The Fed must be watching Japan with fascination

The most notable thing yesterday was the stock market liking the delay in the huge tariff on Europe. This is pretty dumb. It means a rushed deal will be terrible for the euro but not real in any legal or economic sense. Besides, if Europe does balk at Trump demands, the 50% tariff goes right back on, meaning disruption all over the place.

The press has some fun with finger-wagging at TACO—no, not transfusion-associated circulatory overload bur rather Trump Always Chickens Out, something devised by the FT and picked up by the NYT and others. Trump pretends his on-again/off-again tariff moves are “strategy,” but everyone knows he doesn’t have a clue and is just winging it.

As noted above, the WSJ top headline is “Wall Street Bets the Worst of Trump’s Trade War is Behind It.” That’s exactly what Trump wants Wall Street to think—despite his protests, he really is afraid of causing a stock market meltdown. The paper says investors are hopeful deals will get done with little lasting damage to the economy—the epitome of wishful thinking.

We should keep in mind that it’s Congress that has the power of the purse, aka the ability to set taxes. Trump usurped that power by using an “emergency” authorization. It will get to the Supreme Court one of these days and alas, the Court will likely side with Trump. After all, the trade deficit is horrendous. The Trump case “should” have to include the national security aspect but the Court shies away from getting down in those weeds.

Another aspect of the trade debacle is that the treaties Trump is breaking are legal contracts. We know he disdains legal contracts and broke many while building stuff, driving contractors to court and into bankruptcy. We await some kind of blowback for failing to honor contracts. We already know the US reputation risk has hit bottom, but will there ever be consequences for Trump?

Off on the side in the bond market, the Fed must be watching Japan with fascination. After a mini-crisis earlier this week in which longer-term yields soared and prices tanked, setting off the same thing around G7 markets, Japan’s response was to propose lesser issuance at the longer ends. One analyst said “Japan would be a test case for the entire world on the best way for governments to handle ‘signs of stress or a mismatch between supply and demand.’” This is hardly a new idea but the speed and specificity of the response is very rare.

And to be fair, the issue is not going away. The 40-year bond auction overnight was not at all well received and analysts point out that when your yields are 2.9% (30-year) but inflation is 3.6%, you’ve got a mismatch. Investors demand some term premium. As we have seen for years now, the central bank needs to raise rates and yet nobody is forecasting any such thing until much later in the year.

Today we get the minutes of the Fed minutes from May 6-7 meeting. We tend to think minutes are too little, too late and this time what can they say except something like “excessive uncertainty?” Believe it or not, the other top story is Nvidia earnings. We also get two regional Fed survey results but these almost never move the FX market.

Inflation reports from the eurozone are coming in soft. The ECB is paractically certain to but rates next week. But that’s not the story. The real story is ECB chief Lagarde making it clear that she really wants the eurozone to grab the opportunity Trump is handing it on a platter to take over as the top currency. She pointed out "when doubts emerge about the stability of the legal and institutional framework, the impact on currency use is undeniable.

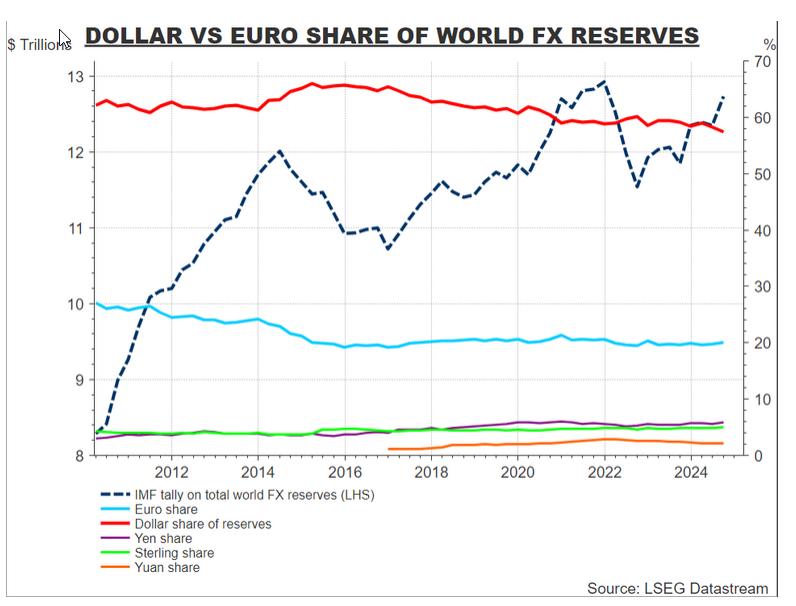

"These doubts have materialised in the form of highly unusual cross-asset correlations since April 2 this year, with the U.S. dollar and U.S. Treasuries experiencing sell-offs even as equities fell. The EU has a legitimate reason to turn its commitment to predictable policymaking and the rule of law into a comparative advantage.”

It will take considerable reforms to permit the EU to seize the opportunity [as former ECB chief Draghi said]. This includes overcoming German resistance to combined euro assets. Weirdly, Trump may not care. It would take a gigantic drop in the dollar to even begin to fix the trade deficit, and he fails to see the corresponding benefits of being the global reserve currency, like the ability to fund his over-spending.

See the chart from Reuters. Ms. Lagarde has a long row to hoe. At this point, we suspect ambitions to become the top player are wishful thinking (if only because Europe is the place that warred with one another for millennia and started two world wars). But a bigger player? You bet. Lagarde has issued a call to action.

Forecast

The dollar recovery has almost no facts behind it. It’s mostly sentiment and sentiment influenced heavily by things like stock market benchmarks. This time we have the 10-year/Bund yield widening in the US favor but it’s nothing to write home about.

Not to be a broken record, but tigers and stripes. Trump is damaging the US economy and social cohesion and legal system in multiple ways and delivers another offense every single day. The mood is severely anti-dollar and one of the few market dynamics in its favor is plain-old position adjustment. We expect the dollar upmove to fizzle this week.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat