Energy markets remain complacent despite significant supply shock

With little tangible evidence of an imminent deal between the US and Iran to get energy supplies flowing through the Strait of Hormuz once again, we believe oil and gas markets are being too complacent, and see significant upside in the absence of a quick resolution.

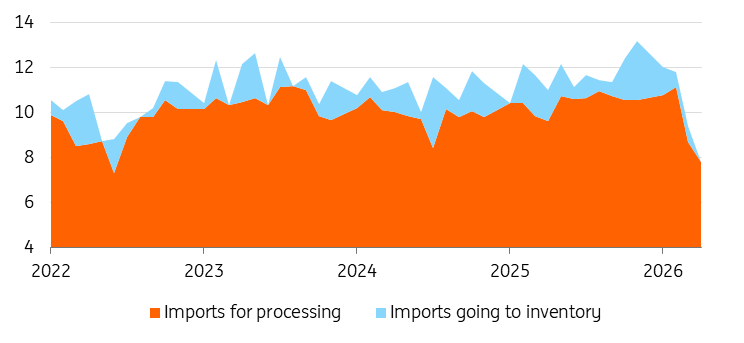

Falling Chinese Oil imports offer relief to the Oil market for now

One wouldn’t think that the oil market is facing an unprecedented supply shock at the moment when looking at price action, with ICE Brent trading below $100/bbl. There has been little to no improvement in energy flows through the Strait of Hormuz and for now there is little sign that we are going to see an imminent resumption in energy flows, with a deal still some way off. This means that the oil market will only continue to tighten and will eventually reach a point where the drawdown of buffers leaves the market increasingly vulnerable to significant upside.

From an inventory perspective, we believe that the end of July could be an inflection point for the market if there is no improvement in energy flows from the Persian Gulf. This could see ICE Brent spike to $120-130/bbl, prompting increased pressure to come to a deal, which at least starts to see energy flows normalising. And failing a deal, one can’t rule out the possibility that we get to a point where energy-starved buyers are more willing to pay Iran tolls for safe passage through the Strait of Hormuz.

Our base case now assumes that we have to wait for this upward pressure before seeing some sort of deal and/or resumption of flows. Therefore, we are of the view that Strait of Hormuz flows will remain largely inhibited until the end of July. This leaves the market in deficit over the third quarter, which sees Brent averaging $110/bbl over 3Q26, before trending lower in 4Q26 and 2027 and flows recover.

There are several factors which have helped to take some pressure off oil markets since the start of the war. First, China has stepped back from the oil market significantly. Crude oil imports in May 2026 fell 3.2m b/d year-on-year to 7.8m b/d – the weakest since October 2017. While China sits on significant inventories, it’s unclear how willing they would be to continue tapping reserves (or potentially even rely on more aggressively), particularly with uncertainty over the duration of the supply disruption. This is a clear risk to our view.

Second, the US has stepped up when it comes to exports. Since the start of the war, US oil and refined product exports are up 1.8m b/d YoY. However, this is not sustainable, given that these stronger exports are coming from inventory rather than additional supply growth. The clear upside risk for the market is if tightening in the US market prompts any intervention from the government when it comes to exports.

Releases from strategic reserves have also shielded the market from significantly higher prices. However, these are coming to an end: the US SPR release is set to conclude by the end of July, after which the pace of tightening in the oil market is likely to pick up. And this is at a time when demand is seasonally stronger.

Chinese Crude Oil imports fall further in May (m b/d)

European Gas storage continues to lag

The European gas market also appears to continue underpricing the supply impact from the Persian Gulf. Global LNG exports in May 2026 fell more than 7% YoY and down 23% from the record levels shipped in January 2026. This has left export volumes at their lowest level since June 2023. The ramping up of new US LNG export capacity has helped to offset some of the Persian Gulf supply losses, but clearly not enough to fully offset. And with new capacity start-ups in 2026 falling short of Persian Gulf disruptions, the market has and will continue to need to see some demand destruction.

Signs of more Asian buying recently could be the catalyst, which has started to raise concerns in Europe. The JKM-TTF spread has been widening as Asian buyers turn to the spot LNG market. This has particularly been evident with Chinese buying appetite returning, while Indian imports have also grown. The longer supply disruptions persist, the more likely we are to see increased competition between Asia and Europe for supplies. EU gas storage is around 43% full, well below the five-year average of 57% full.

The issue for the European market is that the forward curve provides little incentive to inject natural gas for the winter. Summer prices are trading at a premium to winter prices. Therefore, we could see more urgency to fill storage through the third quarter, pushing prices higher. Obviously, the key concern for the market is if Persian Gulf supply disruptions persist through the third quarter, as this will bring more aggressive Asian buying into the spot LNG market at a time when Europe continues to try to fill its storage ahead of the 2026/27 winter.

Given our base case now assumes that energy flows will remain largely constrained until the end of July, we believe that TTF prices will still move higher from current levels. Lower storage levels heading into the 26/27 winter also suggest prices will remain elevated, although much will depend on winter weather.

Author

Warren Patterson

ING Economic and Financial Analysis

Warren Patterson is a commodities strategist at ING. He joined the bank in April 2016 and covers the entire commodities complex. Previously, he worked at a commodities trade house in London.