Indonesia surprise rate hike may not be enough to save the Rupiah

The surprise rate hike from Bank Indonesia, aimed at protecting the Indonesian Rupiah from sliding further, seems to have worked for now. The rate increase definitely helps, but there’s more work to do if Jakarta wants to ease investors’ concerns for good.

The Indonesian Rupiah touched a record low against the US Dollar on June 8, above 18,200. This sharp depreciation, a nearly 8% drop year-to-date, triggered a rare, aggressive off-cycle response from Bank Indonesia (BI), which raised its benchmark interest rate by 25 basis points to 5.5% on Tuesday.

While the rate hike provided a temporary psychological reprieve for the Rupiah and sparked a massive 7.5% relief rally in the IDX Composite, the IDR remains highly vulnerable.

The currency is caught in a big storm comprising external and internal factors: first, the war in Iran has led to a sharp increase in Oil prices, weighing on energy importers such as Indonesia. Second, a significant appreciation of the US Dollar. And third, increasing doubts about the profound structural shifts being implemented under President Prabowo Subianto's administration.

The Iran shock: There’s little to do about it

The ongoing conflict involving Iran has triggered a sharp depreciation of nearly 7% in the Indonesian Rupiah. Because Indonesia relies heavily on Middle Eastern crude oil shipped through the now-blockaded Strait of Hormuz, the country's Oil and Gas import bills have skyrocketed, placing immense downward pressure on the domestic currency.

Compounding these domestic pressures is the US Federal Reserve's "higher for longer" interest rate stance. Stronger-than-expected May jobs data in the United States have revived expectations of another Fed rate hike in 2026. This hawkish outlook has fueled persistent global US Dollar strength, further capital flight from emerging markets, and prolonged pressure on the Rupiah.

This problem isn’t specific to Indonesia: other Asian economies, namely India, have also suffered from the same malaise. But the Southeast Asian country is among the hardest hit.

Indonesians are already feeling the woes: the country’s Consumer Confidence Index dropped to 120.9 in May 2026, down from 123.0 in April and marking its lowest level since September 2025. This slump mirrors a brutal April for the retail sector, where annual sales contracted by 3.7%, a sharp reversal from March’s 3.4% growth, while monthly retail sales fared even worse, plummeting 11.6% to completely erase March's gains.

Fiscal fears, or the "Prabowo risk"

Adding to external woes, global investors are increasingly anxious that President Prabowo Subianto is undoing decades of strict Indonesian spending discipline.

Costly, multi-billion-dollar campaign promises, chiefly the rollout of free school meals for millions of children, have stoked fears of structural fiscal deficits.

Additionally, a necessary but politically painful 32% spike in non-subsidized domestic fuel prices (effective June 10) reflects the soaring toll of global oil costs on the state budget, intensifying domestic inflationary pressures.

Influence over the central bank is another focus of concern: despite Governor Perry Warjiyo's insistence that monetary policies are strictly pro-stability and independent, the central bank's aggressive maneuvers to accommodate structural fiscal shifts have ignited market skepticism regarding BI’s operational independence from the government.

Adding fuel to the fire: The Danantara factor

Effective June 1, the government established a centralized export framework under the sovereign wealth fund Danantara and its operating arm, PT Danantara Sumberdaya Indonesia.

The new legal framework means that, by January 1, 2027, DSI will become the sole export channel and exporter of record for Indonesia’s three flagship strategic commodities: coal, palm oil, and ferroalloys.

While aimed at halting revenue leakages and under-invoicing to stabilize long-term dollar inflows, the policy has triggered immediate regulatory alarm. Exporters and international trade financiers are questioning the erosion of private trade mechanics, contract sanctity, and potential impacts on cash-flow timelines.

However, the change wasn’t taken well outside the country’s borders. Rating agency S&P Global Ratings warned that the plan could hit Indonesia's exports, squeezing government revenues and the country's balance of payments.

How much can Bank Indonesia do?

To halt aggressive capital flight and defend the fragile Rupiah, Bank Indonesia has deployed a massive array of monetary interventions, though it has come at a steep cost to its structural reserves.

The central bank’s off-cycle move is explicitly engineered to widen the real yield differential against the United States, making Indonesian assets structurally more attractive to foreign portfolio managers and discouraging domestic capital flight.

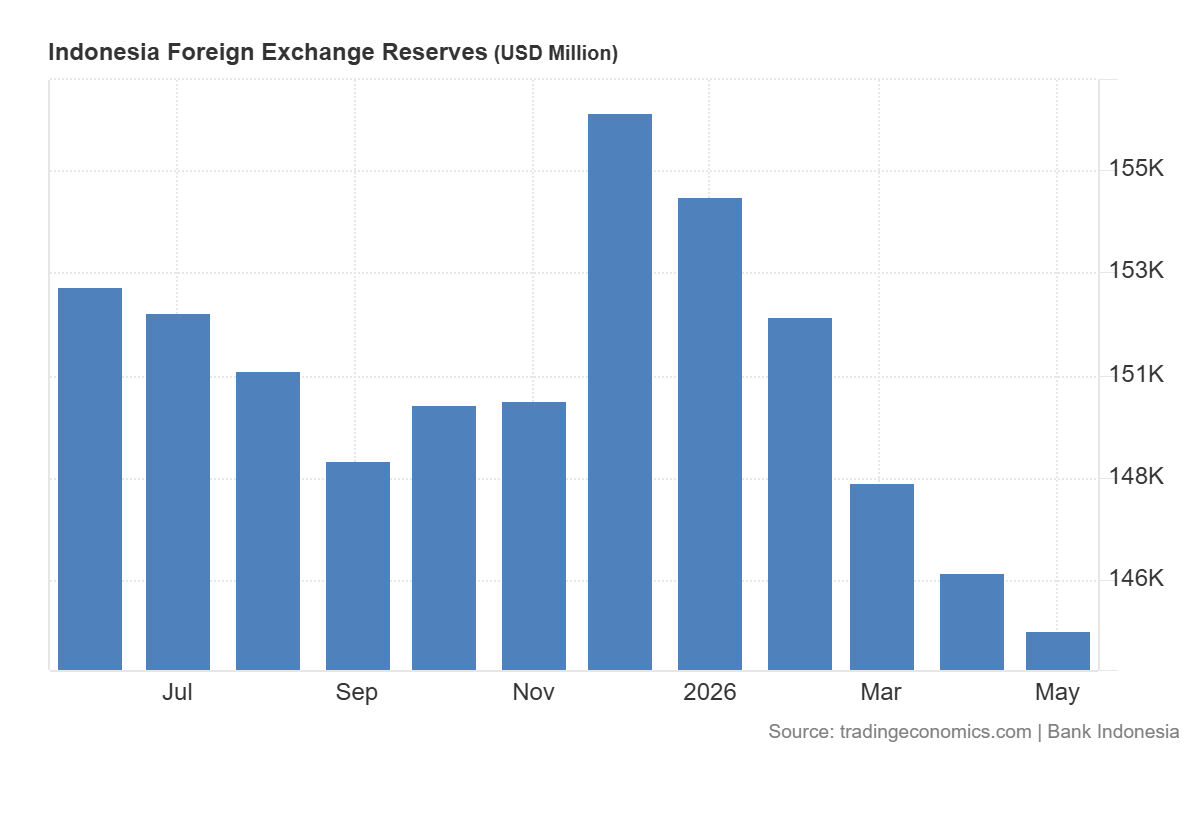

Alongside interest rate hikes, the central bank has intervened heavily in the foreign exchange market, drawing deeply from its war chest. Indonesia's foreign exchange reserves plummeted to a two-year low of USD 144.9 billion by the end of May, reflecting a year-to-date drawdown of roughly $12 billion.

This decline was primarily driven by aggressive spot and forward market interventions to absorb excess Rupiah liquidity, combined with scheduled government external debt repayments. Despite this heavy burn rate, the country's import adequacy remains fundamentally sound at 5.6 months, hovering well above the internationally recognized three-month safety threshold and signaling that the bank still possesses adequate ammunition for prolonged defense.

To further incentivize foreign capital inflows and stabilize the currency, Bank Indonesia has also rolled out structured monetary incentives. The central bank has aggressively pushed up 12-month Bank Indonesia Rupiah Securities (SRBI) yields to 7.25%, pairing these lucrative rates with an attractive 10% hedging swap discount.

By sweetening the deal for yield-seeking international investors and mitigating their exchange rate risk, the central bank hopes to build a temporary buffer for the IDR.

However, this entire defensive framework faces intense scrutiny, as persistent market skepticism lingers over Bank Indonesia’s ultimate operational autonomy amidst mounting executive spending pressures.

What’s next? Bank Indonesia could hike again

Bank Indonesia is trapped in a defensive posture. It will likely have to push interest rates toward 5.75% or 6.00% to keep real yield spreads wide enough to halt portfolio outflows.

The monetary board meets for its scheduled review next week. Given the fragility of the currency and the massive fundamental pressures from the Middle East conflict, Barclays’ projections of another 25 to 50 basis-point hike next week look highly plausible.

Conclusion

BI Governor Warjiyo told parliament that the central bank targets an IDR trading band of 16,800 to 17,500 against the US Dollar for 2027.

Achieving this target depends almost entirely on external factors: a cooling of Middle East tensions to lower Oil import costs and to allow the US Federal Reserve to forget about rate hikes.

But something needs to be done internally as well to ease foreign investors’ worries: If domestic fiscal deficits swell and commodity centralization stumbles into supply chain bottlenecks, the Rupiah faces a high risk of becoming structurally embedded above the 18,000 mark.

Author

Akhtar Faruqui

FXStreet

Akhtar Faruqui is a Forex Analyst based in New Delhi, India. With a keen eye for market trends and a passion for dissecting complex financial dynamics, he is dedicated to delivering accurate and insightful Forex news and analysis.