The fall in private business activity may bottom up in February with ECB keeping rates on hold for longer

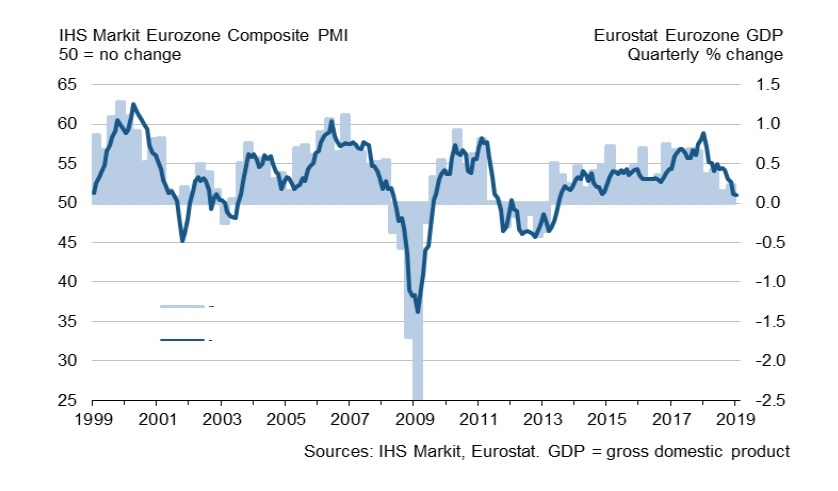

- The Eurozone manufacturing activity gauge, the purchasing managers’ index (PMI) is expected to remain at 50.5 in a flash reading for February, unchanged from the previous month.

- The services PMI is also expected to remain unchanged at 51.2, with the composite PMI seen ticking up to 51.1 in February.

- The German investors’ sentiment indicator from ZEW Institute improved marginally n February to -13.4 with current situation assessment deteriorating sharply.

- The EUR/USD is expected to see a little reaction to the Eurozone PMI data as worsening economic situation is already fully priced in with the ECB changing its interest-rate guidance if it becomes clear the situation isn’t temporary.

The Eurozone composite PMI for February is expected to tick up to 51.2 after falling to the lowest level since November 2014 in January of 51.1. Both manufacturing and services PMIs are expected to remain at unchanged levels in a sign of further economic deterioration in economic activity as global trade tensions weigh of confidence, new orders, and exports.

The leading indicator of investors’ sentiment from the German ZEW Institute saw a marginal improvement in February with a reading of -13.4, up from -15.0 in the previous month, but the current situation sub-index saw further slump by 12.6 points to a level of 15.0 points.

“The figures for industrial production have once again seen a decrease, incoming orders are stagnant and foreign trade currently provides no fresh impulses. All of this is reflected in the fact that the assessment of the current situation has experienced a considerable decline. For the next six months, the financial market experts in our survey do not expect any improvement,” ZEW President Professor Achim Wambach wrote in the report on February 19.

Global economic slowdown caused by the monetary policy tightening in the US and the US-China trade tensions both saw the business confidence deteriorating globally for some time already.

The fact that the Eurozone economy is slowing down is well reflected in the ECB policymakers public statements with the financial markets moving its expectations for a rate hike in the Eurozone well into 2020 from the third quarter this year.

The ECB Governing Council member and governor of Banque de France Francois Villeroy de Galhau said on Sunday for El Pais that the slowdown of the European economy is “significant” and the ECB could change its interest-rate guidance if it becomes clear the situation isn’t temporary.

This indicated that the new wave of support measures are going to be implemented by the ECB with the targeted longer-term refinancing operations (TLTROs) being the most likely option as indicated last week by the ECB executive board member Benoit Coeure.

The Eurozone composite PMI and the GDP growth

Author

Mario Blascak, PhD

Independent Analyst

Dr. Mário Blaščák worked in professional finance and banking for 15 years before moving to journalism. While working for Austrian and German banks, he specialized in covering markets and macroeconomics.