Systemic growth slowdown might trigger negative rates in the Eurozone

Outlook:

We get Dec new home sales from the National Association of Realtors, forecast lower again after Nov shocked with the biggest y/y drop in 7 years, 8.9% m/m when a gain of 3.7% was forecast. It was the lowest number since March 2016. We have no reason to think the numbers will be any better today. New home sales is a minor number but contributes to sentiment.

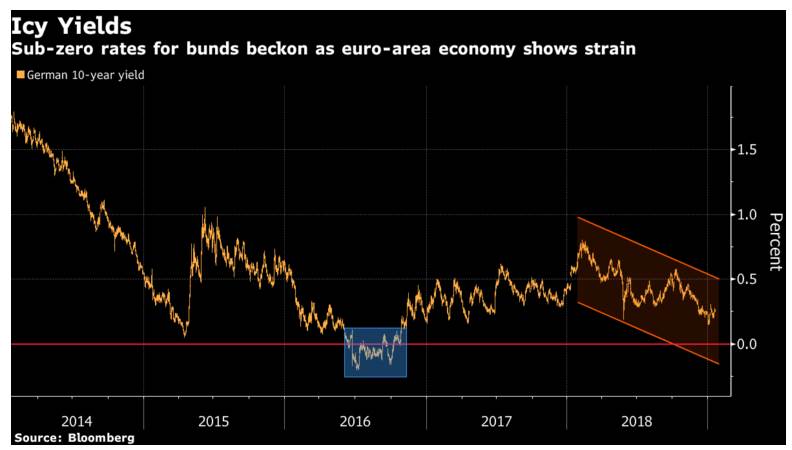

We were set back on our heels by a set of Bloomberg stories that are worth summarizing. It boils down to shock vs. systemic stall. The US may be getting a shock in the form of a worse slowdown from the shutdown than we expect, but it's a huge economy and has a good chance of recovering. It's different in the eurozone, where the trend is a developing downslide that is systemic. Bloomberg reports a handful of important Big Bank analysts who see the Bund yield headed back below zero within the year, maybe even within the quarter—Citibank, NatWest, SocGen. The German yield is starting to look like Japan's. At the last press conference, Draghi admitted data is weaker than expected and momentum may be faltering. "... current money-market pricing implies investors expect any increase only in the second quarter of 2020" rather than near year-end this year. SocGen's Juckes (and we always listen to him) said "If the U.S. economy wasn't slowing, the euro would already be the other side of $1.10." Citi sees the PMIs falling below 50, meaning contraction. With inflation also falling, it's the recipe for negative rates.

Other currency strategists retain optimism about the euro, like Morgan Stanley, Credit Agricole and TD, even if traders are delivering a different verdict in the form of the options risk reversal pricing. One cause of trader skepticism is political risk that will stay the hand of the ECB. Even so, the strategists call for rates going up next year, maybe twice, taking the deposit rate to zero, out of a deep desire to exit QE. TD forecasts the euro to 1.27, vs. the Bloomberg survey average of 1.20 for year-end 2019.

The Allianz strategist names a string of political risks, including Italy, EU parliamentary elections, the new EU commission, and the new ECB chief in the fall. These are fault lines that may prevent the ECB from raising rates. Despite dissipating confidence in the eurozone, the comparison with the US is what counts, and the Fed is definitely on hold. Morgan Stanley forecasts the euro rising to 1.31, vs. 1.20 for the survey average and 1.10 at SocGen.

In Davos, Ray Dalio and former BBK hotshot and now UBS chairman Weber each said the Fed went overboard hiking in 2018, and it's correct for the Fed to be staying its hand now. Dalio suggests rates might get cut this year. A Bloomberg opinion-writer suggest self-interest is motivation, and in comparison with the 1994 tightening, which we referenced a week or two ago, the market reaction has been tepid. "Central bankers may well be encouraged by how well tightening has gone so far, and continue on the path, perhaps thinking that if they don't so it now, it may be a long time before they get the chance again."

This is an important point, or rather it would be an important point if we knew how Mr. Draghi sees it. Remember that at one of the press conferences, Draghi said QE is now an established tool in a central bank toolkit. More recently, Fed chief Powell said contracting the Fed balance sheet is a side issue and not relevant to the Fed's decision making today. The two statements are not comparable, of course. Powell would not deny that QE has become an established tool. But just how much does Mr. Draghi wish to contract the ECB's balance sheet? Or does it view that as secondary, like Powell?

At a guess, fiddling with the balance sheet, while of concern to the Bundesbank, is not a hot-button issue. Mr. Draghi might be free to alter this proportion or that ratio to goose lending. What we need to learn about is the bagful of tricks that do not come to the public's attention, despite best efforts to make central banks "transparent." Tightening does not always come in the form we can see directly, and without an announcement effect. This is a battle between the market and the central bank. The ECB displays intent to tighten and the market doesn't believe the central bank can or will get away with it.

In other words, the market thinks the ECB is wrong. This is exactly what we see with the fixed income gang in the US and the Fed. The gang says the Fed is wrong a lot of the time. The Fed capitulated this time, but on the whole, central banks are reluctant to let the market bully them. We need to see Draghi talk about the intent to tighten this week, if possible. A reporter is sure to ask. We could have an entirely different chart by end of day on Thursday.

Tidbit: The winner of the PC-naming contest is Jack, for Bogle. HAL+ comes in second. Thanks to all for voting!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a free trial, please write to [email protected] and you will be added to the mailing list..

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat