The Dollar reflects the seeming confirmation of the soft landing

Outlook: US data today includes July PPI and the flash University of Michigan consumer sentiment for August. Yawn. See the chart of core PPI on the monthly basis—no change for a long time. And while the supply chain crisis raised the correlation of PPI and CPI, in the US it’s historically a poor relationship. Still, the forecast for PPI y/y is 0.7%, up from 0.1% in June and core is forecast at 2.3% after 2.4% in June (FT).

One of the most important things about the CPI report is core services ex shelter, something Mr. Powell likes, up by 0.2%, too, Annualized, it’s 2.9% over the past six months. When do we get to the level that is over 2% but close enough to 2% to justify expectations of the end of hiking?

We promised no more tiresome inflation studies but feel obliged to note that the NY Fed’s “underlying inflation gauge” that came out right after the CPI delivers the “full data set" at 3.0%, down 0.2% m/m and the "prices-only" at 2.3%, also down 0.2%. These look better than the official 3.2%.

We also got the expected flood of analysis from the commentariat that bad housing data makes inflation look worse than it really is, plus the most pathetic of efforts from old pal Kudlow that energy prices are going to wipe out all the gains because drill rates are down so far. It’s true that the drill rig count is down 14.08% from a year ago, but that is hardly the only factor affecting US energy costs, including increases in foreign output. Besides, energy accounts for less than 10% of household spending. All the same, energy costs are a risk. Today the IEA said global oil demand is hitting record highs and may move higher in August.

Assuming that we are hardly alone in having detected that “true” inflation is far below the headline, we need to ask why the dollar recovered so smartly after the knee-jerk spike low. It looks like Bloomberg hit that nail on the head with the headline—“Fed Seen Pausing After Tame CPI Data, but Mission not Over.” The FX market seems to be pricing in one more hike, even if it’s delayed to Nov after a pause in September.

Somewhat weirdly, the CME FedWatch tool shows a probability of only 26.2% for another hike in November and this is down from earlier periods. Maybe FX is the only market that sees it? But that seems silly, and we are still in a trading range against the key currency, the euro. That’s assuming a non-superficial view of the data. On the surface, it does appear that the US fight against inflation did stall in July.

Here's the funny part—the ECB may pause in September, too. A Reuters poll shows 37 of 70 economists (53%) expect no move at the Sept meeting but the same percentage see rates up by 25 bp year-end to 4.0%. This is “fine-tuning” since nobody expects inflation at the target 2% until 2025 at the earliest. Fun tidbit: “If the ECB hikes once more as the consensus view narrowly predicts, that would mean the highest deposit rate since the euro was introduced in 1999…”

Similarly, Reuters Australia might be in an ever better boat. RBA chief Lowe told the press overnight” policy is in the ‘calibration stage’ as the worst was over for inflation, though some further policy tightening might be needed depending on incoming data and evolving risks.”

The one place where the central bank will likely remain on the warpath is the UK. The FT reports “Markets are pricing in a 70 per cent probability of a further quarter-point increase in September and a 30 per cent chance of a pause. Last week the central bank slowed the pace of its tightening cycle, lifting interest rates by 0.25 percentage points to 5.25 per cent.”

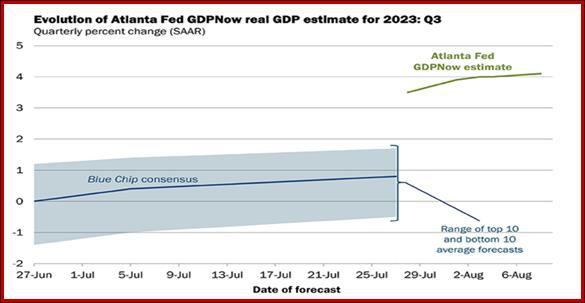

Tidbit: Keep in mind that the Atlanta Fed keeps upping the ante on growth, at 4.1% at the last reading (Aug 8) and another nowcast next week (Aug 15). This outpaces all the rest of G7 by a mile.

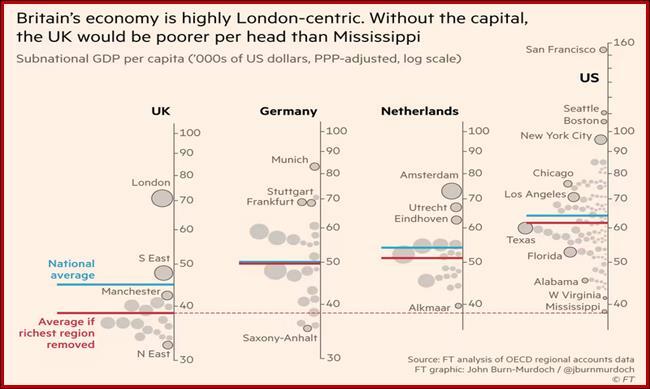

Tidbit 2: The FT has horrid story on the underlying sub-par performance of the UK economy that leaves it, ex-London, as poor as Mississippi. See the chart. The FT struggles to deny it and points out that other key cities elsewhere in the world have a similar effect, but nowhere as much as the UK.

“It will surprise nobody that London accounts for an outsized share of Britain’s output, but the magnitude of the UK’s economic monopolarity is remarkable. Removing London’s output and headcount would shave 14 per cent off British living standards, precisely enough to slip behind the last of the US states. Britain in the aggregate may not be as poor as Mississippi, but absent its outlier capital it would be.

By comparison, amputating Amsterdam from the Netherlands would shave off 5 per cent, and removing Germany’s most productive city (Munich) would only shave off 1 per cent. Most strikingly, for all of San Francisco’s opulent output, if the whole of the bay area from the Golden Gate to Cupertino seceded tomorrow, US GDP per capita would only dip by 4 per cent.”

Forecast: The dollar reflects the seeming confirmation of the soft landing, with former Fed Gov Meyer saying inflation fell far faster and further than anyone expected. Even hawkish current Fed Waller said a series of 0.2% increases would suffice to consider inflation well on its way to the target.

The problem with getting what you want is you don’t know where to go from there. This is what we see in the flattish US equity markets—everyone who was going to buy has already bought. The implication is a sideways move ahead, and we may project something similar for the dollar.

Bottom line, we have rate expectations pretty much lined up, plus GDP growth outlooks, with the US far ahead of all the other developed countries. This leaves risk sentiment stewing in its own juices. Not to be snide, but markets prefer crises or at least surprises on which to trade. “Normalcy” spells boring sideways price moves on the balance of risk-on/risk-off. Even what appears to be a fairly serious situation in China is being downplayed as a risk-off development. In this environment, we should expect profit-taking and the dollar falling back on gravity alone, no sentiment needed.

We might get something from Jackson Hole, scheduled for Aug 24-26 and on the topic of "Structural Shifts in the Global Economy."

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat