The boom daily: Barrels, bandwidth and the battle for supply

Oil market daily: Hormuz still matters, but the pipeline hedge is coming

Goldman Sachs’ latest commodities research, Gulf Exports: Short-Term Uncertainty, Long-Term Pipeline Hedge, draws an important line between the oil market’s immediate exposure to the Strait of Hormuz and the region’s longer-term effort to reduce that vulnerability.

The recent rally in crude, driven by tanker attacks and renewed US–Iran strikes, shows that Hormuz still commands the front of the oil curve. The market does not need to see a full physical shutdown before adding a risk premium. Attacks on vessels, rising insurance costs, disrupted shipping and the threat of military escalation are enough to push prices higher because roughly 23 million barrels per day of pre-war exports from seven Persian Gulf producers remain tied to the Strait.

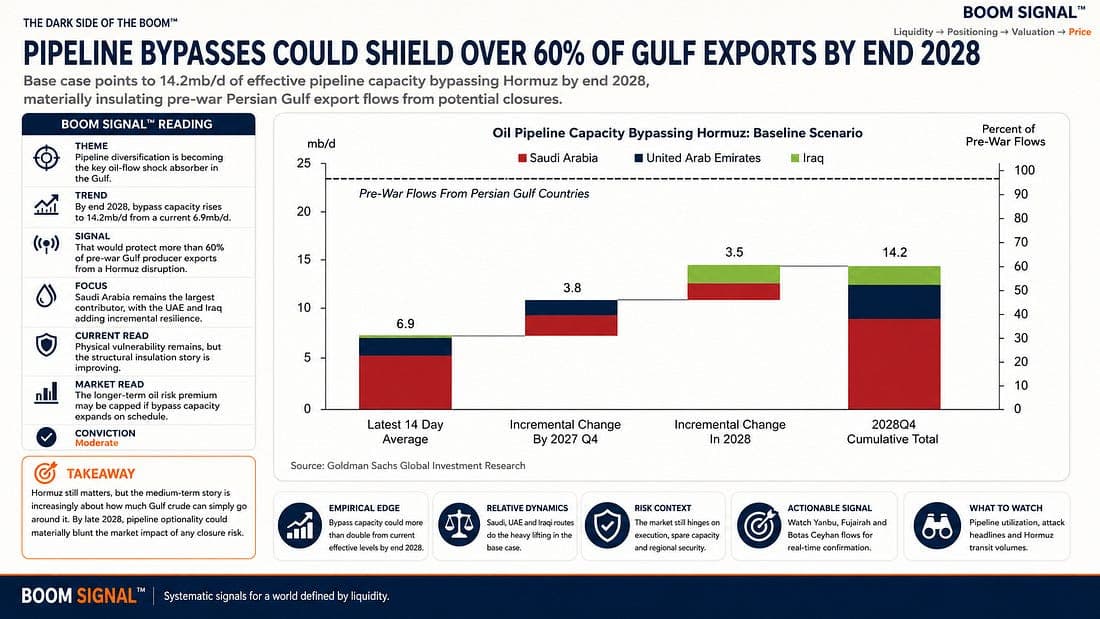

Goldman Sachs argues, however, that this dependence could fall sharply over the next two years. In its base case, effective pipeline capacity bypassing Hormuz rises by another 3.8 million barrels per day by the end of 2027 and by a cumulative 7.3 million barrels per day by the end of 2028.

That would lift total effective bypass capacity above 14 million barrels per day, enough to insulate more than 60% of pre-war export volumes from Saudi Arabia, Kuwait, Iraq, Qatar, Bahrain, the UAE and Iran.

The timetable is not as unrealistic as it may first appear. Goldman Sachs examined nine major regional pipelines and found a median construction period of roughly two and a half years. Projects were often completed more quickly when war, sanctions or supply disruptions turned export security into a strategic necessity.

That history matters now. Governments may move slowly when infrastructure is merely desirable, but they tend to move faster when the alternative is leaving national exports exposed to a single maritime choke point.

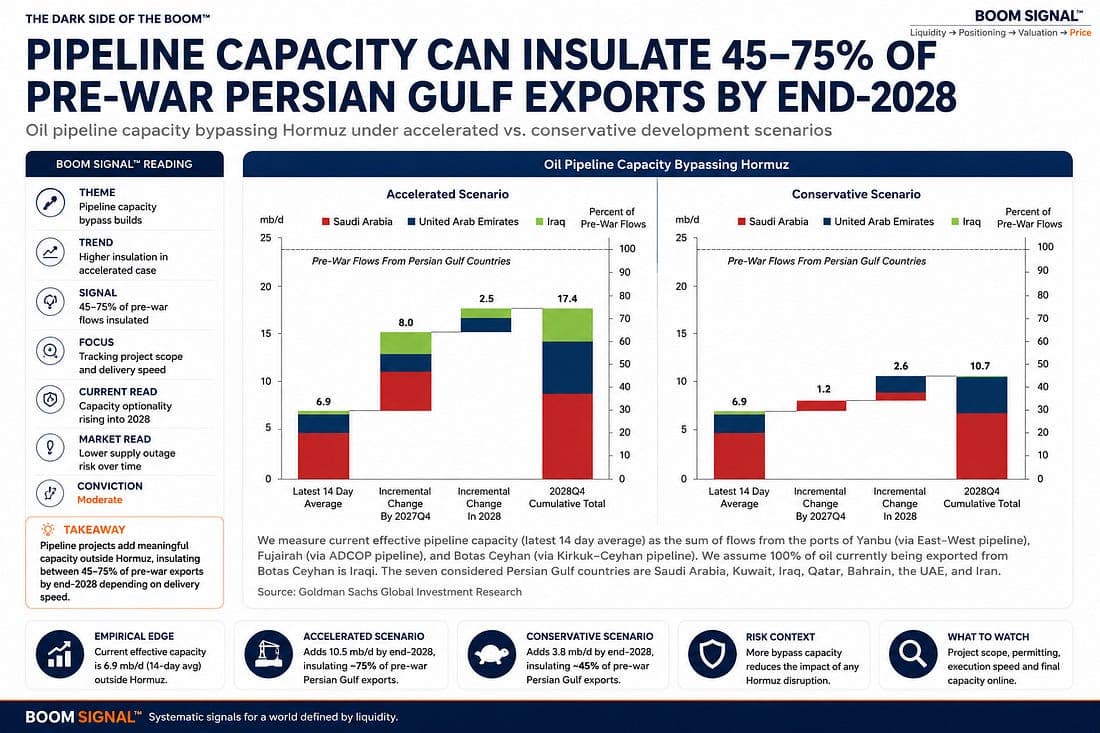

The range of outcomes remains wide. Goldman Sachs estimates that an accelerated buildout could insulate around 75% of pre-war Gulf exports by the end of 2028. A more conservative path would still protect slightly more than 45%.

For traders, the implication is straightforward. Hormuz remains a powerful short-term price trigger, particularly at the front of the curve, where any serious re-escalation could quickly revive upside risk.

The longer-dated story is less comfortable for the bulls. At the peak of the US–Iran war, Goldman Sachs raised its three-year Brent assumption by $9 per barrel to $76, largely to reflect a higher structural security premium. The latest attacks justify that premium for now, but the expansion of bypass capacity creates a clear downside risk to it.

The market is not yet protected from Hormuz. But by 2028, it may be far less hostage to it.

Tech Supply Chain Daily: SK Hynix Has Become the AI Money Tree

SK Hynix has become one of the clearest financial winners of the global AI buildout. Its grip on high-bandwidth memory, the specialist chips paired with Nvidia’s processors, has turned the company into the most valuable piece of South Korea’s technology supply chain and one of the most important pressure points in the entire AI investment cycle.

