The Oil shock boosts Norway’s $2 trillion fund – but there’s a catch

A crisis that should make Norway richer could also put pressure on the very fund built to protect its future wealth. The irony is hard to miss.

The latest Middle East crisis is creating a strange contradiction for Norway’s giant sovereign wealth fund.

As tensions around Iran and the Strait of Hormuz continue to shake global energy markets, Oil prices have surged, boosting revenues for one of the world’s largest petroleum exporters. Yet the very same shock lifting Norway’s energy income is also threatening the value of the country’s massive investments across global equities and bonds.

That tension sits right at the heart of Norway’s Government Pension Fund Global (GPFG), better known as the Norwegian Oil fund.

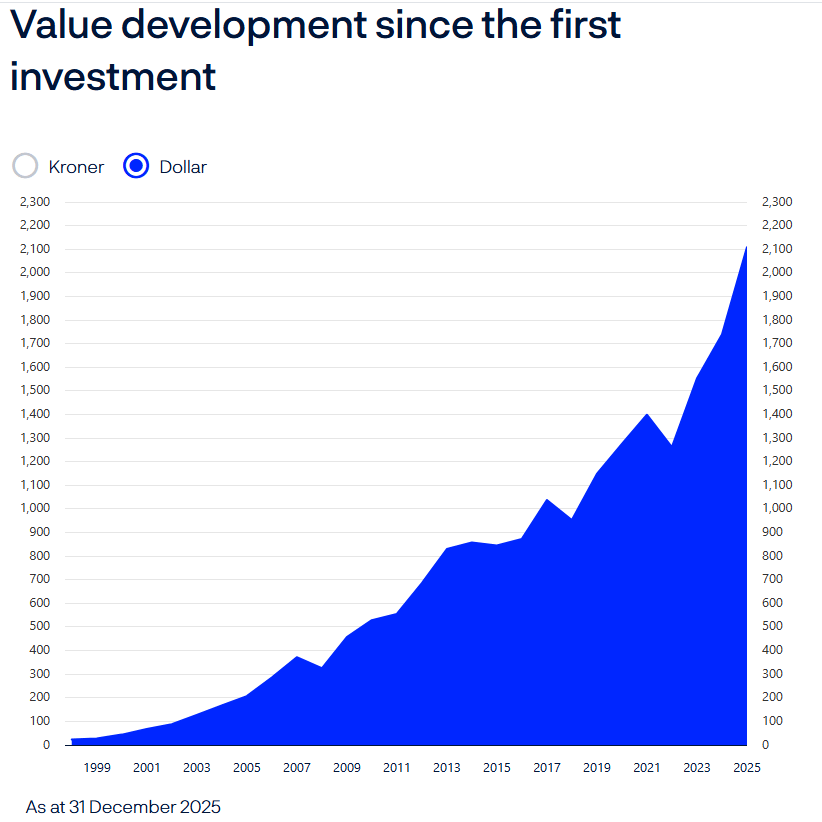

At more than $2 trillion in assets, the GPFG is not only the world’s largest sovereign wealth fund. It is also one of the biggest investors on the planet, with stakes in thousands of companies worldwide.

And right now, it is being pulled in two completely different directions.

Oil prices are rising, and Norway benefits

The renewed instability in the Middle East has once again reminded markets how fragile global energy flows can be.

The Strait of Hormuz remains one of the world’s most important Oil chokepoints, with roughly a fifth of global crude flows normally passing through it. Any disruption there immediately raises fears of tighter supply, higher transport costs and another inflationary energy shock.

That alone has been enough to inject a sizeable geopolitical premium into Oil prices in recent weeks, with Brent remaining extremely sensitive to every headline linked to Iran, US diplomacy and regional security risks.

For Norway, the first impact is straightforward: Higher Oil and Gas prices mean stronger export revenues, larger tax receipts and more money flowing into the country’s petroleum wealth machine.

Norway’s crude Oil exports reportedly jumped nearly 68% YoY in March, while average prices climbed to their highest levels since late 2023.

At first glance, it looks like Norway is once again cashing in on an energy shock, but the reality is far more complicated.

The Oil fund is no longer really “an Oil fund”

This is where the story becomes much more interesting.

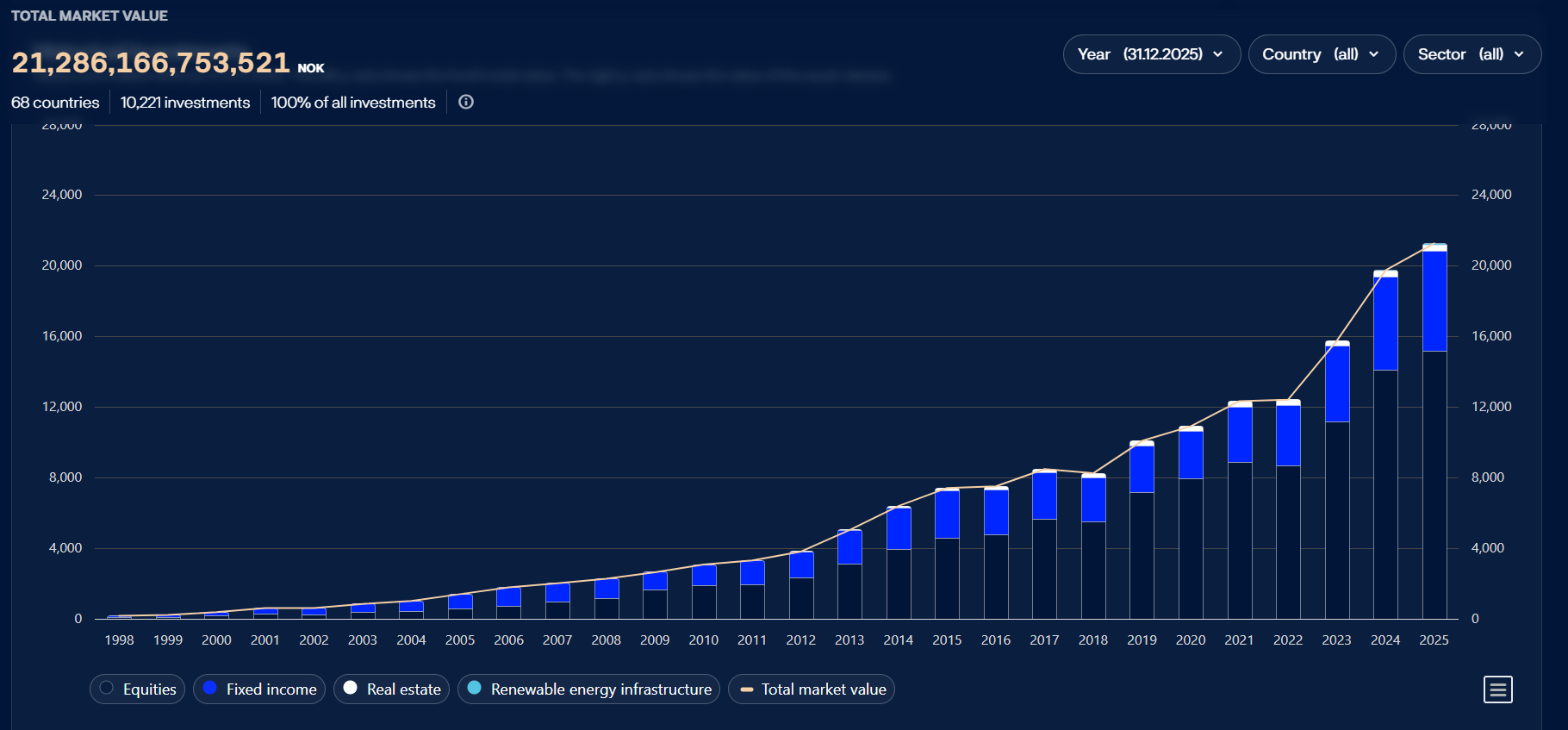

Despite the nickname, the GPFG is no longer simply a giant pot of Oil money sitting on energy investments. Over the years, Norway transformed its petroleum revenues into a massive global portfolio spanning equities, bonds, real estate and renewable infrastructure.

Equities alone account for more than 70% of the fund.

That means the fund is deeply tied to:

- global growth,

- investor sentiment,

- interest rates,

- inflation expectations,

- and the overall health of financial markets.

And that is where the paradox appears: the same Oil shock boosting Norway’s revenues could also hurt the value of the fund itself.

If crude prices continue climbing because of geopolitical tensions, the knock-on effects for markets could become increasingly painful. Higher energy costs feed inflation, pressure consumers, squeeze corporate margins and make life much harder for central banks already struggling to bring inflation back under control.

For a fund heavily invested across global markets, that matters enormously.

The bigger fear is inflation

The Middle East crisis is also reviving fears of a broader stagflationary environment, where slower growth collides with stubborn inflation.

Oil shocks rarely stay confined to energy markets. They eventually spread into transport, manufacturing, logistics and household energy bills. In turn, that can force central banks like the Federal Reserve, the European Central Bank and the Bank of England to keep interest rates higher for longer.

And markets do not particularly like that combination.

Higher yields hurt bonds, tighter monetary policy pressures equities, and weaker growth damages earnings expectations. The GPFG is exposed to all of it.

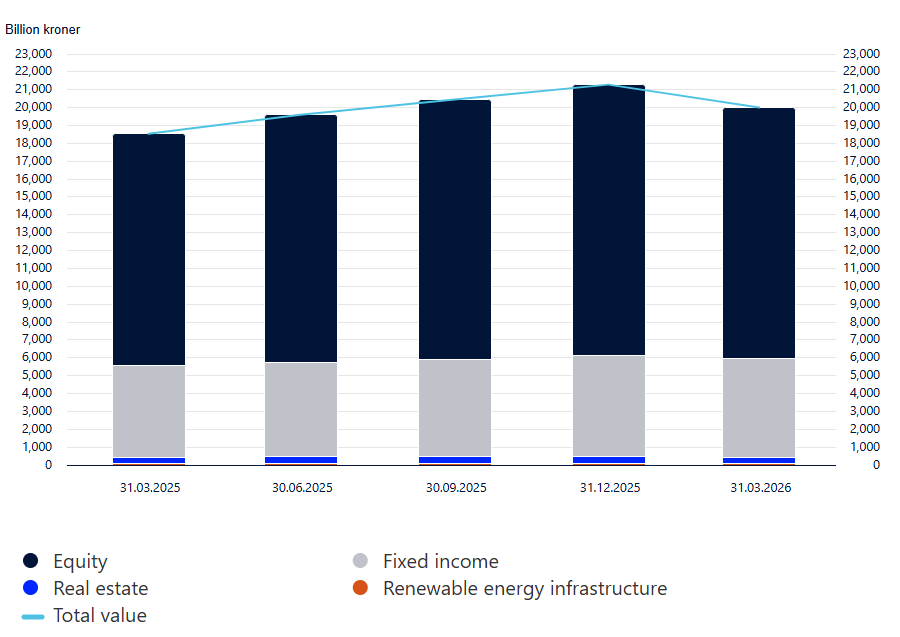

In fact, the fund already reported a negative return of 1.9% in the first quarter as equities and fixed income came under pressure.

That does not mean the fund is in trouble. Far from it. Its entire structure was designed to absorb long-term volatility.

But it does highlight something important: higher Oil income does not automatically translate into higher returns for the Oil fund itself.

Norway’s uncomfortable advantage

Few countries sit in a position quite like Norway’s.

The country benefits financially from higher energy prices at a time when much of the global economy suffers from them. Yet because the GPFG is so deeply embedded in international markets, Norway cannot fully escape the broader damage created by geopolitical turmoil.

That is what makes the fund such a fascinating symbol of the modern global economy.

Norway profits from the Oil shock while simultaneously absorbing the financial consequences of the same crisis through its investment portfolio.

The irony is difficult to ignore.

Norway created the GPFG to transform a finite natural resource into a permanent financial asset for future generations. It became one of the clearest examples of how to avoid the so-called resource curse.

But today, the fund’s greatest strength, its global diversification, also means it is exposed to almost every major shock hitting the world economy.

Bottom line

The Middle East crisis is not just another energy story: it is a reminder that even the world’s largest sovereign wealth fund cannot fully isolate itself from a global Oil shock.

Norway may become richer in petroleum terms as crude prices rise, but the GPFG’s vast exposure to global markets means the country is also tied to the inflation fears, volatility and slower growth that come with it.

That is the real paradox behind Norway’s oil fortune.

The same crisis generating the windfall could also end up damaging the fund built on it.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.