Global macro transmission monitor – Week ending July 3, 2026

Executive transmission map

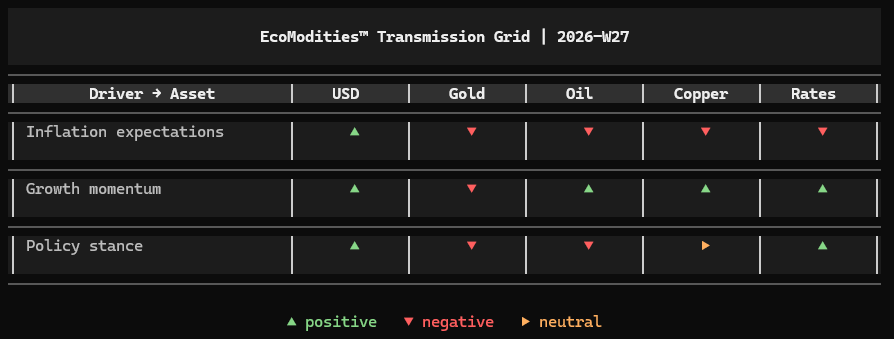

The macro transmission chain rotated back toward USD resilience last week as labor-market data softened but remained sufficiently robust to sustain confidence in the broader economic backdrop. Canadian growth surprised positively, while weaker US payrolls contrasted with a lower unemployment rate and stable wage growth.

Inflation expectations remained relatively firm, supporting the dollar and rates markets while limiting participation across gold and defensive assets. Oil and copper retained support through cyclical resilience despite softer manufacturing activity.

Policy transmission remained supportive for USD pricing as markets continued to anticipate a gradual and cautious easing cycle. Cross-asset alignment strengthened around relative US resilience rather than outright growth acceleration.

1. Macro shock layer

A. Inflation shock

What moved

No major inflation release dominated the week, allowing markets to focus on labor conditions and growth momentum.

Inflation expectations nevertheless remained sufficiently firm to sustain support for USD and rates markets.

Why it matters

With inflation no longer surprising materially lower, markets increasingly shifted attention toward growth resilience and labor-market developments.

Transmission path

- USD retained inflation-driven support.

- Gold lost part of its defensive appeal.

- Oil and copper faced tighter financial conditions.

- Rates remained relatively supported.

FX transmission

The dollar maintained broad support as inflation expectations remained stable despite softer activity indicators.

B. Growth shock

What moved

Growth signals remained mixed but generally constructive.

- Canada GDP m/m: 0.5% vs 0.4% expected.

- ISM Manufacturing PMI: 53.3 vs 53.8 expected.

- Non-Farm Payrolls: 57K vs 114K expected.

- Unemployment Rate: 4.2% vs 4.3% expected.

- Average Hourly Earnings m/m: 0.3% vs 0.3% expected.

Why it matters

Payroll growth disappointed meaningfully, but lower unemployment and stable wages prevented a broader deterioration narrative from emerging. Markets interpreted the data as a moderation rather than a collapse in labor conditions.

Transmission path

- USD remained supported through relative resilience.

- Oil benefited from constructive demand expectations.

- Copper retained support from cyclical sentiment.

- Gold faced headwinds from improving risk appetite.

- Rates remained firm

FX transmission

Growth-sensitive currencies traded selectively, while the USD continued benefiting from relative macro stability despite softer payroll data.

C. Policy shock

What moved

No major central-bank decision took place during the week, although Fed communication continued reinforcing expectations for a gradual normalization process.

BOE communication remained broadly unchanged, while markets focused increasingly on labor-market developments.

Why it matters

Policy expectations remained supportive for the USD and rates complex, preventing softer payrolls from generating a broader dovish repricing.

Transmission path

- USD retained policy support.

- Gold remained pressured.

- Oil faced tighter financial conditions.

- Copper remained broadly neutral.

- Rates pricing stayed relatively firm.

FX transmission

Rate differentials continued supporting the USD as markets delayed expectations for aggressive policy easing.

2. Cross-asset transmission grid – 2026-W27

3. Market alignment check

Cross-asset alignment remained relatively strong during the week.

Softer payroll growth failed to trigger a meaningful defensive rotation as lower unemployment and resilient wage dynamics supported confidence in the broader macro backdrop. Oil and copper continued reflecting cyclical resilience, while gold struggled against firmer USD conditions.

The macro chain currently shows inflation and policy transmission remaining dominant, while growth momentum has moderated without materially deteriorating.

4. Forward pressure points

USD

Pressure remains concentrated around labor-market resilience and evolving Fed expectations.

Gold

Gold remains highly sensitive to real yields and shifts in policy repricing.

Oil

Oil continues balancing supportive cyclical conditions against tighter financial conditions.

Copper

Copper remains dependent on industrial activity expectations and global demand resilience.

Rates

Rates markets remain vulnerable to further labor-market surprises and shifting policy expectations.

One-line takeaway

The macro transmission chain remained centered on USD resilience last week, as softer payroll growth was offset by stable labor conditions, supporting rates and cyclical assets while limiting participation across Gold.

Author

Luca Mattei

LM Trading & Development

Luca Mattei is a market analyst focusing on FX, metals, and macroeconomic trends. He develops trading tools for retail and professional traders, coding indicators and EAs for MT4/MT5 and strategies in Pine Script for TradingView.