Strong Franc sparks bets on SNB negative rates

-

Franc the main FX winner since “Liberation Day”.

-

Could hit Swiss exports, lead the nation into deflation.

-

How will the SNB respond: Negative rates or intervention?

-

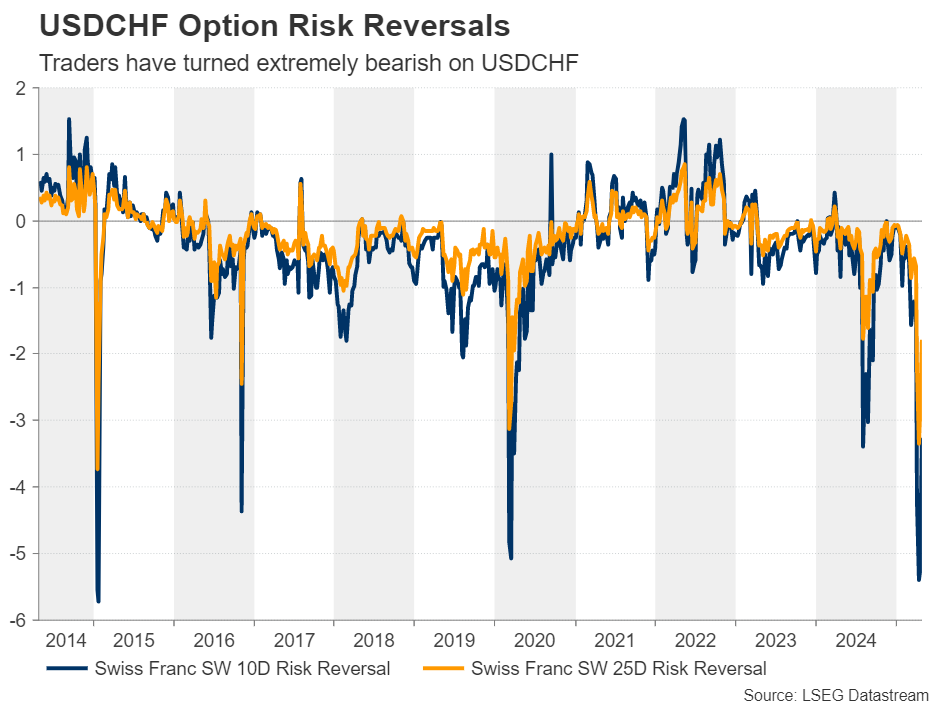

Risk reversals point to strong setback should appetite improve further.

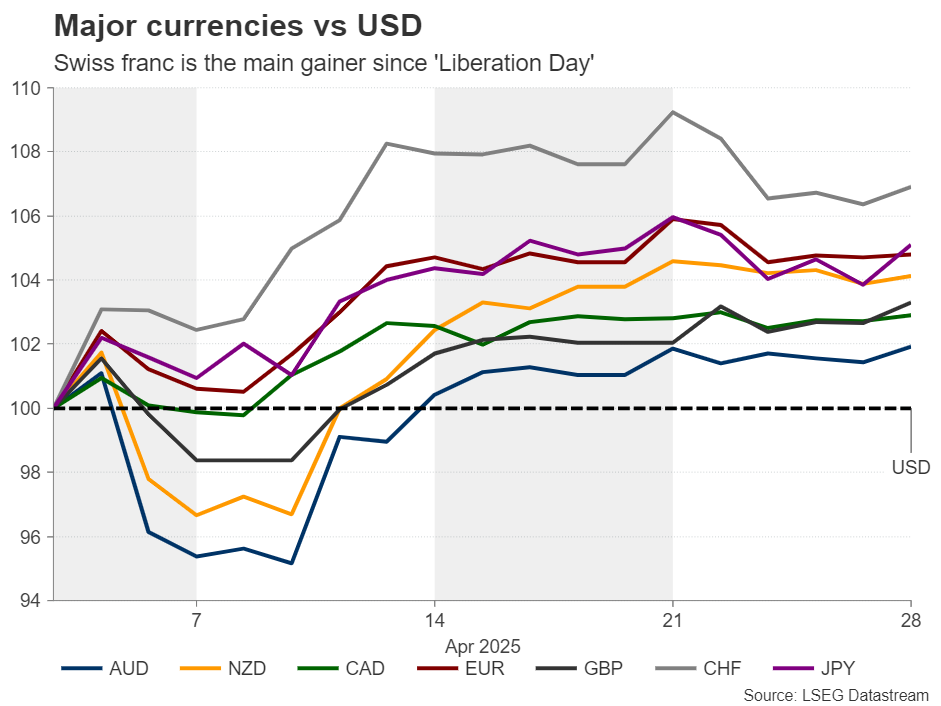

Swiss franc the ultimate FX haven

The Swiss franc seems to be the ultimate safe haven in the FX arena amidst the market turbulence caused by US President Trump’s trade policy and the rhetoric surrounding it. Since the so-called “Liberation Day,” when Trump announced tariffs on all the US’s main trading partner, the franc has been the best performing major currency, with the other safe haven, the Japanese yen, taking second place. In third place, very close to the yen, stands the euro, which benefited from the selling of US assets amid recession fears by the recent fiscal shift in Germany.

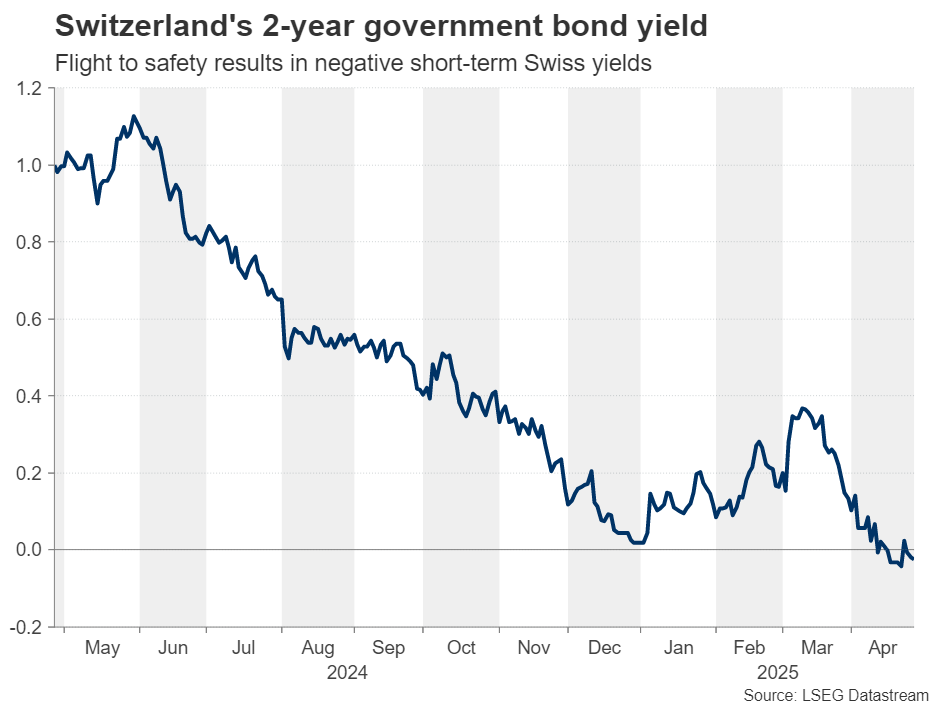

But why did the franc gain the most? Why didn’t the yen follow suit? Switzerland is considered a safe-haven destination for investors due to its strong banking and financial system, its political stability and neutrality, its trade surplus, its favourable tax laws and its strong legal system. Investors were so willing to divert their flows there that they allowed the Swiss 2-year government bond yield to drop into negative territory. This means that investors are willing to lose some money in nominal terms in exchange for the safety of their capital. The yen did not perform in a similar manner, perhaps as traders scaled back their BoJ rate hike bets amid the trade uncertainty.

