The difference in the British and French bond crises

At a glance, the most recent British and French crises were fiscal events, prompted by runaway spending, where those who attempt to prevent calamity are eventually consumed by the crisis itself.

In France, Prime Minister François Bayrou lost a no-confidence vote that saw him ousted following his attempt to force a deficit-reducing budget through the assembly, whilst UK Finance Secretary, Rachel Reeves, clings on by a thread.

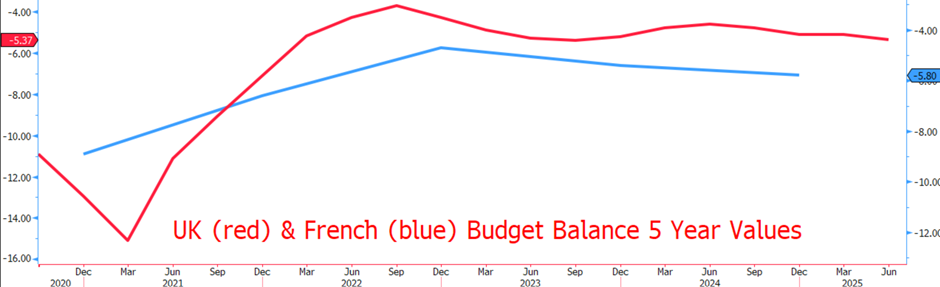

There is an addiction problem in both the UK and France, an addiction to credit, with the respective budget deficits of both shown above, looking similar on the surface. And so when the French PM Bayrou lost his confidence vote over a fiscal issue, we may have expected a similar reaction in French assets to what we saw happen to UK assets.

Yet, we didn’t. In fact, we saw certain signs of French bonds moving in the opposite direction to UK bonds, as if to say that French credit had become more reliable as a result. Indeed, immediately following the vote, we saw the yield on 30-year French bonds actually decline.

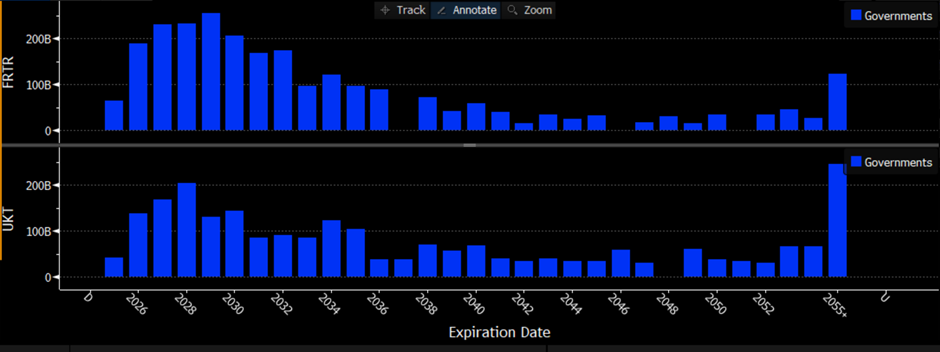

Why? Well, one solid indicator is the difference in the distribution of bond maturities. The French have heavily frontloaded their bond offerings, with most maturing within 10 years or the “short end of the curve”. Practically, this means that instead of asking for your trust that they’ll repay you in 30 years+, you’re just lending to them for a year, or five perhaps, a considerably less daunting proposition than a 30-year line of credit.

In the UK, our Debt Management Office has gone the other way, exhibited above by the value of bonds maturing in different years of France (top chart) and the UK (bottom). Instead, our issuance office has backloaded British debt, so that almost half of it pays off in 30+ years, great when the picture was settled and interest rates low in 2019, not so great in the high-rate, volatile climate we now inhabit.

The debt management office has, in recent years, realised the error of this approach and formally signalled their intent to almost stop long maturity debt issuance, although this seems somewhat like closing the gate after the horse has already bolted.

So, put very simply, the UK and French fiscal crises, whilst having similar causes, had very different effects because the French debt issuance office was smarter than the UK’s. By front-loading the bonds, they ask their creditors to take on less risk. France may run into serious trouble in the future, but for just a year, the risk is worth it. When lending to the UK however, creditors are often asked to extend their horizon into multi-decades, a much more dubious proposition than a shorter-term loan.

Whilst the maturity date of these issuances is not the only factor that meant the Pound dropped so severely during the fiscal angst at the start of this month, I do believe it to be a major factor. France is protected by the fact that it is part of a 20-country monetary system, meaning any issues are only regional when considered within the broad expanse of the Euro as a whole, whilst we in the UK are on our own.

Author

David Stritch

Caxton

Working as an FX Analyst at London-based payments provider Caxton since 2022, David has deftly guided clients through the immediate post-Liz Truss volatility, the 2020 and 2024 US elections and innumerable other crises and events.