The economy doesn’t care who feeds it stimulus, monetary or fiscal policy – as long as it gets Fed

Outlook: The top news items today are Canada’s Sept CPI and the Beige Book, punctuated by Fed speeches. Note that Canadian CPI is expected higher at 4.3% from 4.1% in August, if core CPI unchanged, and the BoC not likely to let it go unmentioned at the policy meeting next Wednesday.

In the US, we still have a big minority who complain about growth not sustaining itself, whether from Covid, labor market constraints or supply problems, leading to the deduction that the Fed should be in easing mode, not hawkish, and still throwing cash at the economy. In fact, it could be the Fed itself damaging growth if anticipation of tightening suffices to cut growth expectations (and business and spending decisions based on those expectations).

This argument carries water only if the fiscal side fails utterly and we do not get Biden’s infrastructure spending. The economy doesn’t care who feeds it stimulus, monetary or fiscal policy—as long as it gets fed. (Other sources of stimulus includes foreign direct investment and conversion of low-yield savings into other assets, including housing.) The long-awaited Biden plan might make some progress by end of week and ahead of the month-end deadline as some features will be dropped and others cut back. Once the deal is done, we should expect a mini-surge of renewed optimism about economic growth.

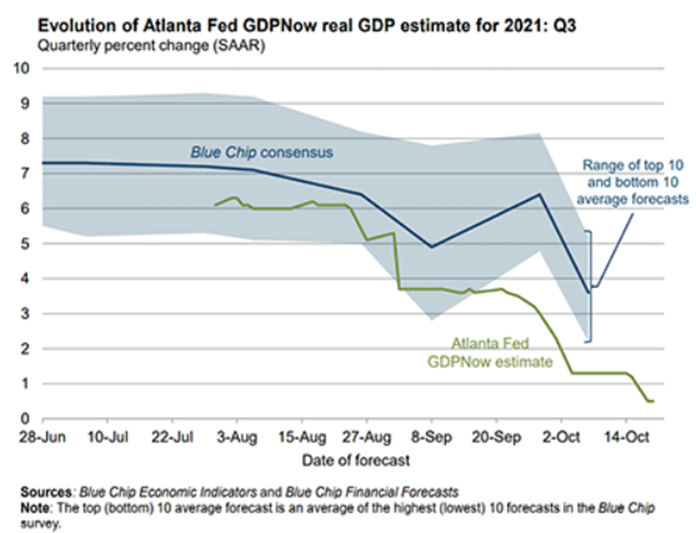

We’re going to need it. While the Atlanta Fed doesn’t take a position on it, the latest GDPNow forecast has Q3 coming in at a dreadful 0.5%. Last week’s 1.2% was bad enough but 0.5%? The reasons for the dismal outlook are personal consumption expenditures growth slipping from 0.9% to 0.4% and real gross private domestic investment growth falling from 10.6% to 8.4%.

Notice that not a single major financial press report names the Atlanta Fed’s GDPNow report. It’s not a market-mover and perhaps not even a market-influencer. We get the actual next Thursday (Oct 28) and the consensus forecast is 3.2%. Trading Economics has 5.1%, and Q2 had been 6.7%, based primarily on the same factors the Atlanta Fed was measuring for its drop (consumption, investment). They had soared in Q2.

So, we should probably consider the scary-low Atlanta Fed forecast an outlier and not the bond market driver. If a majority of the bond gang saw the US economy headed for the drain, they would not persist in selling longer-term paper and driving up the yields. Still, it’s a potential left-field factor and we should keep it in mind. Something else to keep in mind is the blaring headlines about goods shortages in the US that is driving at least some hoarding and early holiday shopping.

Another back-burner factor is mostly political stuff that tends not to affect FX, witness all the UK’s problems that are failing to hold back sterling although sensibility says they “should.” Similarly, the re-jiggering of the Byzantine ECB stimulus packages, long-term and otherwise, might be a small drag on the euro or a small push, but are so complicated and fraught with uncertainty that traders really can’t be bothered. On the whole, too much complexity is a drag. That means, probably, the rise in the euro is a function of traders perceiving an oversold condition, and has nothing to do with the mechanics of QE.

Bottom line, the FX markets is in a state of confusion and uncertainty about what matters, and thus that consolidation/ranginess we saw coming. This state of affairs usually ends with a whimper and not a bang. The point is to avoid losing your shirt until it resolves itself.

Developing themes

-

China is purposefully allowing its own slowdown to take the opportunity to reform its economy away from property and debt. It is risking a global financial crisis to make the point but the markets do not agree that this risk is high, judging from a 4-tenor dollar bond auction that was heavily oversubscribed and delivered yields only a fraction above the US equivalents.

-

The US political system has many faults and one of them is the ability of one party to halt all legislative activity with the threat or practice of the filibuster. This has the power to bring the US economy to a grinding halt and throw it into recession. Getting the Biden infrastructure plans approved will be a respite even if the underlying structural issue does not get resolved.

-

Inflation from commodity price rises and supply chain disruptions as well as bad planning all around (misjudging supply and demand) may become persistent—or may be fixed by 2022, depending on which economists you prefer. Inflation fear is going to cycle from low to high and back to low again many more times. Studies show the public’s inflation expectations are entirely dead wrong and even big finance professionals get it right only 60% of the time.

-

US growth is going to fall from 6.7% in Q2 to 5.1%, or 3.2%, or perhaps as low as 0.5%. Whatever the number, it’s a drop and therefore a drag on sentiment.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat