Banking Crisis: Is it a true crisis or just some overly aggressive players?

Outlook: Today we get the minutes of the Sept FOMC and the PPI data, but both will be seen through the lens of tomorrow’s CPI. As we all know by now, the headline CPI is forecast at 8.1% from 8.3% the month before, but core is expected higher at 6.5% from 6.3%. As usual, analysts will remind us that the Fed doesn’t look at CPI when making decisions, but rather the PCE version, but the public does look at it and behind closed doors, so does the Fed.

It’s not inconceivable that “higher inflation” is already priced in and the actual release will see a burst of profit-taking on long dollar positions.

The dollar is too strong. The interesting currency today is the dollar/yen, which hit 146.50 overnight, surpassing the level at which the BoJ intervened last month and a new 24-year high. The dollar also hit a 2½-year high against the CAD.

The press contains several stories about how the strong dollar harms multinational corporation earnings. As the Brazilian finance minister complained several years ago when the dollar was high, the US is “exporting inflation” and harming emerging markets that had borrowed in dollars—a currency war. This assumes the State Dept could influence the Treas Dept and the Fed to manage things to favor EM’s instead of domestic conditions, but never mind.

The Treasury claims it considers other countries as it observes the FX market, but in practice, “observe” is all it does. The dollar “belongs” to the Treasury, not the Fed, and it’s unthinkable that TreasSec Yellen would call up Fed chief Powell and ask for lesser rate hikes because some EM’s are having trouble paying their bills. If and when some poor place can’t afford to buy food, then the State Dept steps in and organizes some food donations. It’s less than ideal, to say the least, but then, capitalism is heartless.

And just as TreasSec Rubin said decades ago (“A strong dollar is in the US’ best interests”), Yellen said her own version “A market-determined value of the dollar is in America’s interest. The currency movements are a logical outcome of different policy stances.” Hidden behind this reprise of the Rubin mantra is the message that (1) the US will not intervene to cap the dollar because it’s not in the US’ self-interest and (2) do not expect a coordinated effort like the Plaza Accord, which worked all too well in corralling the dollar and had to be reversed by the Louvre Accord a few years later.

As we periodically note, Paul Volcker wrote an outstanding book (Changing Fortunes) about government meddling in FX. He made some remarks still ringing in the ear. First, that a weak currency is not the signpost of a successful and strong economy and should not be sought. Second, stuffed shirts may agree around the table but when it comes to executing rate changes to manipulate FX, hardly anyone obeys. In the Plaza Accord situation, only Japan made the rate changes called for. Europe made promises it did not keep. It’s a bit like any other dysfunctional cartel—it lacks an enforcement mechanism.

The upshot: grin and bear it. But also pare long dollar positions.

Banking Crisis: It’s not clear whether there is a true crisis or just some overly aggressive players. Credit Suisse keeps coming under attack.

Actual solvency is the core issue, but liquidity counts, too, and is sometimes the tip of the spear. Yesterday the NY Fed reported that the Swiss National Bank tapped it for $3.1 billion. The SNB doesn’t offer an explanation but one is that the other Swiss banks (or other European banks generally) are not in the mood to lend to Credit Suisse, which needs the dough, possibly to cover losses on interest rate or FX positions.

One expert couched it more frankly—to prevent a run on Credit Suisse a la Lehman. When a bank is in trouble, its fellow banks either jack up the cost of lending or refuse altogether. The mere fact of CS probably borrowing from the SNB and the SNB borrowing from the Fed doesn’t tell you anything about the actual condition of CS—just that the other banks are not willing to lend to it or only at high cost. Do they know something? If so, they are certainly not telling.

The Bank of England is still being criticized, this time for giving the pension funds to Friday to clean up their act (with the fund association begging for more time).

So then the question becomes whether the BoE might be calling on swap lines at the Fed, too. Gee, two major central banks, and not some benighted, incompetent backwater names, either. We are confused about why the funds don’t just dump their gilts instead of trying to maintain unaffordable hedges.

The pension funds are not the only vulnerable parties. The BoE released that on 9/30 it had met with the Financial Policy Committee, which warned that fresh drops in asset prices together with credit risk concerns could set off a liquidity crisis in other sectors, such as high-yield corporate bonds and leveraged loans.

A Reader was kind enough to send us a primer on central banks swaps. (Who knew the PBOC has a swap line with Argentina?). One of the authors is Benn Steil, author of one of the best ever books on Bretton Woods (The Battle of Bretton Woods, 2013). We read it in a single weekend and that’s saying a lot about a history/economics book.

Not to be crude, but if there really is a looming financial crisis, it likely favors the dollar. This is ironic since it’s the strong dollar that is at least partly to blame for this problem, probably. It’s more expensive for foreigners hedging their dollar assets back to their home currencies now trying to exit those hedges. Maybe it’s no coincidence that the drop in US equities and/or the end of Q3 is when a lot of this turmoil began. If you no longer hold US equities, you don’t need the hedge anymore. Well, it’s a theory.

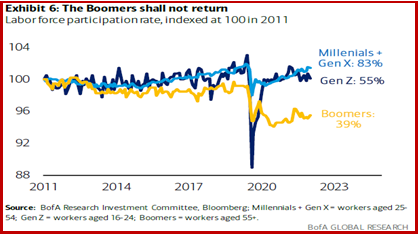

Inflation Tidbits: That labor shortage is weird. A BoA report has some tremendous information about the economy, including this chart that shows the labor shortage really is due to retiring baby boomers plus Gen X (those born roughly between 1965 and 1980, so aged 42 to 57). Two things: this is going to bite us on the rear-end when onshoring manufacturing gets going (think chips). Second, wage hikes are not going to level off because unemployment is going to remain low..

So, if we believe unemployment must rise substantially for the Fed to see the turning pivot point, we are not likely to see it this year, according to BoA. “Payrolls need to slow significantly for unemployment to rise. Monthly job gains would have to drop below 50k for unemployment to hit 5% by the end of next year.” It will take to the end of next year for the unemployment rate to get to 5.5%. The current forecast is for payrolls to fall by an average of 180,000 per month for the first three quarters of next year. We wonder if that is realistic.

One side-issue—there are 7-9 million people not working and not seeking work, mostly on disability, many of whom are likely to be perfectly capable of work. It’s a miserable life because you can’t live on government disability payments, but apparently it beats the proverbial burger flipping jobs.

Inflation Tidbit 2: The NY Fed has issued its latest monthly Survey of Consumer Expectations (https://libertystreeteconomics.newyorkfed.org/2022/10/new-sce-charts-include-a-measure-of-longer-term-inflation-expectations/). Findings: the 5-year inflation expectations remain low at a little over 2% and are comparable across age groups. Another (and new): the likelihood of high inflation rose sharply just after pandemic, but now is falling. And another new one—respondents expect home prices to grow more slowly (except in the South).

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat