Stocks: Potential Risks That May Derail Rally

The global stock market rally that began in early January continued for another day yesterday and continued this morning in Europe, although indices here momentarily gave up their gains while US index futures turned flat. This morning's brief dip came about after Bloomberg reported that a meeting between Presidents Donald Trump and Xi Jinping to sign an agreement to end the US-China trade war won't occur this month and is more likely to happen in April at the earliest. Apparently, this was according to three people familiar with the matter. Truth be told, if this story turns out to be correct, it shouldn't come as major surprise given that Trump himself has already hinted at the prospects of delay when he said the US was not "in a hurry" to a sign a deal. Thus, there is a possibility that any weakness related to US-China trade talks being delayed could prove to be short-lived.

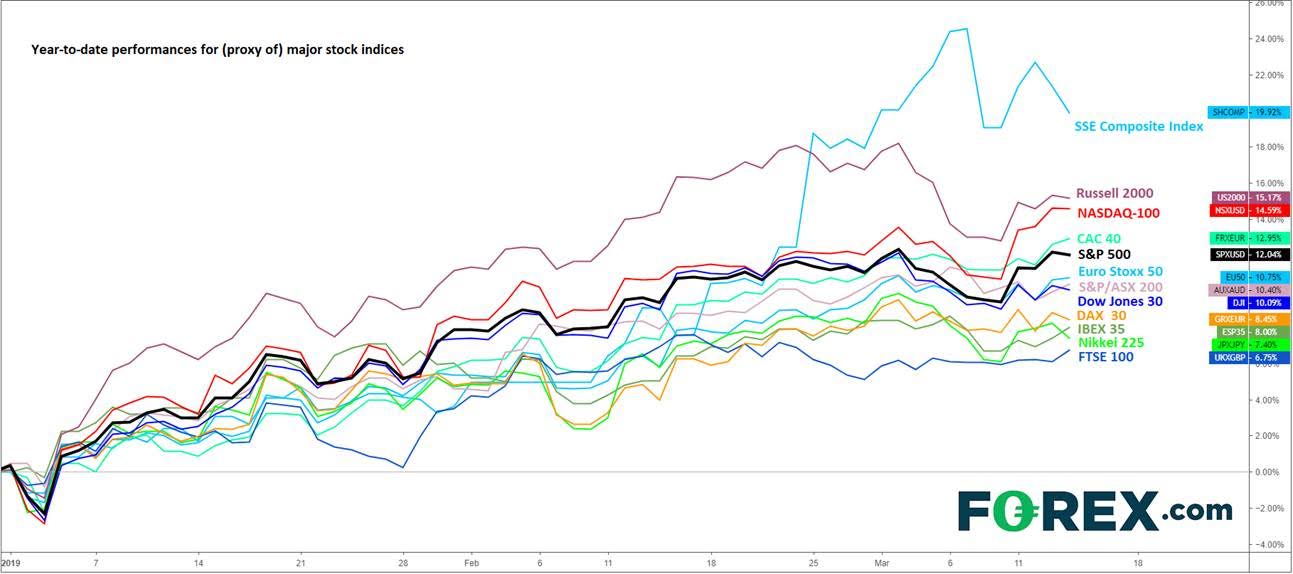

Looking ahead, though, there are a few key risks facing European and global stock markets in general. But sentiment is currently positive given the sharp year-to-date gains for China (nearly 20%), although the rally here has stalled a little over the past few days, while in the US the S&P 500 hit a new high for the year yesterday. Sentiment has so far been boosted by various factors, including:

-

Hopes over (an eventual) trade deal between US and China

-

Falling bond yields amid renewed dovishness from major central banks, boosting the appeal of the riskier equity markets

-

Introduction of various fiscal and monetary stimulus measures from China

-

Global economy not performing as poorly at the start of this year as had been expected

But despite the sharp gains for the US and China, European markets are lagging behind slightly. Here, investors are not as jubilant in part because of ongoing Brexit concerns and weak economic performances across the Eurozone. As well as exports being hit by falling Chinese demand, the recent emerging market currency crisis in places like Turkey has also weighed on growth. But with the ECB introducing new long-term loans for banks and pushing back its rate hike expectations, investors have been warming towards European equities of late. Still, the markets face a few major risks, which among other things, include:

-

Potential for a disorderly Brexit

-

Possibility of US-China trade talks to break down (not to mention the positivity being nearly price in)

-

The imposition of more tariffs on European exports by the US

-

Further economic slowdown in Europe

-

Profit-taking after big gains Q1 US earnings being more disappointing than expected, with mavens at FactSet predicting S&P 500

-

Q1 earnings to be -3.4%, which would be the first year-over-year decline in earnings since Q2 2016. According to FactSet's estimates, the forward 12-month price to earnings ratio for the S&P is 16.0, which is below the 5-year average of 16.4.

So, investors are faced with elevated levels of risks as we head towards the first quarter. While the recent falls in bond yields amid the prospects of interest rates remaining low for longer may keep the downside limited, I am sceptical that the gains we have seen so far this year can be repeated in the upcoming months. Above all, there's the potential for profit-taking with indices looking a little overstretched again.

Figure 1:

Author

Fawad Razaqzada

TradingCandles.com

Experience Fawad is an experienced analyst and economist having been involved in the financial markets since 2010 working for leading global FX, CFD and Spread Betting brokerages, most recently at FOREX.com and City Index.