US/China trade negotiations: Ball is in Trump's court

Outlook:

We have several viewpoints from which to watch the FX market Standard relative economic data, including growth and inflation External geopolitical forces that may precede Contagion in emerging markets (Turkey, Venezuela/oil, Iran) A one-time Shock that pinballs all over the place and has unintended effects On the standard stuff, we still await US CPI as an important factor that will influence the Fed's thinking or at least the Fed's rhetoric. As noted yesterday, the trade war is going to subtract 0.3% (or more) from US GDP but how much effect will it have on inflation? We can't find anyone willing to give an estimate. But it is not zero.

On the EM contagion story, conditions are worsening in all three places but we have yet to see any meltdowns, although holders of Turkish lira would probably disagree. See the chart. The red line is the 200-day moving average. As for the one-time Shock, Trump is the gift that keeps on giving. We had the shock, we got over it, and now Trump punches everyone in the face again. Is Trump just engaging in some kind of negotiating game?

Again we have to say Trump can't play checkers, let alone chess. We see one plausible explanation: he got annoyed by something and blew his top. Maybe China really did try to weasel out of a commitment or reword a commitment in such a way as to favor their own position but got caught. It's hard to imagine Trump read anything, so somebody told him, risking the outcome we got to save his job. If China really is guilty, that would account for the Chinese negotiator being the one to return this week. He can bow and scrape and apologize. It's an embarrassment for China, perhaps, but better than walking out.

Both sides have been accused of being close to walking out, but now that ball is in Trump's court. If the 10% tariff is not removed and instead increased to 25% on Friday, as planned, this is tantamount to the US bullying China at the point of a gun. It totally ruins the US reputation. At the same time, it's a loss of face for China. How can they spin it? It might not be wise to poke the tiger. China can't retaliate with tariffs, but as everyone noted last year when this thing started, retaliation can take many forms. Trump is making an outright enemy out of the world's second largest economy. That can't end well.

Another explanation is more convoluted—that Trump needs an excuse to push for fiscal spending—that $2 trillion infrastructure plan he made with the Dems (that has fallen below the radar), plus goading the Fed into a rate cut. The Fed named "uncertainties about trade" as a factor staying its hand for a hike, so once the uncertainties become a certainty, does that make it a factor for easing? Well, maybe. A Fed rate cut has the effect of delivering something Trump wants, a weaker dollar.

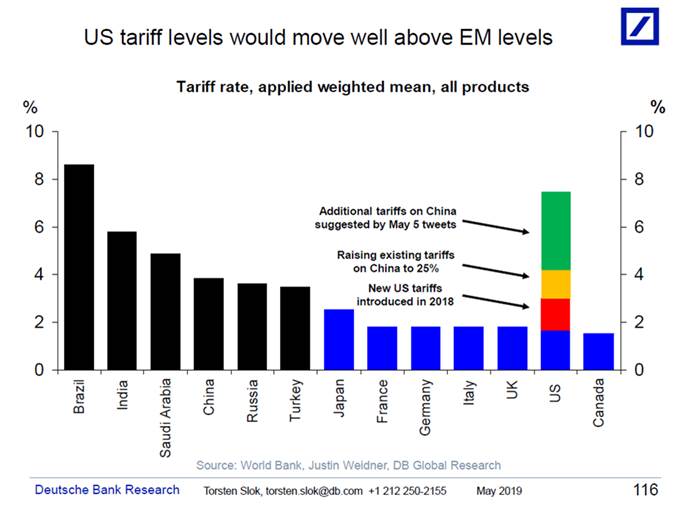

John Authers, who moved from the FT to Bloomberg, has a dandy chart showing the US is now on a par with emerging market countries. How do emerging market economies operate? Tariffs, overborrowing, default, devaluation. Trump is turning back the clock. It has a certain smell of plausibility. The only problem is that it imputes a chain of logical thinking while we think we know Trump can hold only one idea in his head at a time.

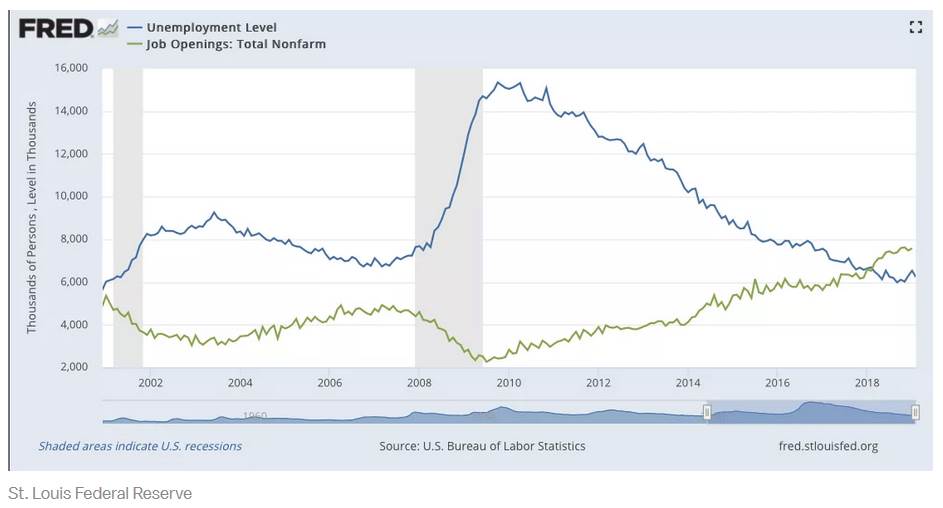

Tidbit about Jobs: In speaking with a non-economist over the weekend, we were reminded of a wrinkle in the US jobs data that doesn't get as much attention as it should. Where are all those new workers coming from to fill 263,000 new jobs in April? Because of baby boomers retiring, the total available pool of labor is contracting. How can it be that the participation rate is relatively steady around 62.8% and the employment to population ratio is steady at 60.6%? If the unemployment rate is a mere 3.8%, where is that pool of unemployed? Companies complain there is a labor shortage and yet every month we get high new jobs numbers.

See the Fed's chart of unemployment vs. job openings. It has reversed for the first time in decades—more jobs than workers. We get JOLTS today, so the chart will shift a little, but the underlying question is not getting answered—where are those workers coming from? We have an all-too-obvious answer, when you think about it—there is a vast number of potential workers not being counted. They are unemployed or employed off the books, not looking, and not receiving benefits that would include them in the count. Drive around any town and you see a lot of able-bodied persons walking around, not "working." What proportion are black or gray market—working off the books? Nobody knows, certainly not the Bureau of Labor Statistics. For this reason, we do not expect average wages to rise all that much. These may be unskilled sub-par workers with bad habits, but they are fairly cheap.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a free trial, please write to [email protected] and you will be added to the mailing list..

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat