4.2% headline, 0.2% core: Why the Fed's next hike may be targeting the wrong problem

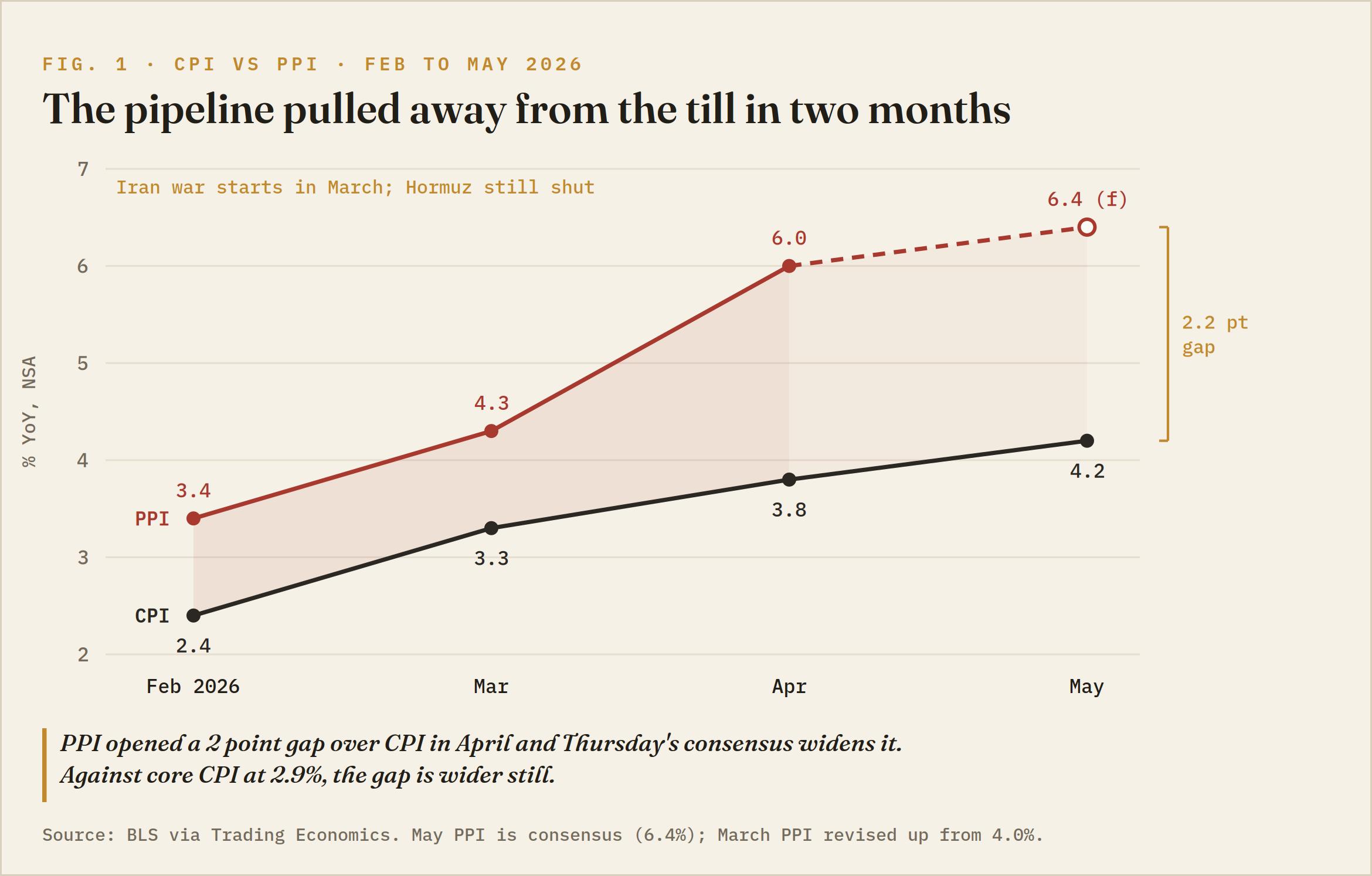

May's Consumer Price Index (CPI) put headline inflation at 4.2% on the year, up from 3.8% in April and the hottest reading since April 2023, while core prices rose just 0.2% on the month, undershooting the 0.3% consensus and halving April's pace. That split is the whole story: the part of inflation that is accelerating is a war tax the Federal Reserve (Fed) cannot print away, and the part the Fed can actually influence just slowed below forecasts.

The Bureau of Labor Statistics (BLS) pinned more than 60% of May's 0.5% monthly increase on energy alone. Yet the futures strip still carries a December rate hike as its base case, which leaves an uncomfortable question hanging over the next week of central bank theatre: what exactly would that hike be aimed at?

The war tax does the heavy lifting

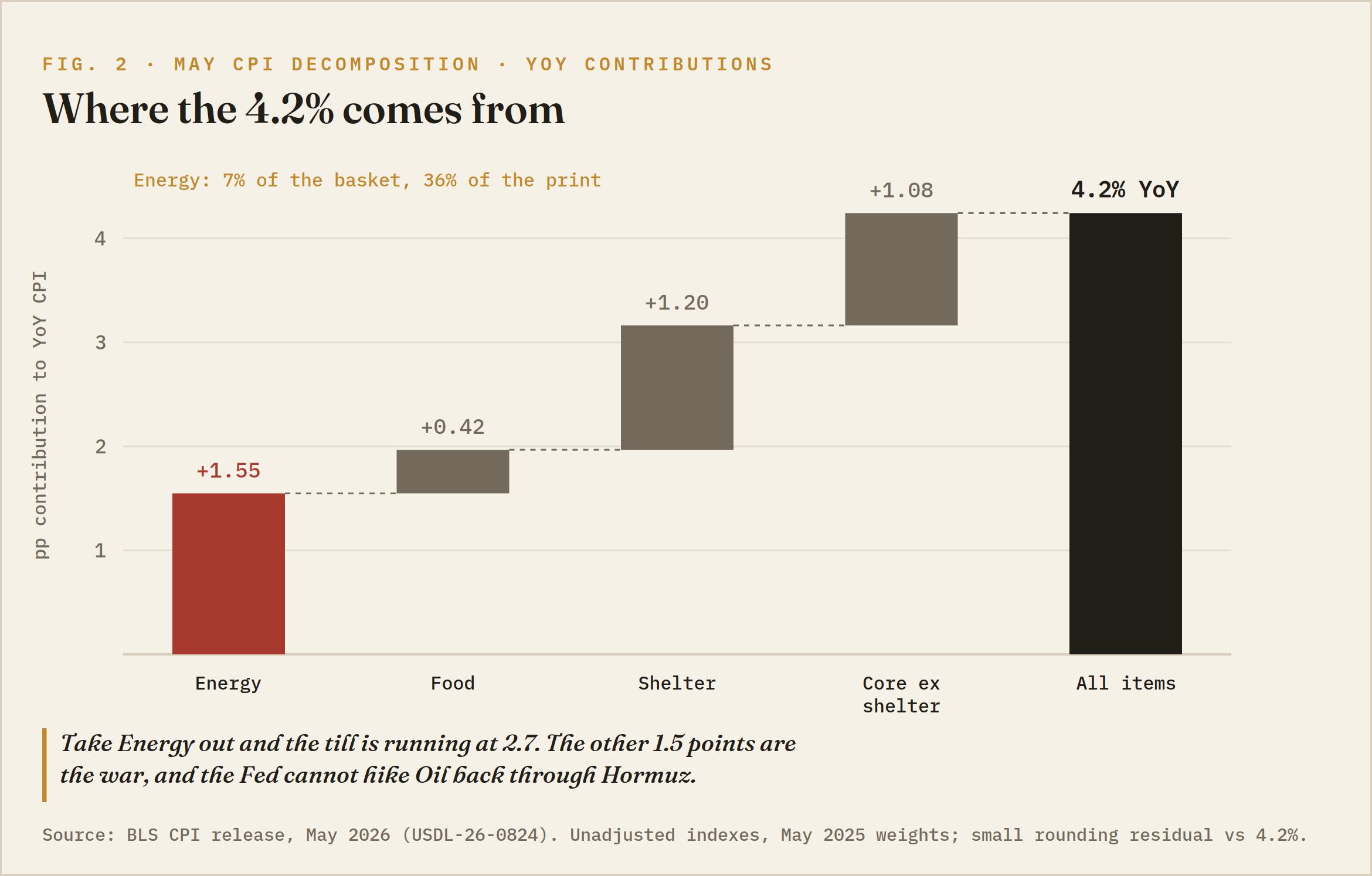

Energy rose 3.9% in May after 3.8% in April and a 10.9% explosion in March, the month the joint US and Israeli strikes on Iran sent Oil to its highest levels since 2022. Gasoline added 7% on the month and now sits 40.5% above a year ago; fuel oil is up 58.9% YoY, and energy commodities as a group are running 40.6% hotter than last May. With the Strait of Hormuz still shut, West Texas Intermediate (WTI) holding above $90 and Brent pressing $97, June's energy line is already half-written.

Tuesday's agreed halt in hostilities survived barely a day: Washington opened Wednesday warning Tehran it would pay for walking away from a deal, and shortly before 16:00 GMT President Donald Trump promised to hit Iran hard again before the day was out, with the deal's fate reduced to a shrug. The tape repriced the escalation in real time. Electricity, the slower-burning channel, is up 5.9% on the year and will keep grinding higher as fuel costs feed through utility tariffs.

The core is whispering demand destruction

Strip out the pump and the picture inverts. Shelter rose 0.3%, half of April's pace. Transportation services fell 0.6% in a month when gasoline rose 7%, which is not what passthrough looks like; it is what households cutting back looks like. Motor vehicle insurance dropped 1.7%, household furnishings fell 0.6%, new vehicles slipped 0.3%, and core goods as a whole deflated on the month, running just 1.1% on the year. The lone clean second-round channel is airline fares, up 2.7% for a third consecutive month and 26.7% YoY as jet fuel works through ticket prices.

Food added a quiet 0.2%, though coffee at 17.5% YoY and beef at 12.9% are doing real damage to the grocery receipt. The hawks argue energy spirals take two quarters to reach services. Maybe. But three months into the shock, the spiral has exactly one confirmed channel, and the rest of the core basket points at a consumer being squeezed rather than a wage-price loop being born.

Warsh inherits the Trichet test

The funds rate has sat at 3.50% to 3.75% since December, and Kevin Warsh chairs his first Federal Open Market Committee (FOMC) meeting next Tuesday and Wednesday, with the decision and his debut press conference on June 17. The committee he inherited was leaning hawkish before he walked in: April's minutes revealed a rare 8-4 split over the statement's easing bias, with most participants prepared to call hikes appropriate if inflation held above 2%. The bond market has pre-voted. The 2-year yield sits above 4%, comfortably through the top of the target range, and a quarter-point December hike remains close to fully priced even after today's soft core shaved the odds at the margin. Last Friday's payrolls beat handed the hawks extra cover.

The awkward parallel is hiding in plain sight. The European Central Bank (ECB) is expected to raise rates on Thursday, into the same Oil shock, with the same softening demand underneath. The last major central bank to hike into a supply-driven Oil spike was the ECB of July 2008, and that decision did not age well. Warsh also has a White House openly campaigning for cuts, which turns his first meeting into an independence test; a chair installed by this administration arguably cannot afford to sound soft, whatever the core print says. The hawks' best card arrives Friday at 14:00 GMT, when the University of Michigan (UoM) survey updates household inflation expectations. The one-year measure went in at 4.8%, and expectations, not the spot print, are what a credibility-minded chair anchors policy to.

And here the politics eat their own tail. The administration demanding lower rates is the same administration promising fresh strikes on Iran, the single largest input into the inflation that makes those cuts impossible. Wednesday compressed the loop into one trading session: a soft core print argued the Fed could afford patience, and within hours the Commander-in-Chief had repriced the war premium that feeds the next headline number. Warsh is being asked to ease into an inflation shock his own White House keeps refueling. The Fed sets the price of money; it does not set the probability of airstrikes, and right now the second variable is doing more work on the US price level than the first.

The Dollar took the dovish read

The US Dollar Index (DXY) tagged the 100.00 handle in the minutes before the 12:30 GMT release, sold off to session lows roughly 30 ticks below it on the soft core, then spent the New York afternoon buying the move back in two distinct legs. The first leg was organic: dip-buyers ground the index off the lows well before the first support shelf even came into view, a market quietly declining to unwind six weeks of hike repricing on one soft core line.

The second leg was the war: within minutes of Trump's escalation comments, the index went vertical, reclaiming the handle to sit flat to marginally higher on the day, the daily candle as it stands all lower-wick. The index has rallied from below 98.00 in mid-May, cleared the 50 and 200 EMA cluster parked at 99.00, and stalled this week ahead of the spring highs, with the April peak above 100.50 the bigger ceiling. The soft core was the bears' best ammunition of the week, and it bought them three hours. The Dollar is running on two engines now, a December hike that refuses to price out and a war premium that refreshes with every headline, and the bid is intact.

Levels and the lean

100.00 is the pivot. Wednesday's rejection there hands the bears the short-term tape, and the bulls need the handle back on a closing basis before anyone talks about the April high. Above it, 100.50 is the spring ceiling; a daily close through that level on hot pipeline data would pull the December pricing forward and put a second 2026 hike on the table. Below, 99.50 is the first shelf, and 99.00 is the line in the sand, where the 50 and 200 EMAs sit beneath the early-June breakout base. Lose 99.00 on a closing basis and the hike premium built since mid-May starts unwinding toward 98.00.

While 99.00 holds, the lean stays higher, and dips are for buying. You can think the December hike is aimed at the wrong inflation and still respect that it is priced, and the next catalyst leans hot: Thursday's Producer Price Index (PPI) lands at 12:30 GMT with a 6.4% YoY consensus, up from 6%, after a 1.4% monthly jump in April. Producer prices running above 6% while consumer core runs 2.9% is the gap this entire debate lives inside. Thursday's print answers the only question today's CPI left open: whether the pipeline agrees with the pump. That answer is part two.

DXY 15-minute chart

Author

Joshua Gibson

FXStreet

Joshua joins the FXStreet team as an Economics and Finance double major from Vancouver Island University with twelve years' experience as an independent trader focusing on technical analysis.