Sterling mostly steady after data as Mandelson vetting scandal continues

After a mostly positive job report and inflation in line with expectations, the BoE is nearly certain to hold next week.

The pound was little changed overall after February-March’s British job report came in overall slightly better than expected and annual headline inflation met expectations. While the Gulf conflict and its impact on trade and inflation continue, headlines in Britain have mostly concentrated on the political scandal around the vetting of Peter Mandelson, the former ambassador to the USA. This article summarises recent data and news then looks briefly at the charts of GBPUSD and EURGBP.

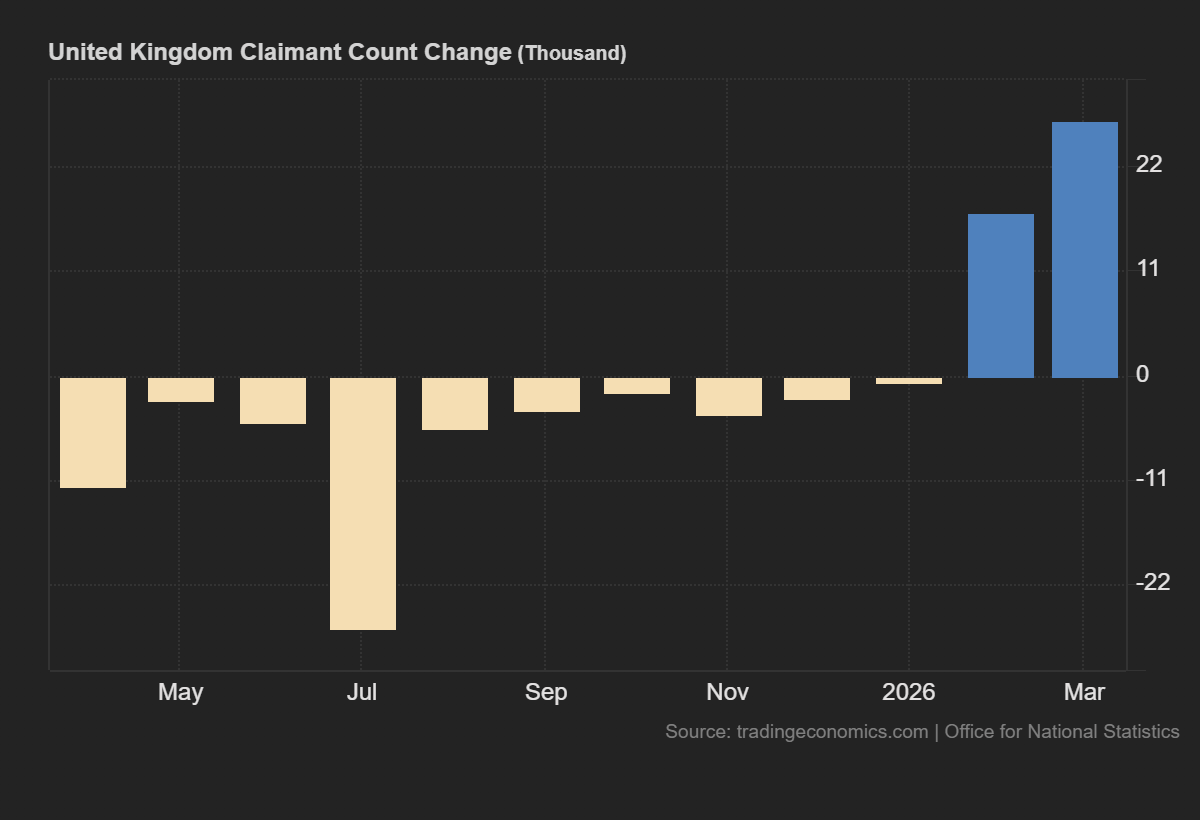

21 April’s British job report covering February-March was somewhat positive on the whole as unemployment declined unexpectedly in February. However, claimants rose more than expected:

The last two months of data challenged the trend active throughout 2025 of consistently declining numbers of claimants. However, February’s unemployment went down to 4.9% against the consensus for a hold at the previous 5.2%.

Some rise in unemployment given the likely economic circumstances in the next few months at least and weaker business confidence seemed to be likely. Inflation though overall rose slightly less than had been expected:

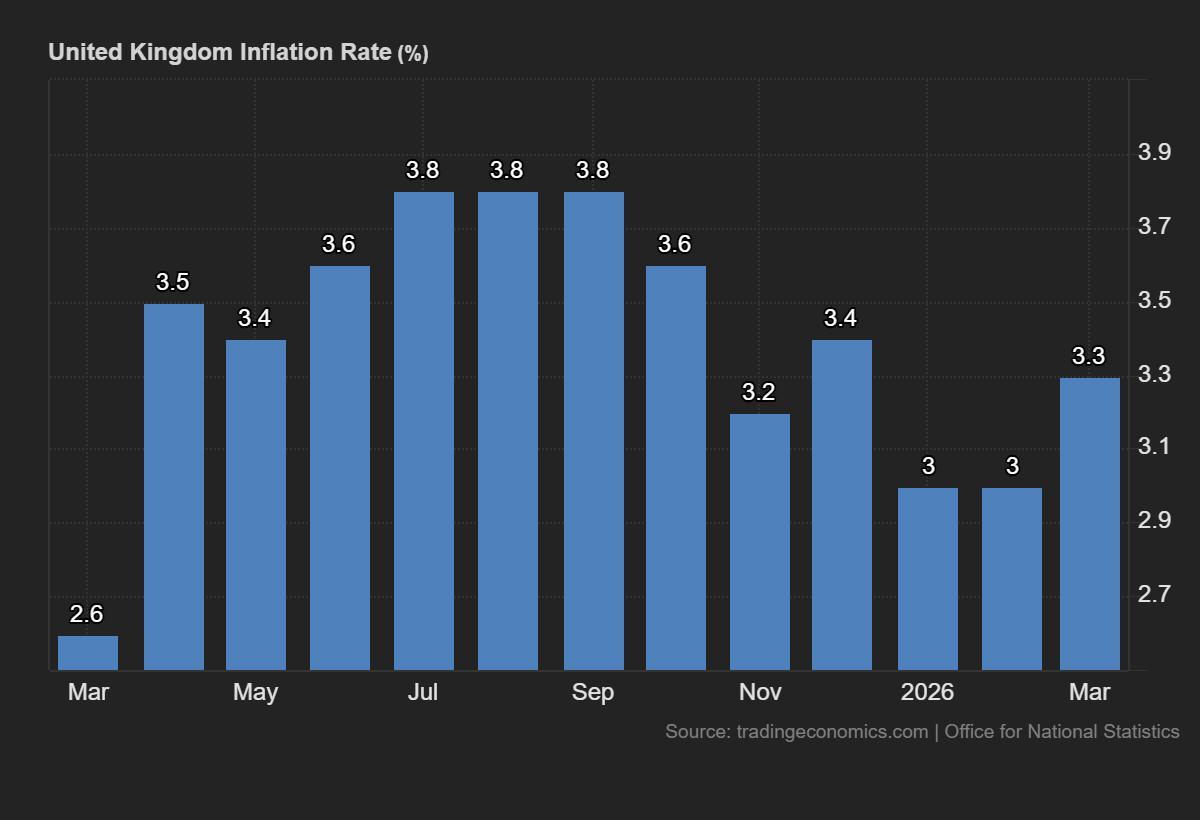

March’s annual headline inflation in Britain above met the consensus at 3.3% but the core figure at 3.2% was slightly less than expected. Similarly to the USA which released inflation for March earlier this month, there’s a clear impact from pricier fuel but not as much as had been feared among some participants.

Overall the impression from these releases plus 23 April’s positive S&P PMIs (manufacturing and services) suggests that the Bank of England (BoE) isn’t under clear pressure to act quickly on rates. Inflation is likely to continue rising at least to some degree in the next few months, but the BoE’s governor Andrew Bailey has effectively ruled out immediate strong hikes.

Prime Minister Keir Starmer is under threat again due to the ongoing inquiry into his handling of the vetting of Peter Mandelson before the latter’s appointment as ambassador to the USA. Although this has been very widely reported on and analysed in most British media, it’s questionable whether this scandal itself seriously threatens the Prime Minister’s position. Equally, in the seemingly unlikely event of the PM being replaced, the transition could probably be orderly with his potential successor (Angela Raynor, Wes Streeting or, less likely, another current minister) expected to favour continuity.

Meanwhile the Chancellor Rachel Reeves had good news as official figures on 23 April showed that governmental borrowing was £700m below target in the year to March. The Gulf conflict is likely to mean sustained challenges for the Exchequer but it’s not yet clear how great and how long they might persist. For the British economy and most others overall, traders are watching closely for any news of further negotiations between the USA and Iran as the ceasefire holds for now.

Cable seems vulnerable but $1.35 an important area

Cable appeared to stabilise around 23 April as traders digested overall decent British data in the few days before and the lack of progress in peace talks between the USA and Iran. The Mandelson scandal although the subject of frenzied reporting doesn’t seem to have had a clear effect on markets so far with the probability of it leading to the Prime Minister’s resignation remaining low.

$1.36 around the upper Band seems like a clear potential resistance which might resist another test if buying volume returns. However, with the drop in volume recently, ATR declining overall and the slow stochastic close to overbought, losses seem more favourable in the immediate future based on TA.

The initial target for sellers might be the 200 SMA around $1.34. $1.315 is a low of around six months so it’d be unlikely to see a sustained push below there unless the central banks’ meetings on 29 and 30 April yield major surprises.

Euro-Pound’s losses pause around 86.5p

The euro declined against various currencies including the pound sterling around 21-23 April as the eurozone posted mostly contracting PMIs except for manufacturing and weaker sentiment in Germany. The pound had some support from reasonably good data over the same period, with the job report for February-March generally positive, inflation in line with expectations and PMIs better than expected. The BoE seems unlikely to shift policy anytime soon, certainly not on 30 April, while a single hike by the ECB is priced in for 11 June. The difference in rates is likely to remain more than 1% for some months at least.

The attempt to push below 86.5p on 23 April seems to have been rejected for now, with the price gaining intraday on 23 April after that area was tested. The obvious target for sellers would be the 38.2% weekly Fibonacci retracement around 86.1p. This was tested unsuccessfully twice in 2026 so far, in late January and around the middle of March. However, the slow stochastic signals oversold, so a possible continuation lower might not be immediate.

As the trend has been overall sideways since last summer, the moving averages have bunched closely together and might each function as a dynamic resistance if there’s a bounce in conjunction with the possible static 23.6% Fibo. As for cable, there has been a drop in volume since the start of April. Traders will now watch closely the meetings of both the BoE and ECB on 30 April.

Author

Michael Stark

Exness

Michael has been investing since 2007 and trading CFDs since 2013. He favors considering both fundamental and technical analysis where possible, with a focus on swing and position trading.