US-Iran talks: The next 60 days will decide where Oil prices go next

Oil markets received some encouraging news after weeks of rising tensions in the Middle East. But let’s not get ahead of ourselves: we’re far from victory, and markets just seem to have priced out the worst-case scenario.

The US and Iran have reportedly made "substantive progress" in talks in Switzerland and agreed on a framework for working toward a broader deal within 60 days. The discussions, mediated by Qatar and Pakistan, also resulted in plans for technical working groups, a direct communication channel between both sides and a mechanism designed to prevent incidents in Lebanon while helping keep the Strait of Hormuz open.

The developments brought a welcome change of tone for investors.

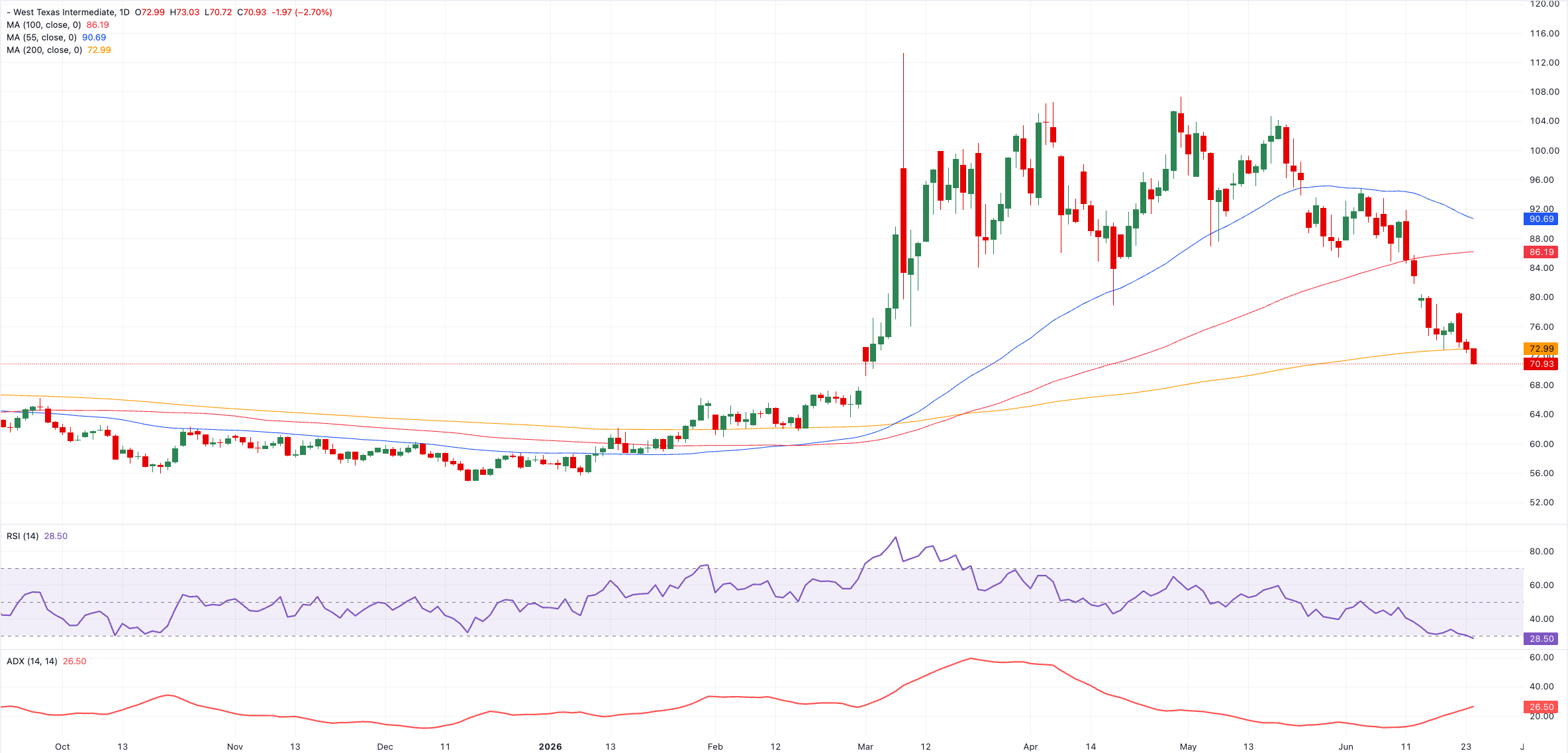

In recent weeks, Oil prices had been adding a hefty geopolitical risk premium, amid fears the conflict could escalate further and threaten one of the world's most important energy chokepoints. As details of the talks emerged, however, that premium began to unwind, with Brent and WT crude reversing earlier gains as traders reassessed the likelihood of a major supply disruption.

Yet despite the positive headlines, markets are far from declaring the crisis over.

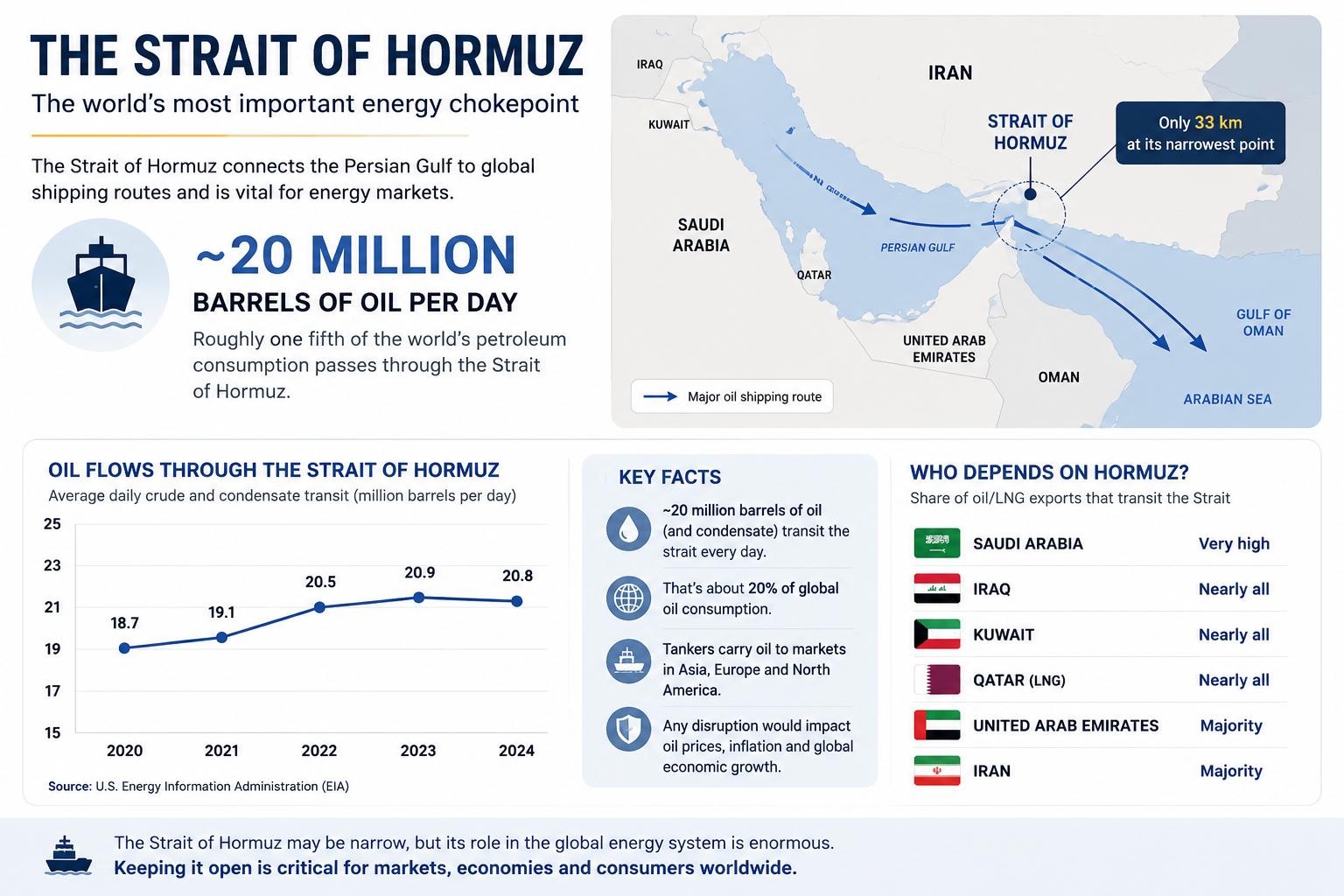

Why the Strait of Hormuz matters

The Strait of Hormuz remains the single most important factor for energy markets.

The narrow waterway connects the Persian Gulf to global shipping routes and handles roughly a fifth of the world's Oil trade. Any disruption, as markets have seen in recent months, has immediate consequences for crude prices, transportation costs and inflation expectations worldwide.

That explains why markets reacted so sharply when Iran suggested over the weekend that the strait could be closed again following renewed Israeli military operations in Lebanon.

But those fears evaporated once talks resumed and oil kept flowing, though the episode was a reminder of how quickly sentiment can shift.

For traders, the difference between an open Strait of Hormuz and a closed one is the difference between a manageable geopolitical dispute and a global economic shock.

The Strait of Hormuz is open, but normality has not fully returned. Shipping traffic remains below pre-war levels, reminding investors that tensions in the region have not disappeared. Even so, the latest data offer reasons for optimism. According to Kpler, 37 commodity carriers crossed the strait on Monday, the busiest day since the conflict began in late February and a sign that confidence may slowly be returning to one of the world's most important trade routes.

Markets are removing risk, not pricing peace

One of the most common misconceptions surrounding geopolitical events is that falling Oil prices automatically signal confidence that a conflict has been resolved.

That is not what markets are saying today.

Instead, investors appear to be reducing the probability of the worst-case scenario.

The talks have lowered fears of an immediate escalation involving shipping routes and regional energy infrastructure. Oil tankers continue to move through Hormuz, supply chains remain intact and there is now at least a diplomatic framework that both sides appear willing to explore.

Those developments are enough to justify some reduction in the risk premium that had built into crude prices.

But they are not enough to convince investors that lasting stability has been achieved.

The situation remains very fragile

In many ways, the recent events highlighted both the opportunities and the risks facing negotiators.

At various points, Iran signalled that Hormuz could once again become a point of pressure. Israeli military activity in Lebanon added another layer of uncertainty, while President Donald Trump reiterated that the United States would respond militarily if Iranian-backed groups continued attacks against Israel.

For a brief period, it appeared as if negotiations could break down altogether.

The fact that talks ultimately resumed and produced a constructive outcome helped calm markets on Monday, but the sequence demonstrated how fragile the path forward remains.

Diplomacy may be advancing, yet the underlying geopolitical tensions that created the crisis have not disappeared.

The next 60 days may matter more than the last 60 hours

The roadmap agreed over the weekend is just the beginning.

Investors will now focus on whether technical negotiations can deliver a more comprehensive agreement and whether both sides are prepared to follow through on their commitments.

Several questions remain unanswered: Can Iran restrain proxy groups operating across the region? Will Israel avoid hurting diplomacy? Can the Strait of Hormuz remain fully operational during negotiations?

And perhaps most importantly for energy markets, could a successful agreement eventually allow additional Iranian Oil to reach global markets?

The answers will shape not only Oil prices, but also inflation expectations, central bank policy and broader market sentiment in the months ahead.

To sum up

The framework agreement represents the most constructive step toward de-escalation in months and has given investors a reason to become more optimistic.

However, optimism should not be confused with certainty.

Markets are no longer pricing an imminent supply shock, but neither are they pricing a lasting peace. The recent decline in Oil prices reflects a reduction in geopolitical risk rather than the complete disappearance of it.

For now, diplomacy has bought the market some breathing room. Whether it can deliver something more durable remains the question that traders, policymakers, and consumers will be watching closely over the next two months.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.