gone parabolic over the last two decades; 20 years ago, US government debt was just above $8 trillion. In two decades, it has almost quintupled, skyrocketing particularly after COVID-19.

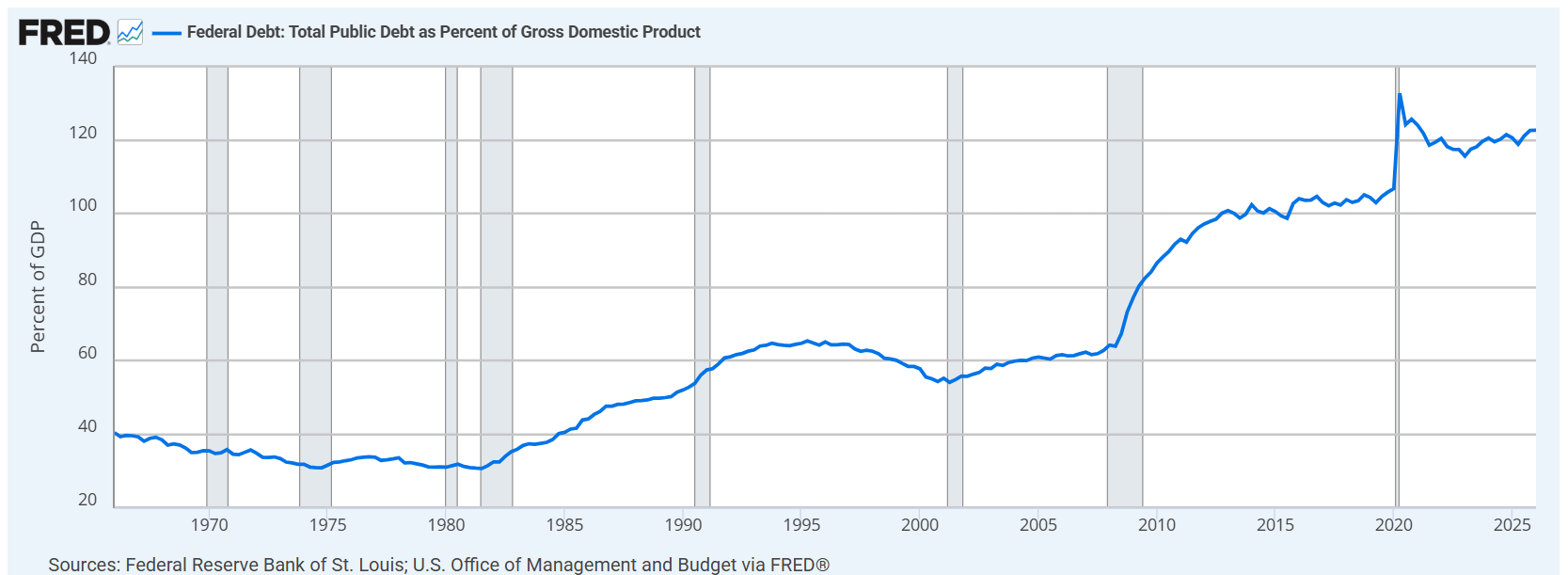

However, looking at the nominal number is incomplete without comparing the US Federal Debt to GDP, where it currently sits above 120%. This means the money the US government owes is larger than everything the world’s largest economy produces in a single year.

The trend keeps getting higher, and it is entirely unsustainable. At some point, policymakers in Washington, DC, whether US Treasury Secretary Scott Bessent, new Fed Chair Kevin Warsh, or both acting in a coordinated effort, will have to fix this. In fact, they might already be working on it behind closed doors.

The three choices facing Washington

There are only three ways to fix a public debt problem:

- Option one: Default. This is not happening. The United States can print the currency in which its debt is issued, and a formal default would blow up the entire global financial system.

- Option two: Fiscal austerity. This requires slashing spending and raising taxes to run large primary surpluses for years. While it is the fiscally responsible path, it is politically unviable. No politician wants to cut social services, trim defense, and hike taxes within an everlasting election cycle that can get them voted out of office in a very short time.

- Option three: Financial repression. This is the scenario investors must focus on. If this is the path the US chooses, it could quietly become one of the most important macro themes of the next decade.

Financial repression doesn’t just change the US government debt dynamics; it fundamentally changes which assets win, which ones lose, and how you should position your portfolio.

Understanding financial repression

The US public debt stock has skyrocketed and shows no signs of stopping: interest costs are growing, making the problem bigger, and the political system has almost no appetite for real fiscal discipline.

But this is not isolated to America. The World Economic Forum notes that global public debt has topped $100 trillion, which is roughly 93% of global GDP. Meanwhile, governments around the world face a fiscal trilemma: the need to spend more on security due to the rise in armed conflicts, aging populations, and growing climate-change needs.

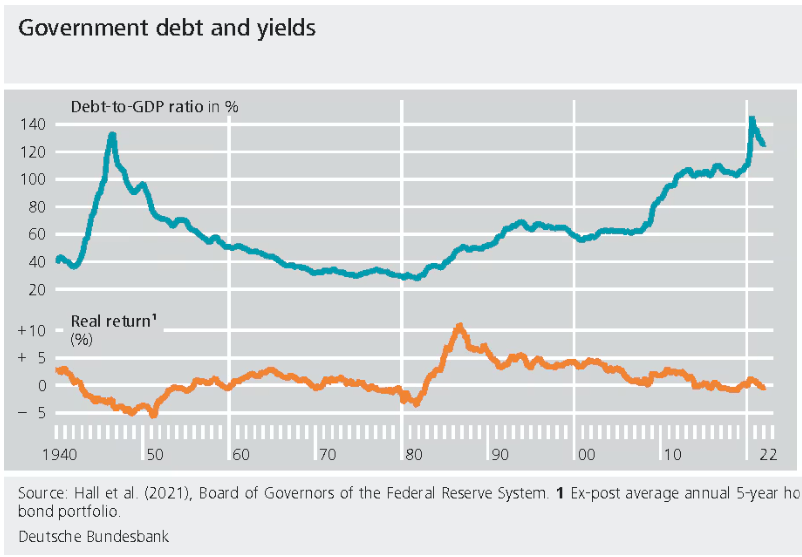

To understand how to tackle this without crashing growth or triggering voter backlash, we can look at history. The US already has experience in financial repression, specifically during the years after World War II. The Allied victory didn’t come without a cost; after 1945, the US federal debt-to-GDP ratio peaked above 100%, approaching the levels we see today. Yet, by 1974, that ratio had fallen to 24%.

To achieve this, the US government inflated its way out of the debt burden. They kept nominal GDP growth alive, capped interest rates, forced banks to buy US government bonds, and let inflation do part of the debt-reduction work. That is the core of financial repression: a slow-motion transfer of wealth from savers to the sovereign.

The mechanism itself is simple: if you keep interest rates below inflation for long enough, the real value of government debt shrinks over time.

Consider the components of GDP: inflation (price levels) and growth (total output). If both rise, GDP growth accelerates. On the other side of the formula, debt is influenced by the principal and the interest rate paid to service it. If nominal GDP rises because of inflation and growth, but the government’s funding costs stay artificially suppressed, the debt-to-GDP ratio can fall even if the nominal debt stock keeps rising.

The government doesn’t need to "pay off" $39 trillion the way a household pays off a mortgage; it just needs to make that debt smaller relative to the size of the economy. The easiest way to do that is to inflate the denominator while keeping the cost of debt under control.

The modern playbook for debt dilution

Historically, policymakers have chosen inflation over fiscal pain, and they may do so again in a subtler, more modern form. Financial repression to dilute massive government debt requires four key elements:

- Inflation is running above target for longer.

- Real rates are kept too low for too long.

- Pressure to maintain orderly government bond markets.

- Policy choices that quietly favor debt sustainability over savers’ purchasing power.

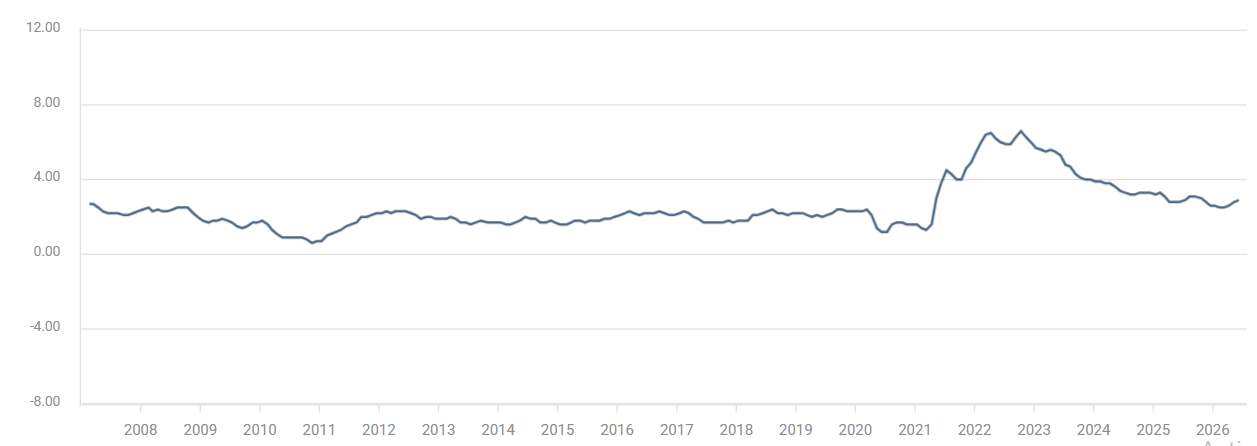

The first element has already been playing out. The last time the US Core CPI printed a figure below the Federal Reserve’s 2% target was in April 2021, marking more than five years of high inflation.

The second element, keeping rates low, has been front and center of political priorities. Donald Trump previously placed significant political pressure on the Fed to lower interest rates even when inflation was running well above the 2% target.

Trump's newly nominated Fed boss, Kevin Warsh, has emphasized Federal Reserve independence and prioritized inflation in his first public appearances, but his under-the-radar policy ideas tell a different story. Warsh’s intent to reduce forward guidance and shift inflation measures from headline figures to more obscure, trimmed-mean indicators might ultimately give the Fed the flexibility to lower rates.

The final elements involve suppressing yields. After falling for thirty years, US 10-year Treasury yields have been rising since the pandemic, substantially increasing the government's borrowing costs. The US government needs yields to go down, meaning it needs demand for US Treasuries to go up.

To achieve this when the market is moving away from sovereign bonds, policymakers may look to past playbooks: forcing banks to hold US Treasuries by law, similar to the Banking Act of 1933 or the post-WWII Fed-Treasury accords. Kevin Warsh at the Fed and Scott Bessent at the Treasury hold the keys to enacting this regime.

Why Gold becomes the ultimate hedge

Financial repression is bad news for anyone holding assets that cannot outrun inflation. If inflation runs at 4% but your cash earns 2%, you lose purchasing power every year. If you own long-duration bonds and yields are capped while inflation stays sticky, your real return gets crushed. This is the hidden tax that dilutes bank balances and bond yields, transferring wealth from savers to borrowers and from cash holders to governments.

Conversely, Gold tends to perform best when real yields are falling, confidence in fiat policy deteriorates, or investors want protection from monetary debasement. If the government artificially suppresses borrowing costs while allowing inflation to run, real interest rates remain negative, an environment that is structurally supportive of Gold.

In a repressive regime, Gold becomes a hedge against three things simultaneously:

- Inflation eroding purchasing power.

- Central banks are tolerating negative real returns.

- The long-term credibility risk of using a currency as a debt-management tool.

This doesn’t mean Gold moves upward in a straight line. Following a historic, unprecedented rally, the bright metal experienced a sharp correction from $5,500 to below $4,000.

In the short term, Gold will still trade on Fed expectations, the US Dollar, yields, and market positioning. But structurally, if the policy mix shifts toward inflating away debt, Gold transitions from a tactical trade to a critical policy hedge.

Five macroeconomic signals traders must watch

To identify if this thesis is actively playing out in real time, traders should monitor five key signals:

- Real yields: If inflation stays sticky but nominal yields stop rising fast enough to compensate investors, the risk of repression increases.

- Fed language on inflation: Look for signs that policymakers are tolerating above-target inflation for longer periods while shifting their focus to economic growth or debt stability.

- Treasury market policy: Watch for any implementation of yield suppression, heavy balance-sheet support, or political pressure to contain funding costs.

- Fiscal trajectory: If deficits remain massive and there is no credible political appetite for spending austerity, the incentive for financial repression grows stronger.

- Gold relative to bonds: If Gold starts to outperform fixed income while real returns on bonds deteriorate, the market is actively discounting an early repression regime.

The bottom line is clear. The US government will not choose to default, nor will it endure the extreme fiscal pain required to genuinely repay $39 trillion in debt. This leaves financial repression as the most politically convenient option, a world where inflation dilutes the debt burden, rates are kept artificially low, and savers bear the brunt. If this is the path ahead, it shifts from a simple debt story to a critical asset allocation story, and Gold remains one of the clearest winners.

(This article was created with the help of an Artificial Intelligence tool and reviewed by an editor. Know more.)

Author

Dhwani Mehta

FXStreet

Residing in Mumbai (India), Dhwani is a Senior Analyst and Manager of the Asian session at FXStreet. She has over 10 years of experience in analyzing and covering the global financial markets, with specialization in Forex and commodities markets.