Spotlight on PCE inflation and Fed Minutes after Powell hints at pause [Video]

![Spotlight on PCE inflation and Fed Minutes after Powell hints at pause [Video]](https://editorial.fxstreet.com/images/Macroeconomics/MonetaryPolicy/FED/new-us-2013-100-bill-federal-reserve-seal-extreme-macro-28149984.jpg)

As Fed officials contemplate whether to pause or not, some vital inflation data will be watched on Friday (12:30 GMT) in the form of the core PCE price index, while the minutes of the May FOMC meeting (Wednesday, 18:00 GMT) might further stir things up in the pause debate. One thing is clear though – the Fed has never been so data dependent and the June decision will likely be a very close call. So what should we expect from the incoming data and are there more gains in store for the US dollar?

More rate hikes to come?

Markets just can’t seem to make up their minds about a rate hike in June amid some conflicting views lately from policymakers about where they stand on the matter. Expectations had been low to begin with, but the hawkish bets started to gather steam when a majority of Fed speakers appeared to back another rate increase despite the Fed having opened the door to a pause at the last meeting.

However, not everyone is convinced that there is a strong enough argument to continue tightening, with Fed chief Powell being among those that have demonstrated a preference to pause. Powell and a few others at the Fed are wary about raising rates further given the lags in policy transmission and perhaps more importantly, the possibility that tighter lending standards following the banking stress may yet lead to some sort of a credit crunch.

The data-dependent Fed

The minutes of the May meeting might reveal more on just how much of a concern a credit squeeze is for the Fed. But aside from those discussions, the minutes are unlikely to offer any fresh insight for traders on where rates are headed.

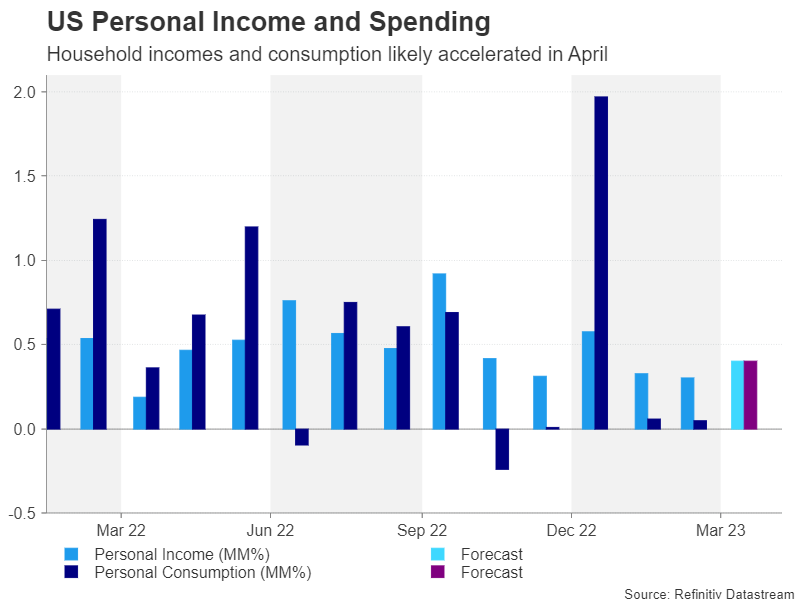

In truth, policymakers don’t seem to have decided how they will vote in June and will therefore be looking at the next batch of data very closely to guide them. Some of the releases on the agenda this week are the second estimate of Q2 GDP growth on Thursday and April durable goods orders on Friday. But investors will mostly be fixated on the PCE inflation and personal income and spending numbers, which will be crucial for the Fed to see whether or not underlying inflation is moderating and how well consumption is holding up.

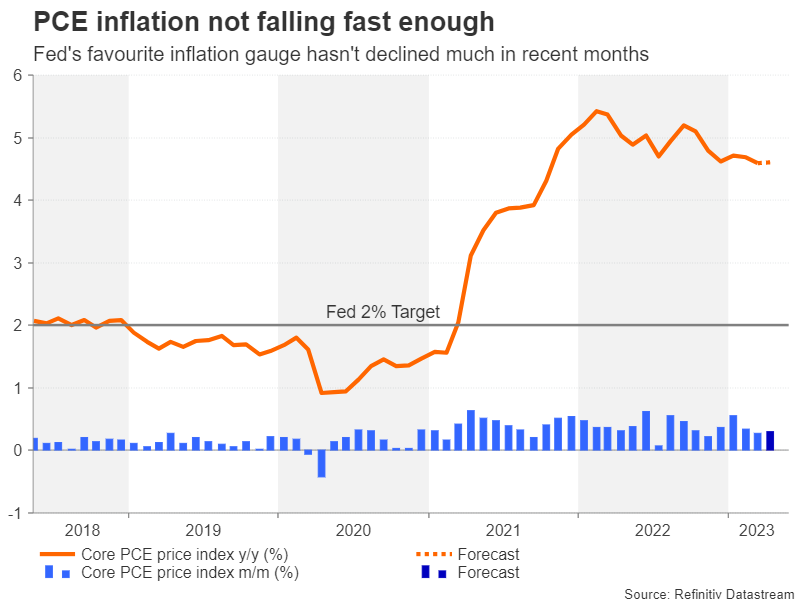

The stickiness of inflation

There can be no denying that headline inflation globally has come down substantially in 2023 as energy and other commodity prices have fallen, but core inflation is turning out to be a lot stickier than what central banks anticipated. In the US, the all-important core PCE price index has been stuck between 4.6% and 4.7% since December and the forecast does not point to any improvement in April.

It is expected to have stayed unchanged at 4.6% y/y. But the Fed might take some comfort from the monthly increase remaining at a reasonable 0.3% pace. One of the reasons why businesses have been able to continue passing on higher prices onto consumers is that households are still flush with cash as highlighted by the Fed’s Bullard this week.

Personal consumption is projected to have grown by 0.4% m/m in April, on the back of a similar increase in personal income.

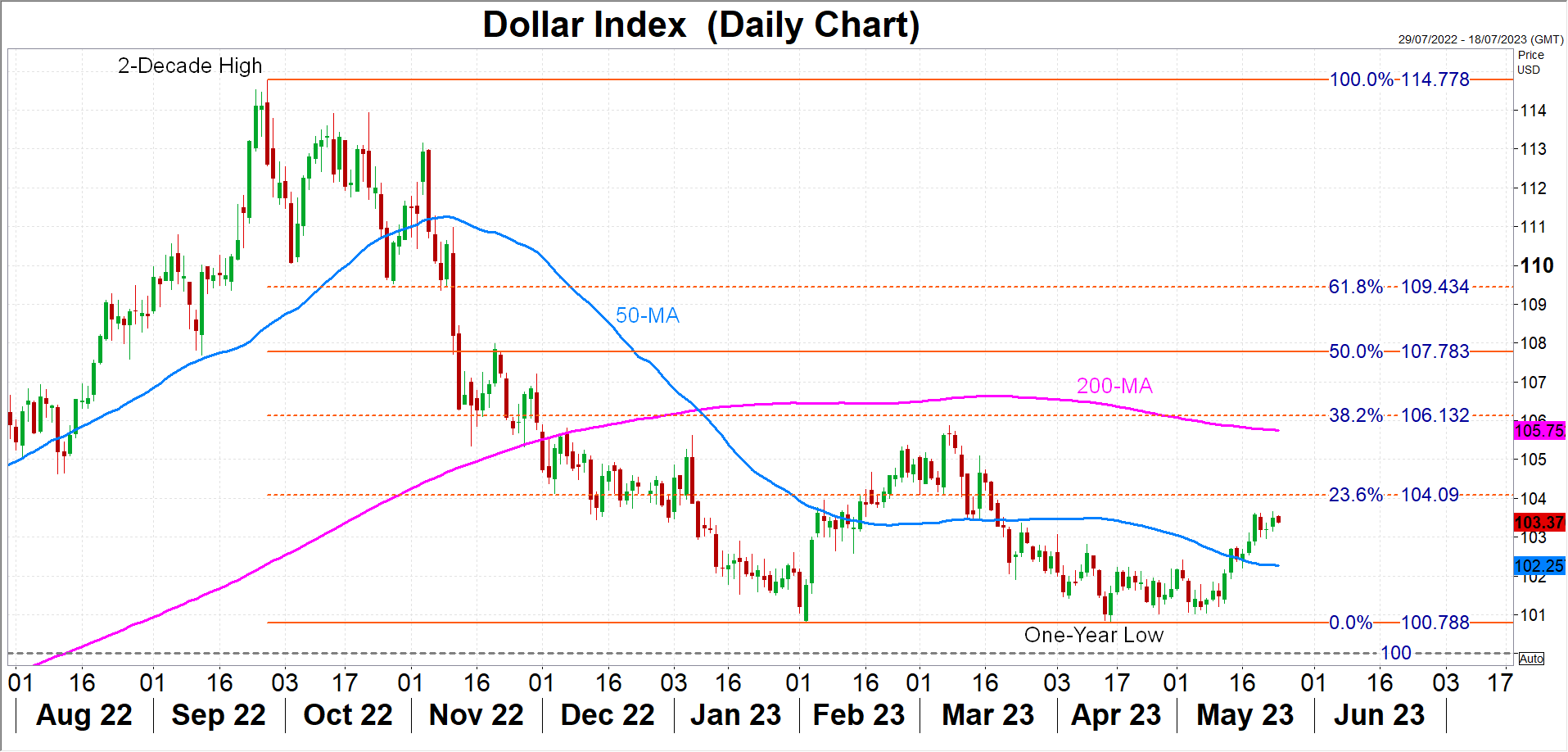

US Dollar: More upside, limited downside

With so many policymakers sitting on the fence, the above numbers are more likely to sway them towards a hike rather than a pause and add more wind to the dollar’s sails.

The dollar index is currently heading towards the 38.2% Fibonacci retracement of the September 2022-April 2023 downtrend at 104.09, having recently crossed above its 50-day moving average (MA). A break above the 23.6% Fibonacci would open the way for the 200-day MA at 105.77, not far below the 38.2% Fibonacci of 106.13.

However, a surprise drop in core PCE could spark a selloff in the dollar crosses, pushing the trade-weighted index back towards the 50-day MA, a breach of which would pave the way for a retest of the 100 level.

It’s worth noting, though, that expectations for rate cuts in the second half of the year have been scaled back significantly over the past week, mainly because the Fed will probably want to maintain a tightening bias after it’s paused, and that should support the greenback even if the data does not bolster the case for a June hike.

Author

Mr Boyadjian graduated from the London School of Economics in 1999 with a BSc in Business Mathematics and Statistics.