Why Oil and Natural Gas are no longer trading the same story

At first glance, both markets belong to the same sector. Their behavior in June suggested otherwise. Oil rallied on fears that Middle East tensions could affect supplies, while U.S. gas prices continued to respond mainly to storage conditions, weather forecasts, and domestic consumption patterns.

That divergence has turned WTI vs NGAS into one of the more interesting relative-value relationships in the energy complex. Although both assets belong to the same sector, they are currently responding to very different drivers — and that separation is creating new opportunities for traders.

The great energy split

A few weeks ago, oil traders could hardly talk about anything except Hormuz. Every new headline from the Middle East seemed capable of moving the market. Brent briefly traded above $95 a barrel, and WTI approached $93 before both retreated sharply. By early July, Brent had fallen back toward the low-$70s and WTI toward the high-$60s as tanker traffic through the Strait of Hormuz normalized, part of the geopolitical risk premium faded, and OPEC+ agreed to another production increase. Even so, Reuters noted that uncertainty surrounding Iran and regional supply risks continued to influence market sentiment.

Natural Gas barely followed

That statement is largely true for U.S. Henry Hub prices, though not for every gas market. European gas contracts and LNG-linked benchmarks reacted to the Hormuz risk as well, but the move remained considerably smaller than the rally in crude. Reuters reported that Europe's gas market absorbed the disruption far more calmly than oil, reflecting relatively comfortable inventories and limited immediate concerns over LNG availability despite continued risks to shipping.

That difference highlights the growing gap in the oil vs. natural gas relationship. The difference comes down to who buys and sells these commodities. Oil prices respond to events happening almost anywhere in the world. U.S. natural gas is a different story. Even with LNG exports growing, storage levels and domestic demand still carry much more weight.

Storage conditions help explain why gas prices remained relatively restrained. The storage picture is another reason gas has struggled to keep up with oil. The latest EIA data showed working gas inventories at roughly 2.9 Tcf, comfortably above the five-year average for this point in the injection season. EIA also continues to project an average Henry Hub price of about $3.34 per MMBtu during the second half of 2026, suggesting that the market is not pricing an immediate supply shortage.

The result is a striking WTI/NGAS comparison. You can see the difference just by looking at the headlines. Oil traders keep an eye on shipping routes and developments in the Middle East. Gas traders are spending far more time talking about inventories and summer weather.

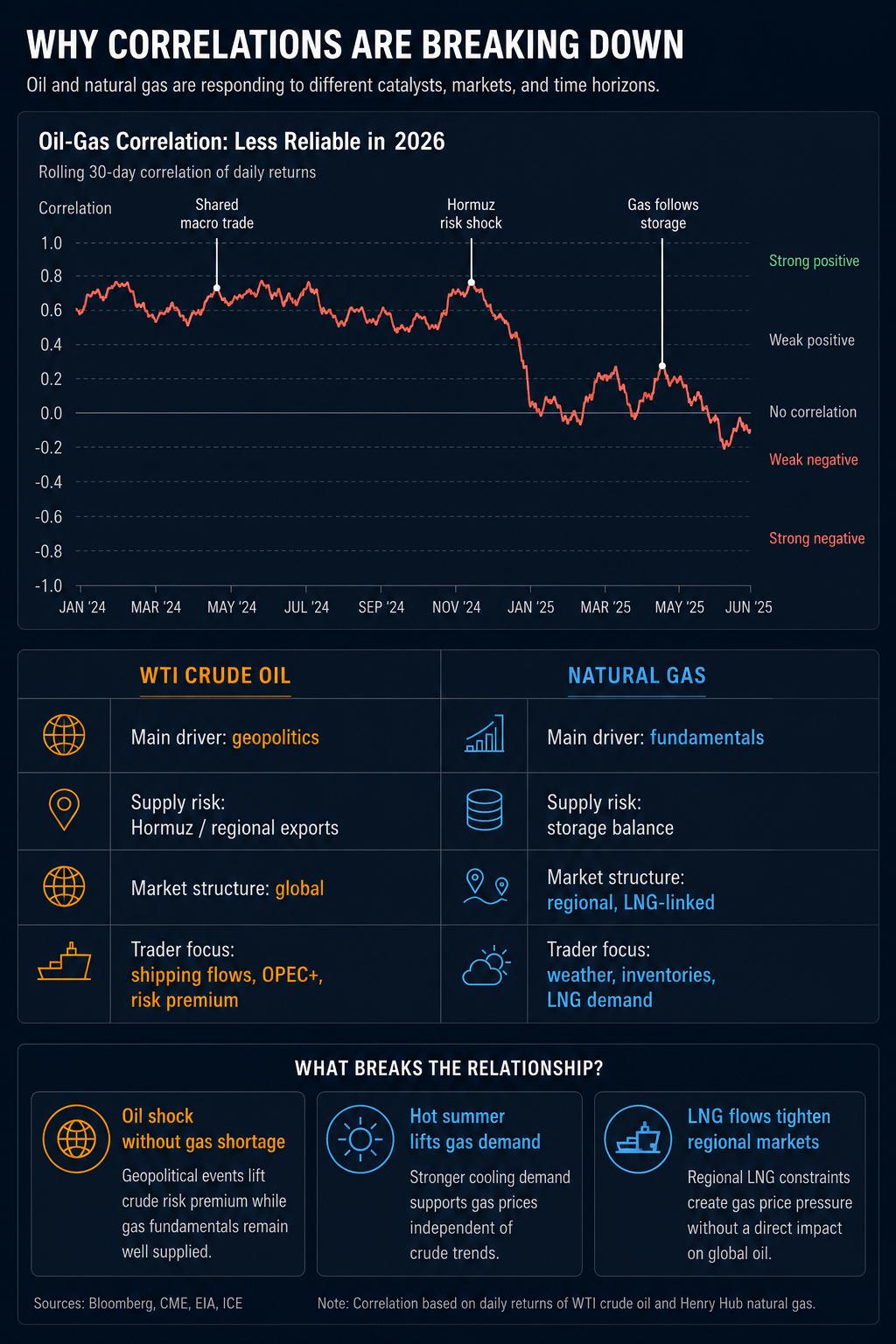

Why correlations are breaking down

Years ago, oil and gas were often moving for the same reasons. That is much less obvious today. The current crude oil vs. gas prices dynamic has more to do with how differently the two markets are structured than with any single macrofactor.

U.S. shale production created an abundant natural gas supply, while oil remains tied to a much more international pricing system.

That is why the recent energy market divergence should not automatically be viewed as a temporary anomaly.

Oil is trading geopolitics

The headlines are not moving prices as dramatically as they did during the peak of the tension, yet few oil traders are looking away. The region remains important, OPEC+ remains important, and so do the shipping lanes that carry crude to global markets.

The June price action offered a clear example. The move up was fast, and so was the move back down. Oil rallied as traders worried about Hormuz, then reversed course when the risk no longer looked quite as immediate. That kind of price action tends to show up when geopolitics is doing most of the driving.

Natural Gas is trading fundamentals

The conversation in the gas market sounds very different. Traders are talking about storage, weather, LNG exports, and production. As long as those numbers look reasonably healthy, headlines that send oil prices flying may barely register in natural gas.

Current EIA projections suggest storage conditions remain sufficient to prevent the type of supply panic that often drives large oil rallies.

This helps explain the weakening oil and gas correlation visible throughout much of 2026.

Another reason is that the cost of natural gas vs. oil remains heavily influenced by regional infrastructure, storage capacity, and electricity demand rather than maritime supply routes. That distinction has become increasingly important for traders comparing energy markets.

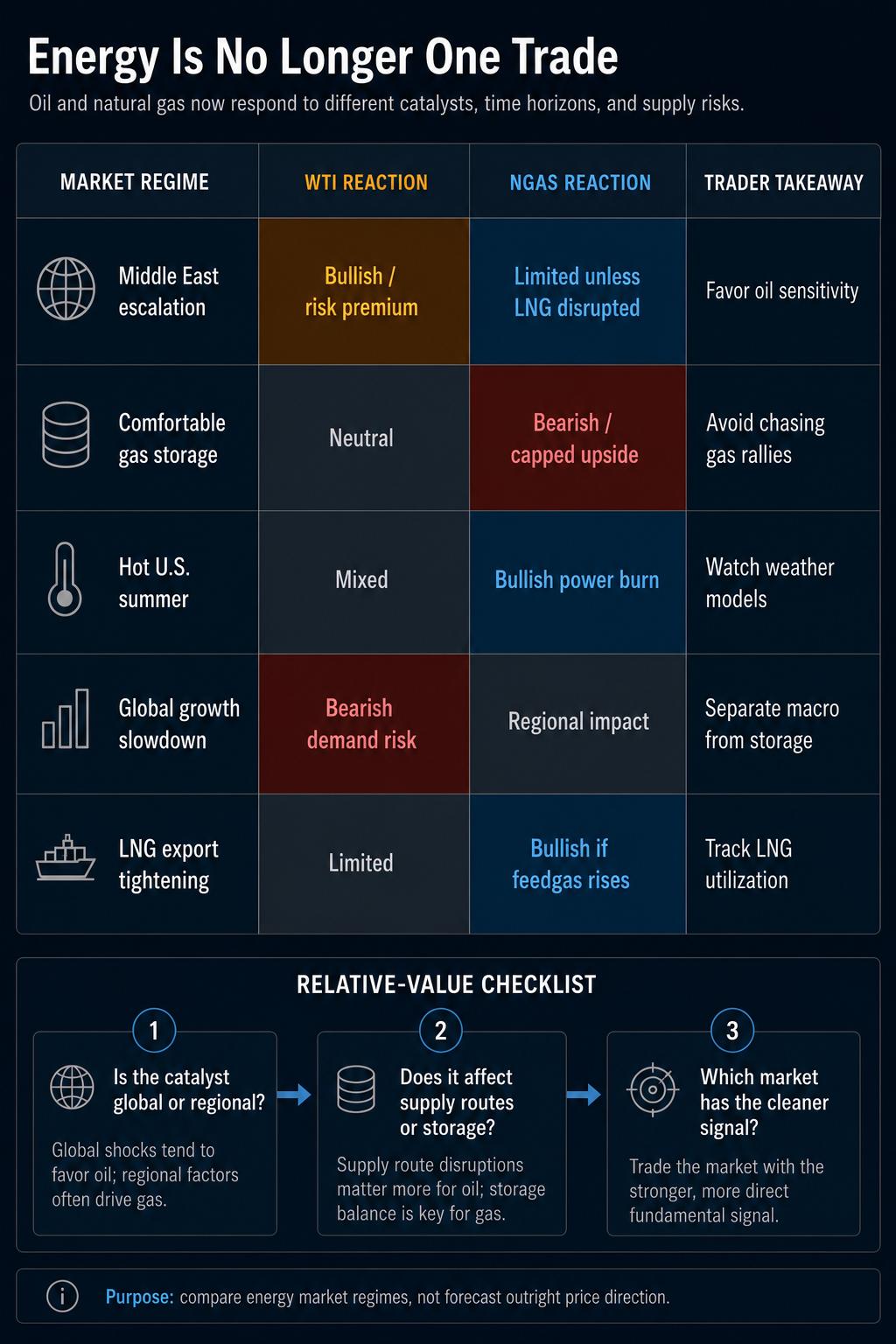

What traders are watching

For traders evaluating a potential Versus Trade WTI NGAS, the key question is whether the current divergence can persist.

The answer depends on which catalyst arrives first.

A renewed disruption to Middle East supply could push oil higher again even if natural gas remains stable. On the other hand, an unusually hot U.S. summer could tighten electricity demand and lift gas prices without generating the same upside for crude.

That creates opportunities for traders seeking exposure to oil vs. gas performance rather than taking outright directional risk in the broader commodity sector.

One practical framework is to monitor three indicators:

- Strait of Hormuz shipping activity;

- US Natural Gas storage reports;

- LNG export utilization rates.

Together, those variables currently provide more useful signals than broader macro headlines.

For active traders, the most useful question may not be whether energy prices are rising or falling. Instead, it is whether natural gas vs. oil prices are being driven by the same catalyst. When the answer is no, relative-value opportunities often emerge.

The bigger lesson for energy markets

The current energy commodities comparison shows why traders should avoid treating the energy sector as a single asset class.

A few years ago, many participants assumed natural gas vs. oil movements would remain closely linked. June 2026 suggests otherwise.

The crude oil vs. natural gas relationship increasingly reflects two separate markets operating under different rules. Oil remains highly sensitive to international supply disruptions, while gas continues to trade local fundamentals and seasonal demand patterns.

For traders considering whether to trade oil vs. natural gas, that distinction matters. Relative-value opportunities often emerge when markets that usually move together begin responding to different catalysts — and the current environment is a useful example.

The comparison between natural gas vs. crude oil is, therefore, less about choosing a direction and more about identifying which market has the stronger catalyst. In some periods, oil leads. In others, weather and storage dominate gas pricing.

Right now, oil is trading a combination of geopolitics, OPEC+ supply decisions, and changing perceptions of global supply risk. Natural gas continues to trade primarily on storage levels, weather, and domestic demand fundamentals.

That may be the most important takeaway from the current oil vs. natural gas price comparison. The traditional relationship between the two fuels has weakened, making it increasingly important to evaluate each market on its own fundamentals. Whether comparing oil heat vs. natural gas demand trends, regional infrastructure constraints, or broader supply risks, traders are finding that energy markets no longer move as one.

Understanding that shift may ultimately matter more than predicting the next headline.

Author

Amir Razak

Versus Trade

Malaysian-born market analyst Amir Razak cuts through the noise every week, breaking down Versus Pairs and explaining what is really driving one asset ahead of another.