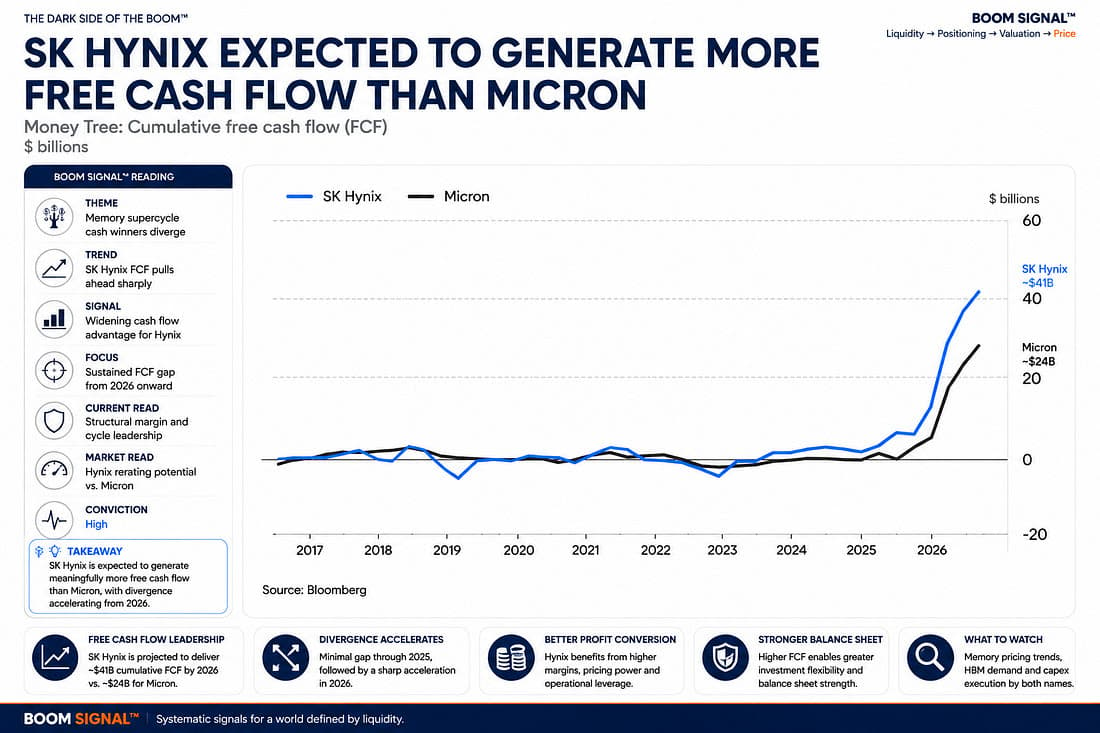

The numbers explain the enthusiasm. With advanced memory supply expected to remain tight into 2027, SK Hynix is forecast to generate more than $300 billion in free cash flow across this year and next, comfortably ahead of Micron. That cash machine helped support a record $26.5 billion US share sale and elevated the company into the trillion-dollar club.

The problem with becoming the market’s golden goose is that everyone eventually wants an egg.

South Korea’s government sees SK Hynix as a tool for reviving investment, rebuilding industrial confidence and spreading semiconductor development beyond the established manufacturing belt south of Seoul. Washington wants more capacity built in the US. Investors want rising profits and capital returns, while households increasingly see the stock as a national wealth vehicle.

Those demands are beginning to collide.

SK Hynix has committed to doubling wafer capacity within five years and is considering investments far beyond the $35 billion it has already deployed in the US. Yet the company is not expanding alone. Samsung is building additional high-bandwidth memory capacity, Micron is increasing US spending and China’s ChangXin Memory is emerging as a more credible competitive threat.

The result could be a familiar semiconductor trap. Today’s shortage encourages every producer to build at the same time. Several years later, that capacity arrives together, turning scarcity into oversupply just as demand begins to cool.

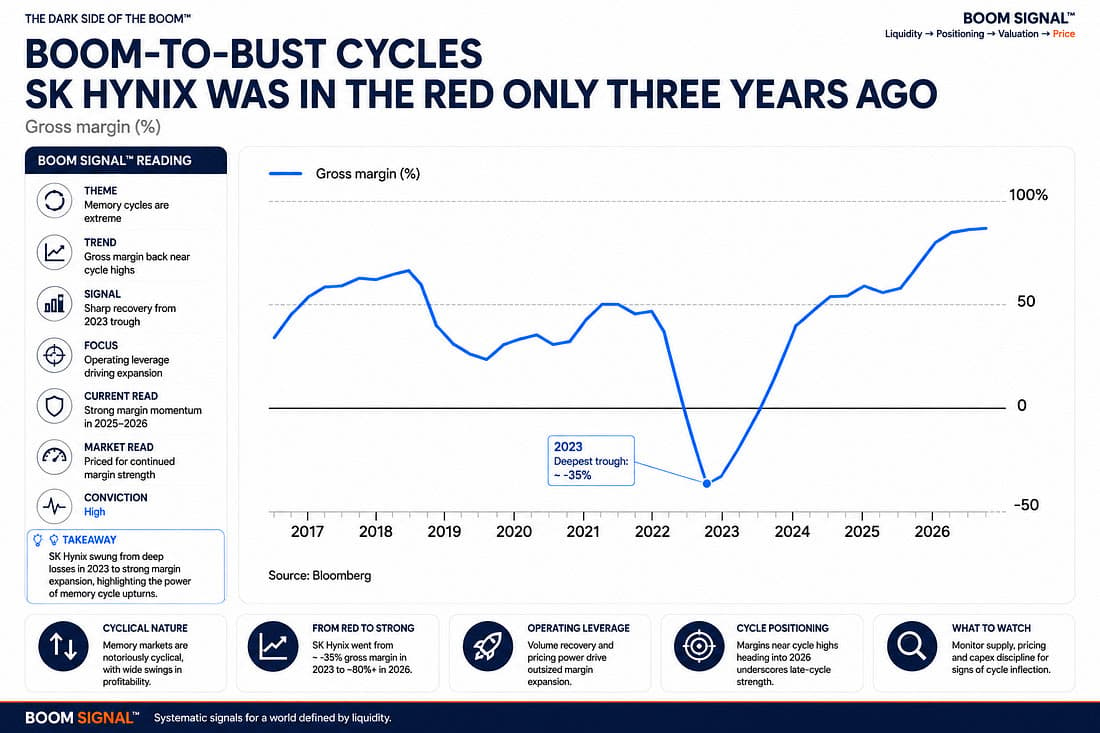

Management believes the memory shortage could persist beyond 2030, but investors should remember how quickly this industry turns. SK Hynix is enjoying record profitability now, yet it was losing money only three years ago. Memory remains one of technology’s most cyclical businesses, capable of moving from peak pricing to painful inventory correction within a couple of years.

That cycle matters because the shareholder base has changed. South Korean retail investors have piled into the stock while global institutions sold into the rally. Many have also chased leveraged exchange-traded funds launched just as volatility began to rise, leaving them exposed not only to price declines but to the slow erosion caused by volatility decay.

This turns SK Hynix into more than a semiconductor story. It is now a test of whether the AI supply chain can keep converting extraordinary demand into durable returns without repeating the industry’s old boom-and-bust script.

The company must satisfy governments seeking factories, investors demanding discipline and households betting that one stock can become a national pension plan. That is a heavy burden for any business, particularly one operating in a market where yesterday’s shortage can become tomorrow’s glut.

SK Hynix has become the AI money tree. The difficult part is making sure the next wave of spending produces more fruit rather than too many branches.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.