Surge threatens exporters, increases deflation risk

Having said all that, the appreciation of the franc is a major threat to Swiss exporters as it raises the price of what Switzerland’s trading partners are paying for Swiss goods. Switzerland is a net exporting nation, and the biggest importer of its products is the European Union. Although the euro also appreciated, it did not shine as the franc, leading to a drop in euro/franc and an increase in the price of Swiss products in the rest of Europe.

And the timing couldn’t be worse as US tariffs are also threatening Swiss exporters. On April 2, the US imposed a 31% tariff rate on Swiss goods, before the broader 90-day delay was announced.

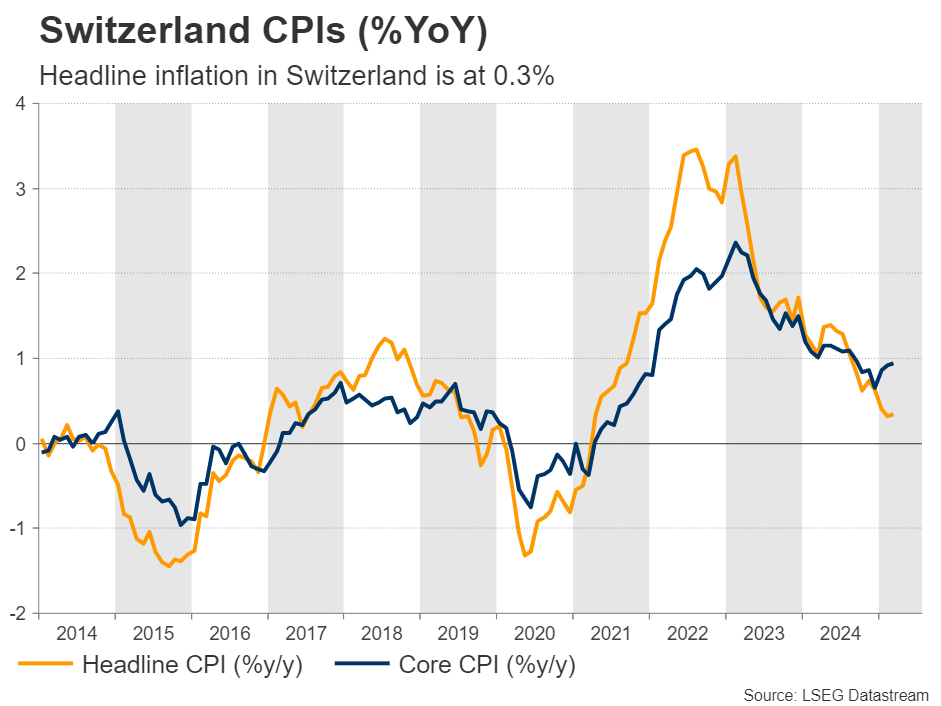

All this could weigh on Swiss inflation and it is very likely to result in deflation. After all, the year-over-year CPI rate in Switzerland is already very low, at 0.3%. And the big question on many market participants’ minds nowadays may be: How will the Swiss National Bank (SNB) respond to that?

Negative interest rates or Intervention

There are two channels through which the SNB had battled the appreciation of the franc. One is through cutting interest rates as most central banks around the globe are doing, and the other is through intervention, by buying its own currency and selling foreign reserves.

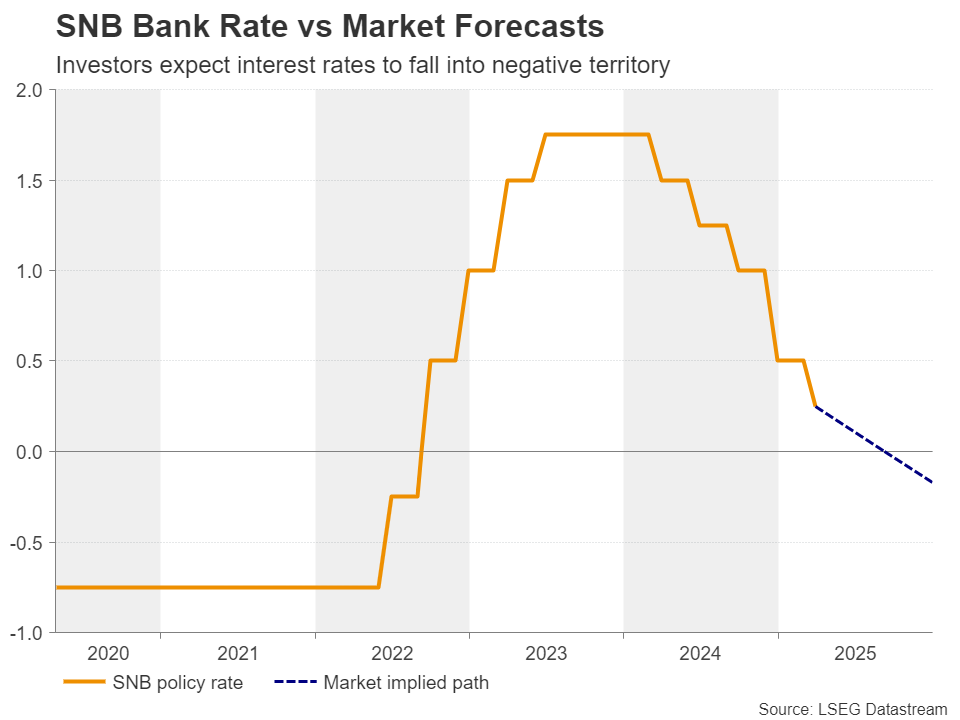

Getting the ball rolling with interest rates, the SNB has the lowest benchmark rate among major central banks, currently at 0.25%, and the franc’s appreciation may have raised speculation that policymakers could push interest rates into negative territory again. Indeed, according to Switzerland’s Overnight Index Swaps (OIS) market, there is an around 80% chance for a quarter-point cut to zero at the Bank’s next decision on June 19, with another 10bps worth of cuts expected by September.

SNB Chairman Martin Sclegel has not ruled out the likelihood of interest rates diving into negative territory but noted several times in the past that such a step would not be taken lightly.

This makes the option of intervention as the more likely one. Or not? According to a Bloomberg analyst-based survey, most participants predict that the Bank will avoid cutting interest rates below zero, with only Goldman Sachs holding such a forecast.

Nonetheless, intervention will not come without consequences. Such a policy risks stirring the US hornets’ nest, with Trump likely branding again Switzerland as currency manipulator as he did back in 2020. Although this could weaken Switzerland’s negotiating hand in potential trade talks, the President of the Swiss Confederation Karin Keller-Sutter said recently that she is not worried about that, which keeps intervention as a more likely option than negative interest rates.

The painless way

The painless way is for the Swiss franc to further weaken on its own. The SNB could still cut interest rates to zero, but officials could refrain from taking them into negative zone and also abstain from intervening. However, for that to happen, risk aversion may need to improve further, driven by new headlines about easing tariff tensions and the potential of trade negotiations.

The Swiss franc could fall notably, leading to impressive rebounds in franc pairs. What supports this notion is the fact that, on April 11, the 10-day and 25-day risk reversals of dollar/franc options hit their lowest since January 2015, when the SNB abandoned the 1.20 floor in euro/franc. This points to extremely bearish conditions, which suggests that there may be very little room for the franc to appreciate further and a lot of downside potential in case the broader market environment brightens further.

Author

Charalampos joined the XM Investment Research department in August 2022 as a senior investment analyst.