The Blame Game [Video]

![The Blame Game [Video]](https://editorial.fxstreet.com/images/Macroeconomics/Events/ElectionUS/Donald-Trump-pointing-out_XtraLarge.jpg)

The Day So Far…

Whether it’s probes into his dealings with Russia, threatening North Korea with fire and fury, or blaming both sides for the deadly violence in Charlottesville, the President of the United States of America is doing a good job at remaining top of Twitter’s trending topics. As such, over the last few months Trump’s disapproval rating has continued to rise but if you were looking purely at the financial markets it would be hard to tell this was the case.

Whether this is complacency or confidence in the underlying economy is hard to tell but it does seem that Trump’s relevance for markets is diminishing. I mention this as there was a school of thought in recent months that with all the distractions the more market sensitive pledges of wide scale fiscal stimulus was at risk of being delayed or even implemented at all. However, what now appears to be the case is that despite the momentary blips of volatility Trump’s unstable manner seems to be priced in to some extent and is now expected by the trading community.

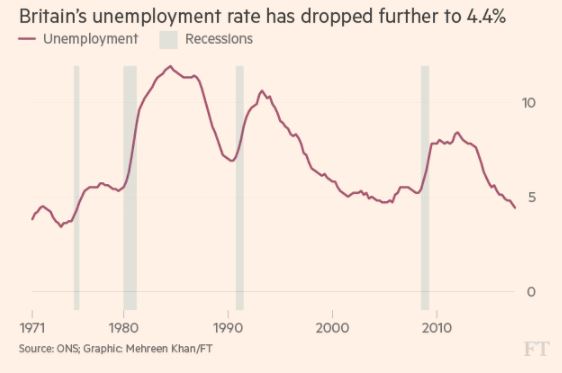

Moving away from Trump and back to financial markets, UK economic data has been back in focus and after yesterday’s slightly weaker CPI reading the latest wage numbers outpaced expectations while unemployment for the second quarter dropped to a 42-year low. As such, GBP/USD has reversed some of the losses seen on Tuesday but has encountered resistance at the daily pivot level in the futures market just above the 1.2900 handle.

Elsewhere, EUR/USD has also had a volatile start to the day firstly seeing some weakness on the back of a Reuters source report suggesting Mario Draghi will not deliver a new policy message at the upcoming Jackson Hole conference, putting aside any market concerns that his first appearance at the event in 3-yrs may have been used to deliver a hawkish surprise. However, the currency soon reversed following the latest flash GDP estimate for the EU which confirmed the Euro-area is well on track.

The Day Ahead…

Our strategies for this afternoon are a repeat of yesterday in that it is only the S&P that we remain more positive on with short plays prepared for EUR/USD, T-notes and WTI crude. From a calendar perspective the housing data is unlikely to draw much attention but the DoE oil inventory numbers could be interesting. Last night we saw the headline API crude number show a drawdown of 9.2mln (Exp. -472k), the largest draw since September 2016. However, negating some of the bullish interpretation was the Cushing build (+1.7mln vs Exp. +700k) and gasoline number which had its second weekly build in a row (+301k vs Exp. -450k). Although on balance the outlying nature of the headline has seen WTI crude futures drift higher this morning the mixed nature of the overall report, with the release of the US output figure, will further complicate the initial reaction later with the best advice to await clarification on the full report rather than jumping in aggressively when the numbers hit at 3.30pm this afternoon.

Finally, the FOMC minutes of the July meeting are due at 7pm with economists at Deutsche Bank expecting the committee to remain on course to announce the commencement of its balance sheet unwind at the September meeting with a lively debate likely to have taken place on the outlook for inflation.

Author

Amplify Trading Team

Amplify

Amplify Trading is a proprietary trading company specialising in the development of new trading talent offering direct experience in financial markets.