The US economy remains resilient and fairly robust

Outlook: The US economy remains resilient and fairly robust. But a low reading in PPI and/or CPI this week might re-ignite doubts about the Fed’s resoluteness, even if the vast majority think the Nov 3 policy meeting brings 75 bp come hell or high water. It’s a small and temporary risk to the dollar. Today Chicago Fed Evans and Vice Chair Brainard speak about "Restoring Price Stability in an Uncertain Economic Environment" at 1:35 pm ET. There’s a webcast if you need a nap.

The problem with the outlook for the Fed is that we cannot know how much it respects The Lag. It claims to be data-dependent but surely all those brainy back- office economists are factoring in that the data is terribly backward-looking, and by more than one month. That puts the Dec 14 policy meeting covered in question marks–as it should.

By the time of the Dec meeting, the Fed will have two more sets of data in jobs, inflation and supporting actors like retail sales. So far the CME Fedwatch tool shows 62.5% think the Dec hike will be “only” 50 bp vs. 23% who see 75 bp. But if the economy persists is being resilient and robust, especially labor, the Fed may go for the whole megillah in Dec and overshoot. We expect to hear the word overshoot any minute now.

We get the Sept meeting minutes on Wednesday, sure to reinforce the hawkish view. Note we get PPI before CPI on Wednesday, too, with headline expected at 8.4% y/y from 8.7% in August and core unchanged at 7.3% y/y.

The big news this week is the CPI, last at 8.3% in August from 8.5% in July and the lowest in 4 months. The consensus forecast is for headline to come in at 8.1% and core at 6.5% after 6.3% in Aug. The Cleveland Fed sees Sept headline at 8.04%, a decent drop, and core at 6.58%, a scary-big rise.

Attention focused on oil and gas is apparently misplaced. Gasoline is going up and inventories are shrinking (actually normal for this time of year), but natural gas prices are falling. Trading Economics says prices are close to the 3-month low and last week had the biggest ever increase in inventories.

By Friday when everyone is exhausted, we get retail sales, forecast down a smidge to 0.2% m/m vs. 0.3% in Aug. It may be important that sales ex-autos are expected negative at -0.1% m/m, if less negative than -0.3% in August.

Retail sales are important as part of “real personal consumption expenditures,” one of the Atlanta Fed’s primary GDPNow components and something that drove the Q3 forecast to a whopping 2.9% on Friday, from 2.7% only a few days before and a lousy 0.2% on Sept 21. We get a new version on Friday. For what it’s worth, we get the first estimate of Q3 from the government on Oct 27. Bloomberg forecasts 1.5%. In practice, the Atlanta Fed overshoots and Bloomberg is probably closer, but never mind--neither number is a negative.

On Friday we also get the preliminary University of Michigan consumer sentiment for Sept, probably little or no change.

In other news, the IMF and World Bank are holding their annual meeting in Washington, with a gloomy message about world growth falling off the cliff and central banks being overly aggressive and harming the poor. China is preparing for the Communist Party Congress that is supposed to install Xi for life. Worry has switched from Taiwan to what China will do about the new US chip rules, which have the potential to cost China dearly near-term (and the US dearly longer-term).

There’s a ton of news developments and data this week, but perhaps simplistically, we think what counts for FX is those yields.

What about “global financial market instability”? The UK issues were not a Lehman moment and not likely to become one. We cringe at the continuing use of the word “crisis.” UK bonds are still being sold and the 10-year yield is up 0.091% to 4.328%, in part because of the BoE announcing an extended plan to increase buying and also launch a long-term facility to address liquidity problems. The BoE wants the market to know it is not trying to bring down yields, just adjusting for liquidity reasons, and it looks like a success. Bloomberg reports “The Treasury also made its own attempt to calm markets, with Chancellor of the Exchequer Kwasi Kwarteng saying he will announce his medium-term fiscal strategy and accompanying economic forecasts on Oct. 31, earlier than initially planned.”

You’d think these developments would be good news but sterling fell anyway, likely because Truss’ damage control is only just beginning. She meets with Tory MP’s this week for fend off those sending messages about “no confidence” and possible resignations. As noted last week, public opinion remains solidly anti-Tory.

But political turmoil is a different thing from financial market instability, something not every commentator appreciates. Similarly, we see reasonableness restored by those analysts who point out that good news (e.g., payrolls) being bad news for the stock market is not about the news itself but rather expectations of what the Fed will do. Since that consists of staying an already mapped course, it’s pretty silly to blame the Fed for Friday’s sell-off.

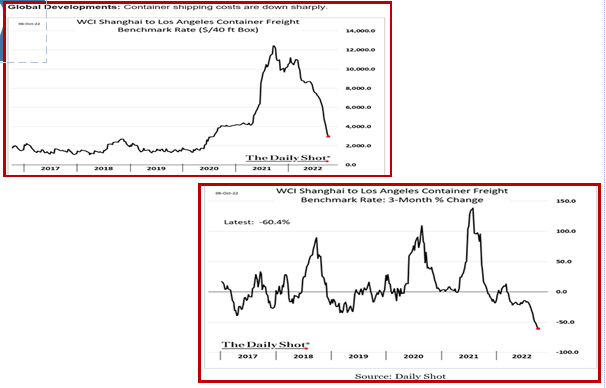

Tidbit: The always annoying but usually right Krugman noted on Friday that “the cost of shipping a container across the Pacific, which was $20,586 in September 2021, is now $2,265.” This doesn’t mean supply chain issues are gone, but does imply inflation from this cause has faded. A different source verifies, saying the backlog at ports in S. California “reached 109 container ships in January of last year, but more recently has dropped below 10. Meanwhile, the cost of shipping a container from China to the United States has fallen below $4,000, compared to last year’s high of around $20,000” [as of Sept 29].”

To confirm, the WSJ Daily Shot delivers these dandy charts. Note that on the 3-month basis, prices are down the most in 5 years.

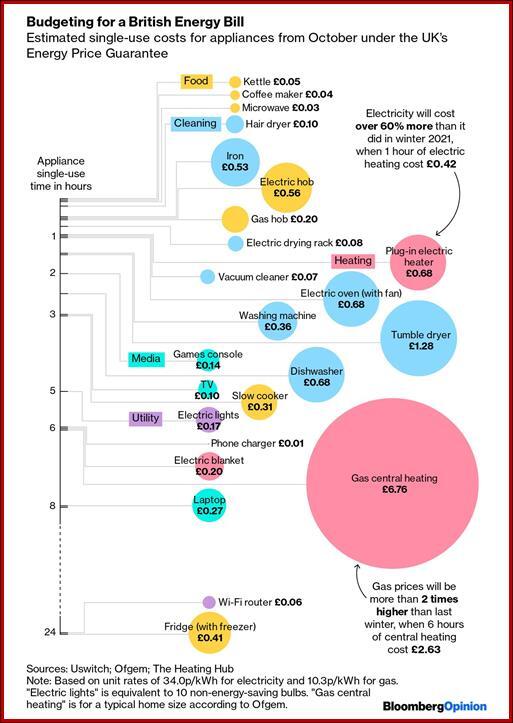

Tidbit 2: UK PM Truss is madly unpopular, with a lower rating than Boris at his lowest. Bloomberg quotes people saying things like “Only four weeks into her leadership, all the talk at the Conservative Party conference in Birmingham was whether UK Prime Minister Liz Truss will survive until Christmas.”

Even the loyal Tory demographic homeowners are disenchanted as they face mortgage rate soaring and raising their monthly cost as much as 70%.

(That’ll teach ‘em to float.) And people acknowledge that many “nanny state” regs are actually a Good Thing, like seat belts. Truss doesn’t want to publish information on how households can save energy because it’s too “interventionist.” See the chart–you’ll be okay if you turn off the central heat in favor of the fireplace and hang your sheets and towels to dry instead of running the electric dryer.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat