Stick or twist [Video]

![Stick or twist [Video]](https://editorial.fxstreet.com/images/Macroeconomics/CentralBanks/BOE/bank-of-england-on-threadneedle-street-in-london-15709828_XtraLarge.jpg)

The Day So Far…

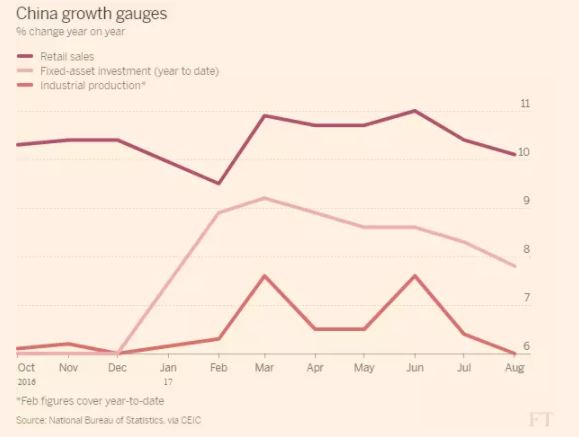

Not a great deal to speak of so far today as market participants await two key risk events that being the Bank of England interest rate announcement and the latest CPI reading from the US. Before we discuss these releases in more detail lets start from last night where US equities finished in minor positive territory with the surprisingly near-term timeline tabled for further details surrounding the Trump tax plan. Overnight the Asia-Pac session was a little more mixed with focus on the AUD which spiked higher upon release of the latest jobs data where employment rose by 54,200 from July, over and above the expectations of just a 20,000 gain. In fact, CBA pointed out overnight that in the last six months over a quarter million jobs have been created a performance that has not been matched since some 17-years ago. However, the move has since been partial retraced following the release of a suite of Chinese economic data where industrial production and retail sales fell short of street estimates.

Elsewhere, oil is in bullish mode with a technical break of yesterday’s high acting as a catalyst for a move toward $50. This comes after a positive session yesterday following the latest report from the IEA who noted global oil demand is outpacing expectations and excess crude inventories are falling. Taking a further step back, this week has also seen a persistent theme of verbal support for prices from influential members Saudi Arabia and Russia who continue to state their willingness to act beyond the current production agreement if required.

The Day Ahead…

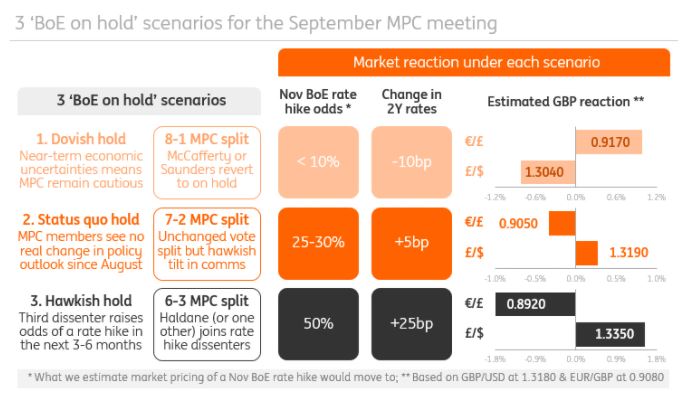

The Bank of England today has the possibility of being one of the more interesting meetings in recent months. Important to note that we are not expecting any change in interest rates today but given the move higher in core inflation this week (now highest since Dec 2011) there is likely to be a material change in the tone of the minutes which on balance may be perceived as being more hawkish. From a strategy point of view it would make sense that the Bank may attempt to remain credible that they can move on rates in the future if inflationary pressures were to persist. The other big factor to the short-term movement of GBP is the vote split where by there is a plausible chance chief economist Andy Haldane may have joined longstanding hawks Ian McCafferty and Michael Saunders. Today’s meeting also sees new member Sir David Ramsden cast his inaugural vote but expectations are that he will stick with the majority at least until he finds his feet. My thoughts here are that even in a 7-2 split the overall outcome could still be perceived to be hawkish once the language of the minutes is scrutinised, but overall this doesn’t change our longer-term view that interest rates in the UK are not going to rise anytime soon with evidence in yesterday’s wage data reflecting the ongoing squeeze that is being faced by the consumer under the cloud of political uncertainty in the year ahead.

Here’s a useful table from analysts at ING on today’s meeting:

In terms of US CPI the market will be digesting the data in direct context to its implication on Fed policy thinking and the fate of a December rate hike. DB noted this morning that we have had 5 consecutive downside misses on the core reading and even if the M/M figure comes inline with expectations it would result in the Y/Y rate slipping one tenth to 1.6%, the lowest since January 2014.

Author

Amplify Trading Team

Amplify

Amplify Trading is a proprietary trading company specialising in the development of new trading talent offering direct experience in financial markets.