Week ahead – ISM services PMI and Fed Minutes to shake Fed hike bets

- Dollar drops on NFP, but rate hike still expected by year-end.

- ISM services PMI and Fed minutes are the greenback’s next catalysts.

- RBNZ expected to raise rates, focus will be on forward guidance.

- ECB minutes, China CPI and Canada’s jobs report also on the agenda.

Fed hike still on the table after disappointing data

The US dollar is finishing the week on the back foot against most of its major counterparts this week, losing the most ground against the kiwi, the franc and the pound.

Despite the pullback, investors remained adamant in their view that the Fed may have to press the rate hike button before the turn of the year. Although oil prices have fallen back to their pre-war levels, the impact of the energy shock resulting from the war in Iran may not have yet been fully transmitted to the broader economy.

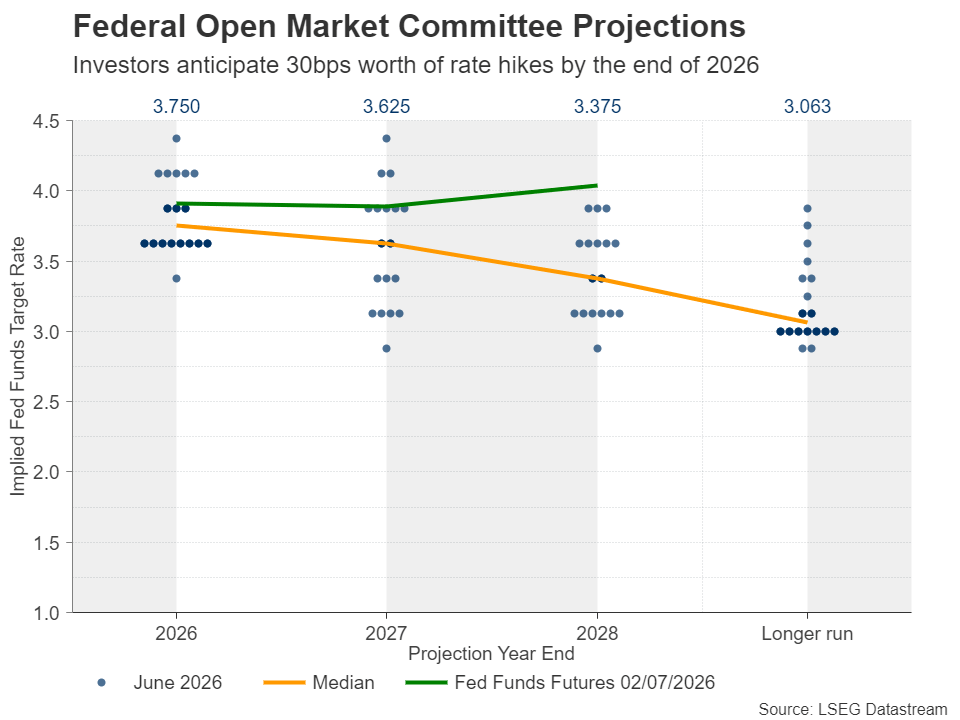

However, the softness in the ISM manufacturing PMI and the surprisingly weak nonfarm payrolls, both for the month of June, have prompted investors to slightly push back the timing of when they expect policymakers to press the rate-hike button. A quarter-point rate hike is now fully priced in for December, while the probability of it being delivered in July has slipped from around 35% to 18%.

What may have allowed investors to maintain some of their hawkish Fed bets despite the weakness in the data and the pullback of oil prices, were remarks by Fed Chair Keving Warsh at the ECB Forum in Sintra, Portugal. The new Fed chief said that he will “disappoint” anyone expecting him and his colleagues to tolerate above-target inflation.

Given that Warsh was appointed by President Trump on the premise that he will be more dovish than his predecessor, Jerome Powell, his remarks sounded as music to investors’ ears. Indeed, when asked about whether Trump may be among those who will be disappointed, Warsh stressed and highlighted that the Fed have been and will continue to be an independent central bank.

ISM services PMI and Fed Minutes enter the limelight

With all that in mind, investors next week will closely monitor the ISM services PMI for June, due out on Monday, as well as the minutes of the latest FOMC meeting, scheduled for Wednesday.

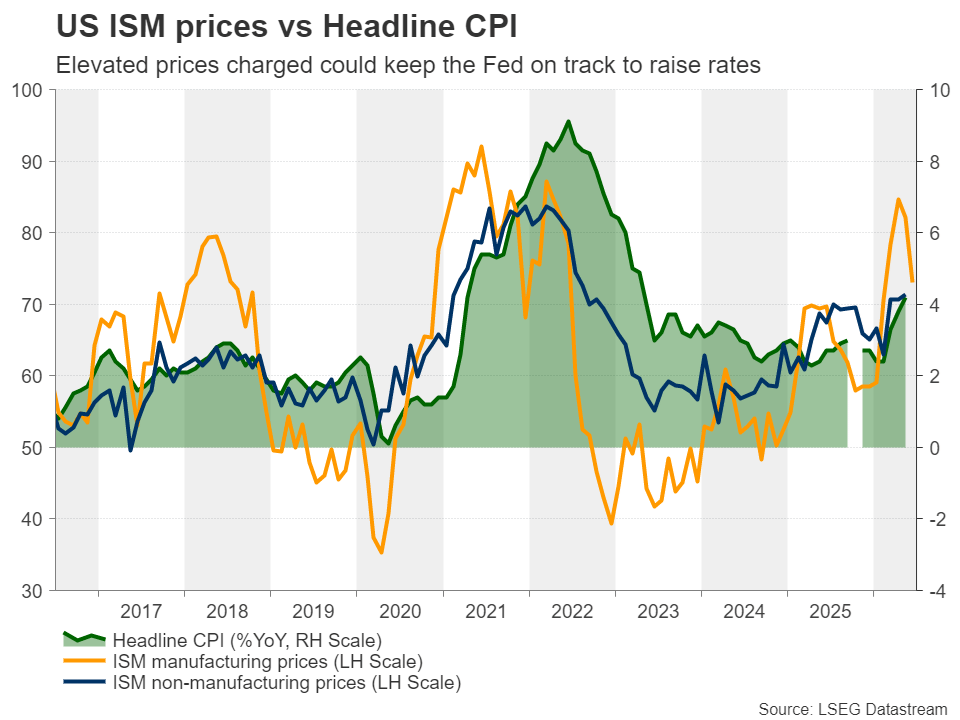

This week, the ISM manufacturing PMI slipped to 53.3 from 54.0, with the prices subindex retreating to 73.0 from 82.1, still an elevated level, which, besides the period of the Middle East war, was last seen back in 2022, when the war in Ukraine erupted. Given that the non-manufacturing sector accounts for around 90% of US GDP, an elevated price subindex in the services survey could revive Fed rate hike bets.

As for the minutes, bearing in mind that the forward guidance was removed from the meeting statement and that Kevin Warch did not submit his interest rate projections, traders will be looking for clues as to whether he is supportive of a rate increase in the coming months.

With 9 members favoring at least one 25bps increase this year, with one voting for three and five members for two, a hawkish message from the minutes could help send Treasury yields and the US dollar up again. At the same time, gold could resume its slide amid a rising opportunity cost, while equities could pull back as a steeper implied Fed rate path could weigh on the present values of high-growth stocks. The opposite may be true if the data corroborates the notion that the Fed should wait a bit longer before deciding to raise interest rates.

Will the RBNZ opt for a hawkish hike?

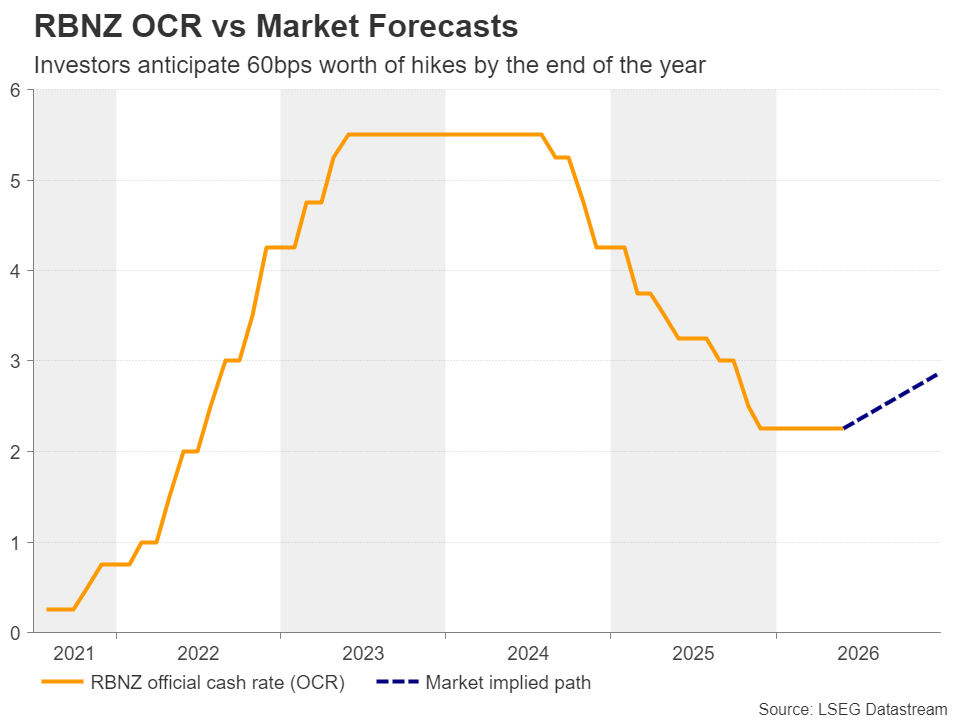

Ahead of the FOMC minutes, during the Asian session on Wednesday, the RBNZ will announce its monetary policy decision. The latest gathering was held on May 27, with the central bank deciding to keep interest rates untouched.

However, the decision was far from unanimous. Three members voted for no changes and three for a rate hike, with Governor Breman’s vote tilting the scale towards keeping rates on hold. That said, the accompanying statement was more hawkish than previously, indicating that rates would have to rise sooner and by more than previously expected due to the upside risks stemming from the Iran-related energy crisis.

Since then, although oil prices have pulled back amid a ceasefire deal between the US and Iran resulting in the reopening of the Strait of Hormuz, incoming data has reinforced the rate-hike case, with the GDP for Q1 coming in better than expected.

According to New Zealand’s Overnight Index Swaps (OIS) market, there is a strong 80% chance of a quarter point rate increase at this gathering, while another two same-sized hikes are nearly fully priced in by February. Thus, for the kiwi to continue flexing its muscles, a 25bps hike on its own may not be enough. The Bank may also need to sound hawkish enough to satisfy market expectations of more increases in the months to come.

ECB minutes, China CPI and Canada jobs data

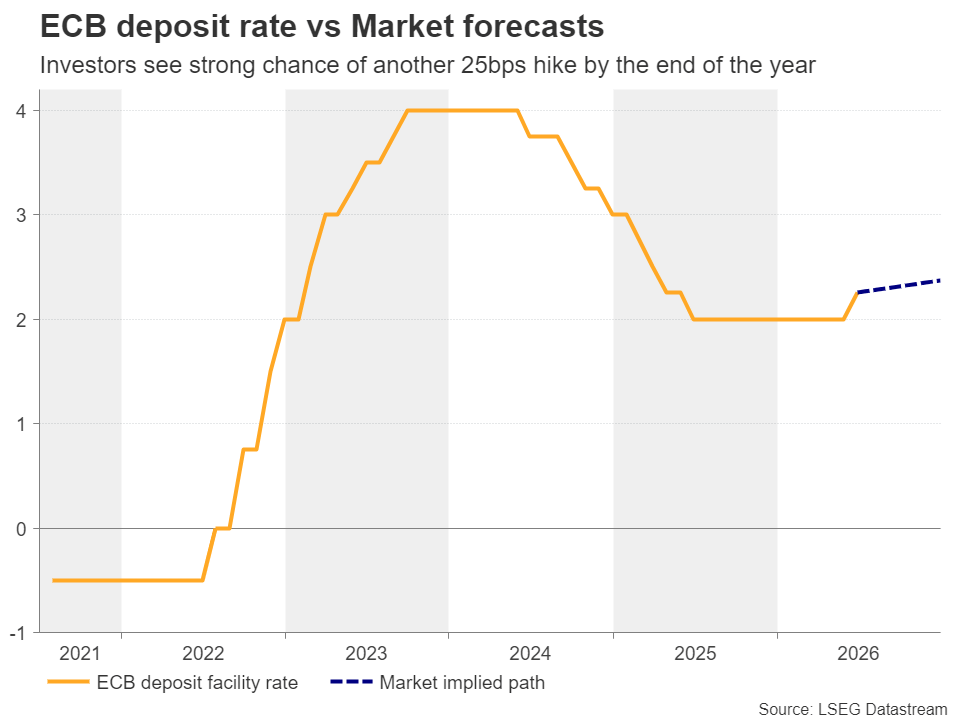

On Thursday, the ECB will release the accounts of its latest meeting, when officials decided to raise interest rates by 25bps, taking the deposit rate up to 2.25%, and revised their inflation projections higher. Although the overall tone was hawkish, officials highlighted a data-dependent approach moving forward.

Market participants are now assigning a 30% chance of a rate hike at the upcoming meeting later this month, and thus, they may be eager to find out whether they are correct in doing so. Should the minutes reveal that officials had no reservations proceeding with a back-to-back hike if needed, that probability could go higher, providing some support to the euro.

Elsewhere, ahead of the ECB minutes, China’s CPI and PPI data for June will come out, while on Friday, Canada will release its jobs report for the same month. The loonie has been suffering since the beginning of May, feeling the heat of falling oil prices and the BoC’s neutral policy stance. It will be interesting to see whether a strong jobs report could allow for a relief bounce.

Author

Charalampos joined Trading Point in August 2022 as a senior market analyst. He has extensive experience in analyzing financial markets, gained through a decade-long career, with his primary focus being on the currency market.