Five sessions, one round trip: Why the whipsaw is exactly what Warsh ordered

Markets opened July with a December hike as the base case and spent five trading sessions unlearning and relearning it. A 57K payrolls print bled the tightening bets out of the strip; a re-shut Strait of Hormuz is pushing them back in. Wednesday's minutes from the June Federal Open Market Committee (FOMC) meeting landed mid-round-trip, describing a world that had already stopped existing. The Federal Reserve (Fed) did not misfire; this is the operating system Kevin Warsh installed on June 17, running as designed.

Five sessions, two repricings

The Bureau of Labor Statistics (BLS) opened the sequence last Thursday with June Nonfarm Payrolls (NFP) at 57K against a consensus near 115K; May was cut to 129K from 172K, and the two prior months lost a combined 74K to revisions. The unemployment rate fell to 4.2%, and for the wrong reason: participation dropped to 61.5%, its lowest since March 2021, as roughly 720K people left the labour force in a single month. Average hourly earnings rose 3.5% YoY against headline inflation above 4%; real pay is still shrinking.

The strip did what the data said. A September hike came off the table, October stayed pencilled, and the sell side spent the long weekend capitulating to the peace trade: the US Energy Information Administration cut $27 from its third-quarter Brent forecast and Saudi Arabia cut official selling prices by the most in two decades. Within two sessions, the trade they were chasing was gone.

Washington revoked Iran's oil-export licence on Tuesday, three tankers were hit in the Strait of Hormuz, and by Wednesday, President Donald Trump was declaring the ceasefire over. Brent traded through $80 at the highs as the front spread flipped from contango to backwardation, and tanker traffic through the strait all but stopped. That is the war's allotted space in this note, because for rate purposes only one line matters: the single largest input into the next run of inflation prints is again being set by ordnance.

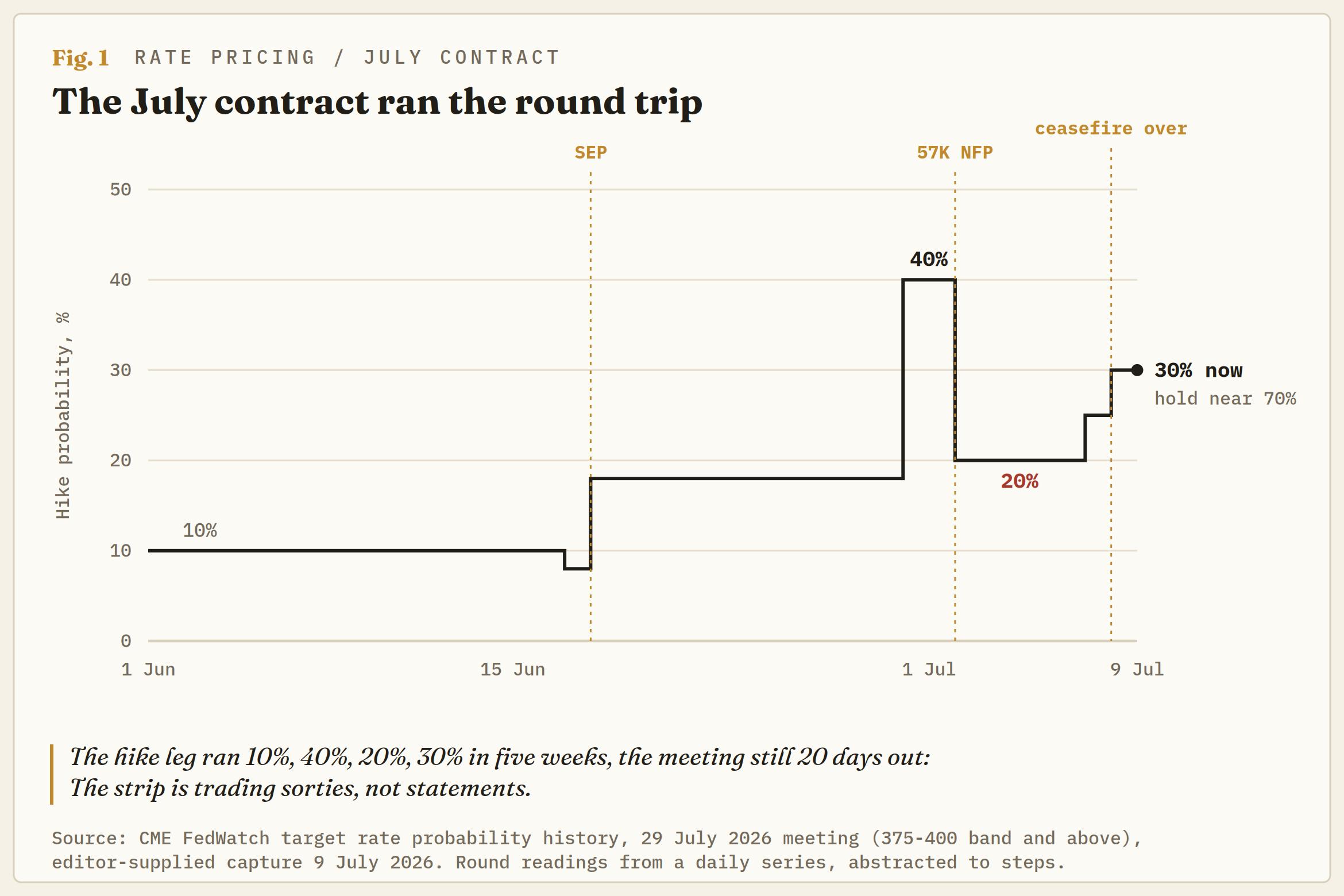

The July contract tells it in miniature: its hike tail ran to 40% in late June, was cut to 20% by the payrolls print, and has re-armed to 30% per CME FedWatch, leaving the hold near 70%, with money markets still carrying at least one 25bp hike this year.

Nine dots walked in, a few walked out

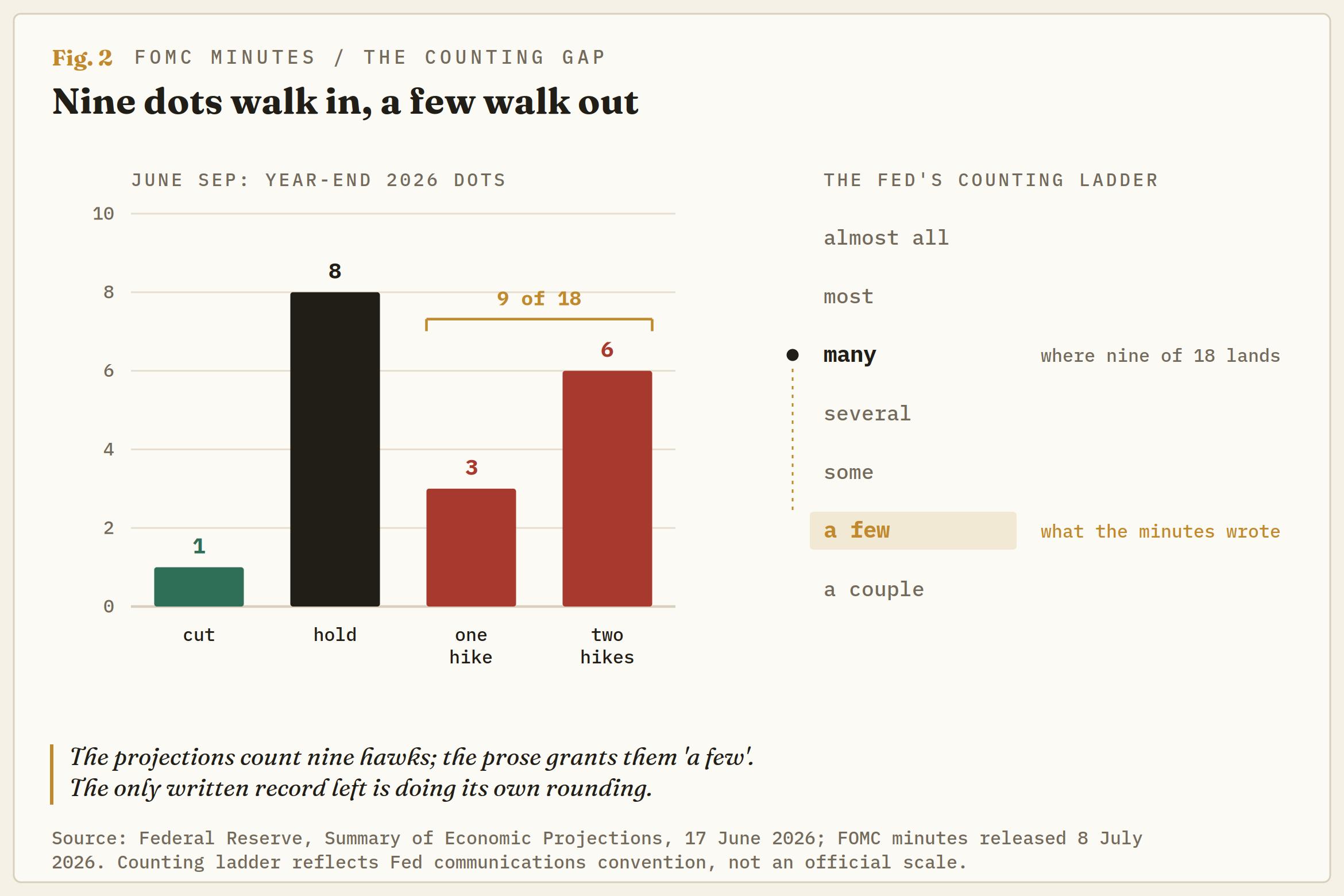

The June Summary of Economic Projections (SEP) showed nine of 18 dots penciling in at least one 2026 hike, the lurch that made December a live contract. The minutes of the same meeting describe only "a few" participants judging that another hike could eventually become appropriate. In the Fed's counting lexicon, “a few” sits near the bottom of the ladder; nine of 18 would ordinarily earn an "about half." Somewhere between the dot plot and the prose, the hawk bloc shrank.

There are two ways to read the gap, and neither is comfortable. Either the dots are scenarios rather than convictions, pencilled sketches of a path nobody will argue for on the record, or the last detailed account of the committee's thinking is itself being managed down. Under a chair who struck forward guidance and withheld his own dot, the minutes are no longer a postscript, and even they read softer than the projections they accompany.

The arithmetic makes it worse. Dots are anonymous across the full set of participants, but only 12 members vote, and June's hold at 3.50%-3.75% passed 12-0. The hawkish case exists in projections and in what Warsh called a "family fight", nowhere yet in a dissent. The sharpest detail is that the camps are largely the same people: the record sketches paths where inflation fades and lower rates follow, alongside paths where the war, tariffs and AI demand keep prices elevated and firming follows.

One committee carries two opposite reaction functions and outsources the choice to the data; a December hike buyer is pricing a coalition that has never shown up on a ballot.

The record is shrinking on every page

The statement went first, cut to roughly 130 words from about 310 and stripped of forward guidance along with its easing bias. The minutes confirm the committee signed off: a majority of participants saw advantages in the shorter statement, and a number called it an opportune moment to rethink the format altogether. This is a regime with buy-in, not a new chair's whim, and regimes outlast their authors.

The minutes themselves ran shorter than usual, and the five task forces Warsh unveiled at the podium, covering communications, the balance sheet, data sources, productivity and the inflation framework, earned barely a line of recorded discussion. Add the floated idea of press conferences held only when the Fed has something to say, and every channel is narrowing at once.

Since the debut presser, Warsh has made one public appearance, at Sintra, warning that nobody should expect his Fed to be comfortable with inflation above 2%. One sentence from one podium currently carries the entire reaction function.

Minutes for a world that no longer exists

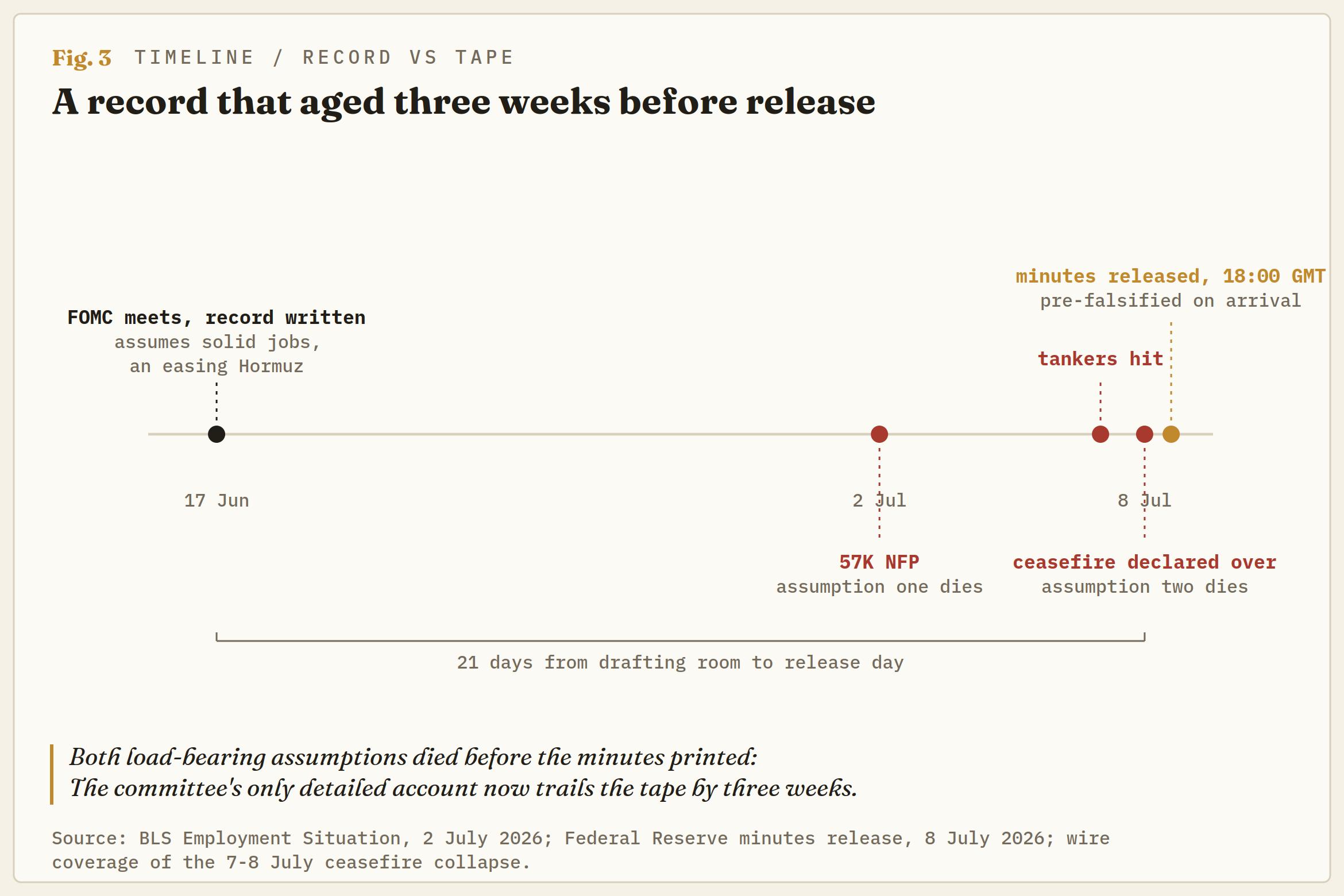

Read closely, the June record rests on two assumptions that died before it printed. Its labour read predates the 57K print, the revisions and the participation slide. Its inflation path leans on pump prices falling and on supply disruptions from a shut Hormuz diminishing, and that conditional inverted before the document was a day old.

What survives the staleness is the part the market has barely priced. The staff revised inflation higher for both 2026 and 2027, with participants flagging the war, tariffs and AI-related investment as the persistence channels, an admission that price pressure should outlast the war premium itself. That is the downstream passthrough these pages argued after the debut presser, fertiliser and feedstock costs grinding into food on a planting-to-harvest lag, and round two of the shock lands on a complex that never normalised from round one.

The AI line deserves its own beat because it decides which scenario wins. Participants see the buildout sustaining price pressure on technology products and electricity now; Warsh has publicly planted himself in the productivity camp, where AI is net disinflationary eventually. If the chair discounts the one domestic inflation driver his committee flags as current, the burden of proof for a hike quietly rises, whatever the dots say.

The patience clock

Sitting over all of it is the man who made the appointment. Trump picked Warsh expressly to deliver cuts, called the no-cut debut fine, and has now personally re-armed the December contract by declaring the ceasefire dead, his own escalation feeding straight back into his own borrowing costs. That patience has never been tested by a war premium with his name on it.

Every print now trades twice

The next test is Tuesday. June Consumer Price Index (CPI) data lands July 14 at 12:30 GMT and covers the peace-dividend month, when pump prices were falling, so a soft headline is close to baked, and the market then has to decide what a backward-looking print is worth against crude up roughly 10% inside a week. The Producer Price Index (PPI) follows on July 15 with retail sales on July 16, and the FOMC sits July 28-29 with no SEP attached and no guarantee of a podium, given the chair's preference for speaking only when there is something to say.

The lean is to stop trading the level of December pricing and start trading its range. Terminal conviction has died twice in three weeks, once on a payrolls print and once on a tanker attack, and a hold-through-December consensus is one hot expectations print or one more week of a shut strait from the same fate.

In a no-guidance regime, every print trades twice, once on the number and once on its reconciliation with the live tape, so a soft June CPI into $80 crude is a fade rather than a trend.

Warsh built the regime so markets would trade the data instead of the Fed, and for five sessions, markets have obliged, except the input that mattered was measured in sorties, not basis points. The committee has written down two futures and told the tape to pick one. The tape is currently picking both, twice a week.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joshua Gibson

FXStreet

Joshua joins the FXStreet team as an Economics and Finance double major from Vancouver Island University with twelve years' experience as an independent trader focusing on technical analysis.