Sterling Pounds Brexit Bears

Victory for new President Trump has markets focusing on the prospect of substantial public spending lifting U.S inflation and prompting a rise in domestic interest rates. The odds of two Fed rate hikes by end of next year have risen to almost +90%, and it’s this potential rate differential that has the dollar in demand.

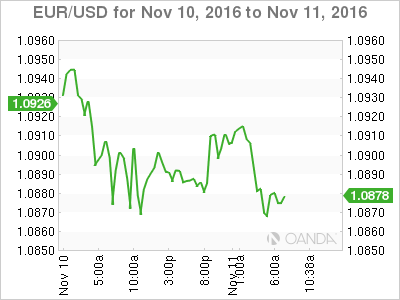

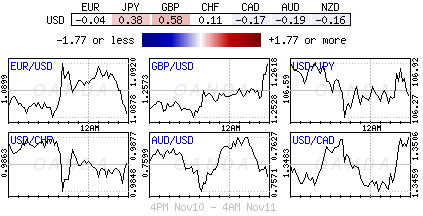

With a Trump win, perhaps the euro (€1.0870) may be the next currency victim? His victory this week certainly raises concerns about a massive shift towards “populist politics” before next year’s elections in France and Germany. The single unit, straddling atop of some key support levels, is at risk of medium-term bearishness given the numerous political risks facing the eurozone over the next few quarters. Trump’s loose and reflationary fiscal ideology should only add weight to the single unit.

The uncertainties surrounding the Republican win this week certainly strengthen the case for the ECB to extend its current asset purchase program by an additional six-months beyond March next year. This would be supportive for Euro credit, and to a certain extent the currency.

1. Emerging equity rout persists

Emerging markets are feeling the heat; they sold off aggressively overnight as U.S. Treasury yields continue to back up.

With investors favouring U.S conditions, money continues to be pulled out of Asia and into the U.S and why regional currencies, bonds and stocks are underperforming.

Indexes from Indonesia, Philippines and Malaysia’s plummeted on average a couple of percent.

In Hong Kong, the Hang Seng Index was down -1.4%, South Korea’s Kospi closed -0.9% lower and Taiwan’s Taiex fell -2.1%.

However, bucking the trend was Japan’s Nikkei rallying +0.2%, even as the yen (¥106.30) gained +0.3% outright. Australia’s S&P/ASX 200 also rose +0.8%, lifted by the global commodity rally. In Shanghai, stocks entered a technical bull market.

In Europe, equity indices are trading mixed across the board as Brexit concerns resurface after market participants accept Trumps electoral victory. The banking sector is trading generally and weighing on Eurostoxx, while commodity and mining stocks in the FTSE 100 trading mixed.

S&P futures are trading little changed ahead of today’s Veteran’s Day holiday stateside.

Indices: Stoxx50 -0.4% at 3,037, FTSE -1.2% at 6,748, DAX +0.1% at 10,645, CAC-40 -0.5% at 4,509, IBEX-35 -0.9% at 8,677, FTSE MIB +0.4% at 16,872, SMI -0.4% at 7,898, S&P 500 Futures -0.3%.

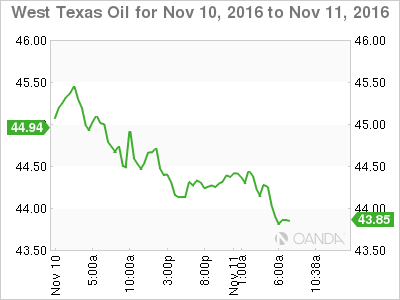

2. Oil prices dip on supply overhang, Commodities rally

Oil prices trade under pressure as dealers refocus on the markets persistent fuel supply overhang that is not expected to subside unless OPEC and other producers cut their output significantly. Will they do that on Nov 30?

Brent crude futures are trading at +$45.70 per barrel, -14c from yesterday’s close. Light crude or West Texas Intermediate (WTI) futures are trading -29c lower at +$44.37 per barrel.

This week the International Energy Agency (IEA) reported record production from OPEC members and subdued expectations for demand growth. The market believes that this supply glut is capable of running deep into next year without an output cut from the OPEC at the end of the month.

U.S. President-elect Donald Trump’s promises about infrastructure spending are supporting industrial metals, which are having their best week in more than 25- years.

Copper, a core industrial metal, has surged +3.6% overnight +7% since the U.S. election, while iron ore has jumped +4.4% to a two-year high.

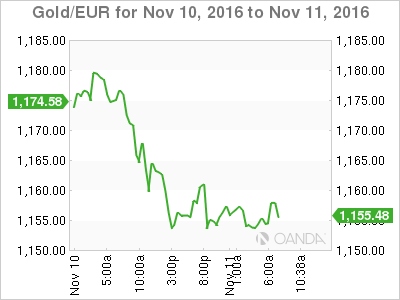

If a different story for gold, its lost -3.9% ($1,257) this week on inflation expectations and the potential for Fed tightening.

3. Bonds Trump tantrum

U.S bonds have extended their selloff in the worst week for Treasuries in nearly a decade. Global bonds have lost -$1 Trillion in value this week.

Overnight, the yields on U.S 10’s have climbed to +2.118% from +2.07% Wednesday (which saw the largest one-day rise in yields in three-years +22bps).

This market selling is not isolated to the states, Aussie 10-year yields have surged +7bps to +2.57%, the highest since May. Similar-maturity notes in Germany fell for a fifth day, and currently yield +0.34%.

Yesterday Federal Reserve Bank of St. Louis President James Bullard (voting member) said that he remains on board with raising rates next month and explained it will take some time to understand the economic implications of the unexpected election of Trump to be president. Fed fund futures are pricing in +80% chance of a Dec Fed hike.

The President-elect’s strong bias toward fiscal expansion, which will lead to inflationary pressures, opens the door for the Fed to hike more quickly in 2017 and 2018 than previously expected.

4. Sterling Pounds Brexit Bears

So far, Cable is amongst today’s best performers, hitting a six-week high of €0.8615 against its Euro counterpart and a one-month high outright £1.2633.

Note: The pound has now recovered all of its losses following last month’s Oct 7th flash crash.

There are a number of possible reasons that is putting the pound ‘bears’ under pressure this week.

One, sterling’s demise has been oversold, two, a delayed BoE rate cut expectation, three, or perhaps the markets lack of current focus on Brexit is forcing both dealers and investors to cover some of the massive short positions that the pound has built up recently, nor is Trump’s victory – the “U.S. and the U.K. will continue to enjoy a ‘very special’ relationship.”

Elsewhere, EM currencies are feeling the pressure of capital outflows to higher yielding U.S assets. The MYR is off -1.2% overnight and this has forced the Indonesian central bank to defend its own currency this morning.

Latin America continues their plummet this morning on fears that Trump’s administration will table protectionist measures to protect U.S. workers and companies from unfair trade deals.

5. HUF and Bonds an outlier

In August and September foreign investors were net buyers of Hungarian local-currency government securities after a long streak of negative months. The net share of foreigners owning local government securities rose to +29%.

Demand for Hungarian assets has been on the rise this week, which is trading counterproductive to what else is going on. Why? From a regional perspective, analysts consider it good value, especially since S&P upgraded Hungary to investment grade in September and Moody’s this month. The possibility of looser monetary policy from the ECB is also supporting this.

This Capital “inflow” is also been helping to support HUF (€309.00) to a certain extent – it has been an outperformer this week even while its neighbouring currencies have been hit hard by Trump’s victory.

However, fixed income futures expect a dovish central bank’s (HNB) stance will drive the EUR/HUF towards €315.00 by Q1, 2017.

Author

Dean Popplewell

MarketPulse