Brent outlook: Bears hold grip despite fresh escalation in the Middle East

Brent Oil

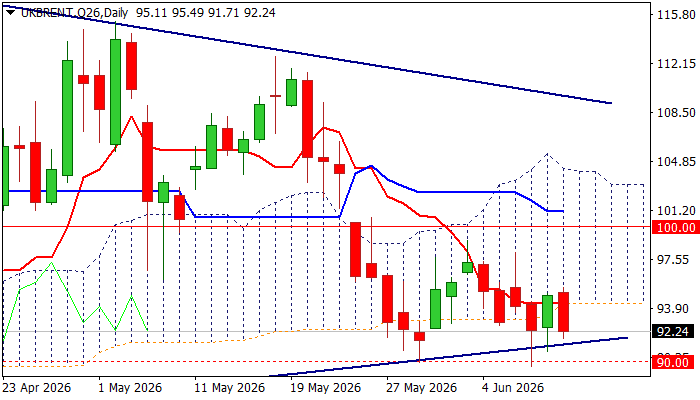

Brent Oil price remains within a range between $90.00 and $95.00 for the fifth consecutive day despite renewed tensions in the Middle East and much stronger than expected draw in US crude inventories, as markets still do not see significant threat from the overall situation.

Although the price repeatedly jumped (Wed / Thu) on fire exchange between US and Iran, gains were limited, with today’s quick reversal (price dropped almost $4) suggesting that markets look for stronger signal from geopolitical side to define fresh direction.

Also, US crude inventories fell by 7.2 million barrels last week (almost identical drop to the previous week’s 7.9 million barrels) and strongly overshot forecasts for 3 million barrels draw, as the US continues to use reserves and strategic reserves to cover up shortage in supply, caused by partial / total close of strait of Hormuz, key route for transport of oil from several Gulf countries that resulted in the lowest oil output from OPEC members in over two decades.

Technical picture remains predominantly bearish on daily chart (negative momentum studies / MAs in mixed setup) with near-term price action mainly holding below the base of thick daily Ichimoku cloud, which now acts as solid resistance (cracked several times but without sustained break higher) that keeps upper breakpoints at $99.00 and $100.00 out of reach.

Near-term bias is expected to remain with bears while cloud base limits recovery attempts.

On the other hand, the base has been formed at $90.00 zone following repeated strong rejection here and renewed attacks are likely to face increased headwinds, but firm break would signal continuation of larger downtrend from $120 zone.

Res: 94.32; 95.50; 97.41; 98.41.

Sup: 91.71; 90.76; 90.00; 89.58.

Author

Slobodan Drvenica

Windsor Brokers

Industry veteran with over 22 years’ experience, Slobodan Drvenica joined Windsor Brokers in 1995 when he was an active trader for more than 10 years, managing the trading desk and own account departments.