The US Dollar just beat the Swiss Franc at its own safe-haven game

As the king among safe havens, the Swiss Franc (CHF) is supposed to benefit from geopolitical shocks such as the Iran war. This time, it didn’t.

The Swissie is nearly 6% below January’s peak against the US Dollar (USD) after a sharp decline that came along with the war in Iran and the closure of the Strait of Hormuz. The Swiss currency has recovered somewhat in the past week, but its relatively subdued performance during one of the major recent geopolitical shocks has left questions over why the Franc failed to behave like a traditional safe-haven.

What happened? The conflict in the Middle East and the subsequent energy shock have led to a winner-takes-it-all scenario, with the US Dollar as the only shelter in moments of risk aversion.

How did we get here?

Going back to the end of January, the concern among Swiss authorities was not a weak Franc, but an excessively strong one. The currency had become a headache for Swiss exporters, already hit by US tariffs. The mounting geopolitical tensions and a weaker US Dollar –the Fed was hinting at rate cuts at that time– boosted the Swiss Franc to 0.7604 against the Greenback, its highest level since July 2011 in the midst of the global financial crisis.

Then everything changed. Bombs started falling across the Middle East, Tehran closed the Strait of Hormuz, and the market stopped rewarding traditional safe havens equally. On the one hand, the Swiss National Bank (SNB) signaled its willingness to intervene against the excessive CHF strength. On the other, Switzerland’s dependence on energy imports started to manifest, with Industrial Production falling sharply in the first quarter.

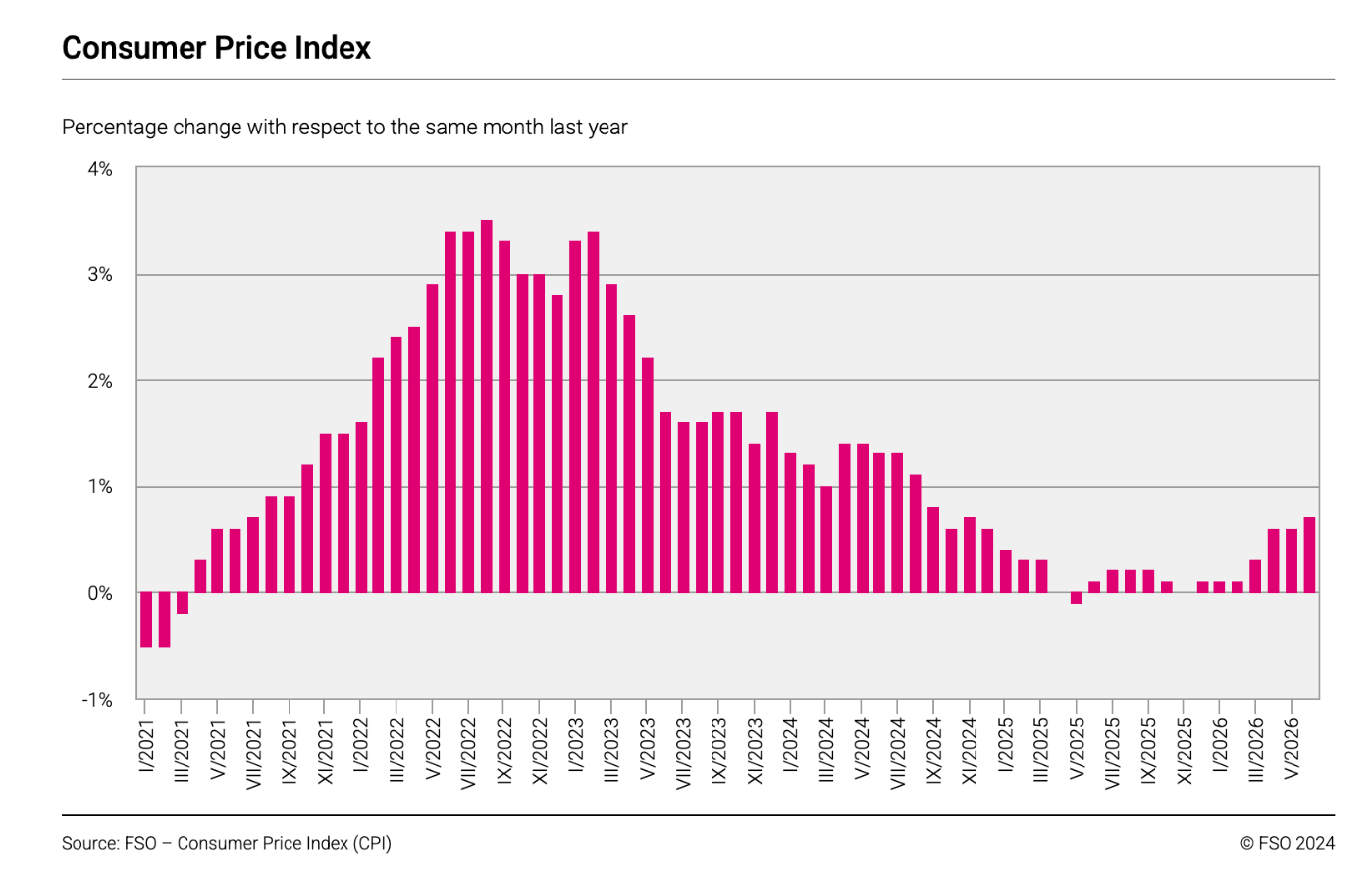

Swiss inflation has remained subdued despite higher energy prices

Meanwhile, Swiss inflation remains anchored near 0%, leaving the Swiss central bank with little reason to tighten policy further. Last week’s Consumer Price Index (CPI) report showed monthly inflation cooling back to 0% in June from 0.2% in May, while the annual rate declined to 0.5% from 0.6%.

That matters because higher Oil prices were supposed to reignite inflationary pressures. Instead, Swiss price growth barely moved. Without persistent inflation, there is little urgency for the SNB to raise interest rates, leaving the Franc without one of the traditional pillars that usually support a currency.

Commerzbank analysts Michael Pfister and Norman Liebke expect a limited movement in the CHF in the coming months amid the SNB’s dovish stance: "We therefore continue to expect the SNB to leave its key interest rate unchanged in the coming months, meaning no significant franc movement is likely to result from this policy."

The Fed left the SNB behind

At the same time, the picture in the US looks very different. While Swiss inflation remains close to zero, the US economy continues to show surprising resilience. Although June’s Nonfarm Payrolls disappointed, the labour market remains relatively stable and inflation is still running above the Federal Reserve’s (Fed) target.

Beyond that, recent US macroeconomic data have reinforced the narrative of American exceptionalism. Gross Domestic Product (GDP) expanded by more than 2% in the first quarter, with manufacturing and services activity growing at healthy levels. At the same time, the ongoing AI investment boom continues to attract foreign capital into the US, supporting demand for the US Dollar.

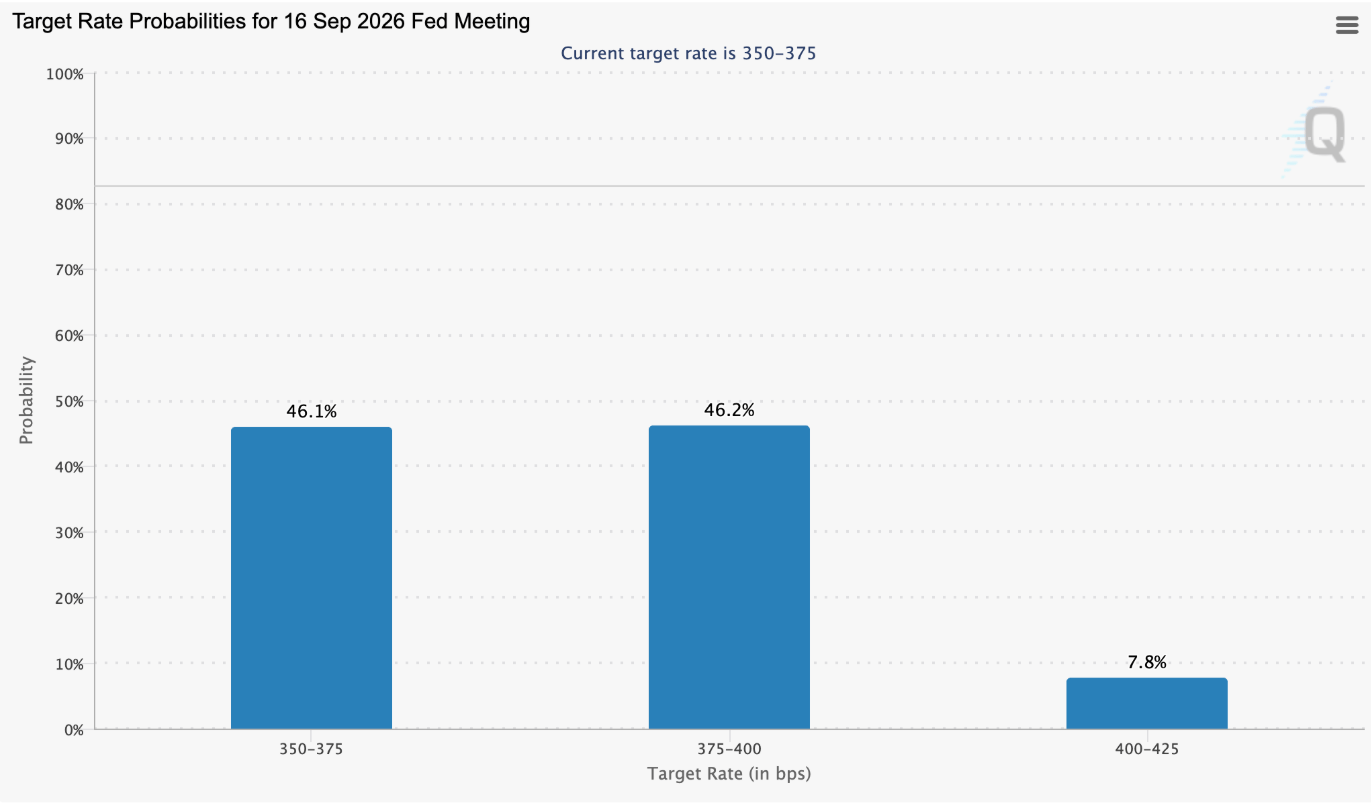

Against this backdrop, Fed officials, led by the new Chairman Kevin Warsh, have adopted increasingly hawkish language, prompting investors to shift previous expectations of at least one Fed rate cut in 2026 to rate hikes that might come as soon as October. All in all, an ideal context for a steady US Dollar appreciation.

The Dollar has become the world's safe haven

The US Dollar has emerged as the market’s preferred safe-haven in times of turbulence, and not just because of geopolitical tensions. Higher US interest rates, economic resilience and a more hawkish Federal Reserve have combined to make the Greenback attractive even as Middle East risks begin to fade.

That leaves the Swiss Franc in an uncomfortable position. Traditionally, global turmoil would have pushed investors toward Switzerland. This time, capital has largely flowed into the US Dollar instead.

Unless the macroeconomic scenario changes radically, the Swiss Franc is likely to remain on the defensive. June's weak Nonfarm Payrolls briefly interrupted the USD’s rally, not enough to change the broader narrative. For now, the Fed’s interest-rate advantage continues to outweigh the Franc’s traditional safe-haven appeal.

Swiss Franc FAQs

The Swiss Franc (CHF) is Switzerland’s official currency. It is among the top ten most traded currencies globally, reaching volumes that well exceed the size of the Swiss economy. Its value is determined by the broad market sentiment, the country’s economic health or action taken by the Swiss National Bank (SNB), among other factors. Between 2011 and 2015, the Swiss Franc was pegged to the Euro (EUR). The peg was abruptly removed, resulting in a more than 20% increase in the Franc’s value, causing a turmoil in markets. Even though the peg isn’t in force anymore, CHF fortunes tend to be highly correlated with the Euro ones due to the high dependency of the Swiss economy on the neighboring Eurozone.

The Swiss Franc (CHF) is considered a safe-haven asset, or a currency that investors tend to buy in times of market stress. This is due to the perceived status of Switzerland in the world: a stable economy, a strong export sector, big central bank reserves or a longstanding political stance towards neutrality in global conflicts make the country’s currency a good choice for investors fleeing from risks. Turbulent times are likely to strengthen CHF value against other currencies that are seen as more risky to invest in.

The Swiss National Bank (SNB) meets four times a year – once every quarter, less than other major central banks – to decide on monetary policy. The bank aims for an annual inflation rate of less than 2%. When inflation is above target or forecasted to be above target in the foreseeable future, the bank will attempt to tame price growth by raising its policy rate. Higher interest rates are generally positive for the Swiss Franc (CHF) as they lead to higher yields, making the country a more attractive place for investors. On the contrary, lower interest rates tend to weaken CHF.

Macroeconomic data releases in Switzerland are key to assessing the state of the economy and can impact the Swiss Franc’s (CHF) valuation. The Swiss economy is broadly stable, but any sudden change in economic growth, inflation, current account or the central bank’s currency reserves have the potential to trigger moves in CHF. Generally, high economic growth, low unemployment and high confidence are good for CHF. Conversely, if economic data points to weakening momentum, CHF is likely to depreciate.

As a small and open economy, Switzerland is heavily dependent on the health of the neighboring Eurozone economies. The broader European Union is Switzerland’s main economic partner and a key political ally, so macroeconomic and monetary policy stability in the Eurozone is essential for Switzerland and, thus, for the Swiss Franc (CHF). With such dependency, some models suggest that the correlation between the fortunes of the Euro (EUR) and the CHF is more than 90%, or close to perfect.

Author

Guillermo Alcala

FXStreet

Graduated in Communication Sciences at the Universidad del Pais Vasco and Universiteit van Amsterdam, Guillermo has been working as financial news editor and copywriter in diverse Forex-related firms, like FXStreet and Kantox.