S&P 500 wavers after dovish Powell statement

The US dollar declined after Federal Reserve’s Jerome Powell shrugged the latest jump in US inflation. He said that the bank will act to keep inflation under control by raising interest rates and tapering asset purchases. Still, he repeatedly said that the bank still expected inflation to ease later this year. He testified to a congressional committee a day after data showed that the headline inflation rose at the fastest pace in 13 years. This inflation was mostly because of the ongoing supply logjam that has led to challenges in shipping. It was also because of the ongoing chip shortages that has pushed the prices of new and used cars sharply higher. The US dollar will react to the latest initial jobless claims numbers and the New York and Philadelphia Fed manufacturing index.

The Australian dollar rose during the overnight session mostly because of the dovish statement by the Federal Reserve. The currency also rose as the market reacted to strong economic data from Australia and China. The Australian employment data showed that the country added more than 29.1k jobs in June after adding 115k in May. Most importantly, the unemployment rate dropped from 5.1% to 4.9%, which was better than the median estimate of 5.0%. The participation rate remained intact at 66.2%.

Meanwhile, Chinese data showed that the economy grew by 7.9% in the second quarter. This growth was driven by a 12% increase in fixed-asset investment and a jump in export and local consumption. The country’s unemployment rate remained steady at 5.0% whole retail sales rose by 12.1% in June. These numbers show that the country’s economy is holding steady as the rest of the world recovers.

US stocks were relatively mixed on Wednesday as the earnings season continued. The Dow Jones and S&P 500 index rose slightly while the Nasdaq 100 index declined by 32 points. On Wednesday, some of the companies that reported their earnings were Blackrock, Bank of America, Citi, and Wells Fargo. Wells Fargo posted revenue of more than $20.27 billion, its highest growth since the pandemic started. On the other hand, Citigroup posted a profit of more than $6 billion while Bank of America recorded more than $9 billion. Morgan Stanley, Alcoa, and Progressive will publish their results today.

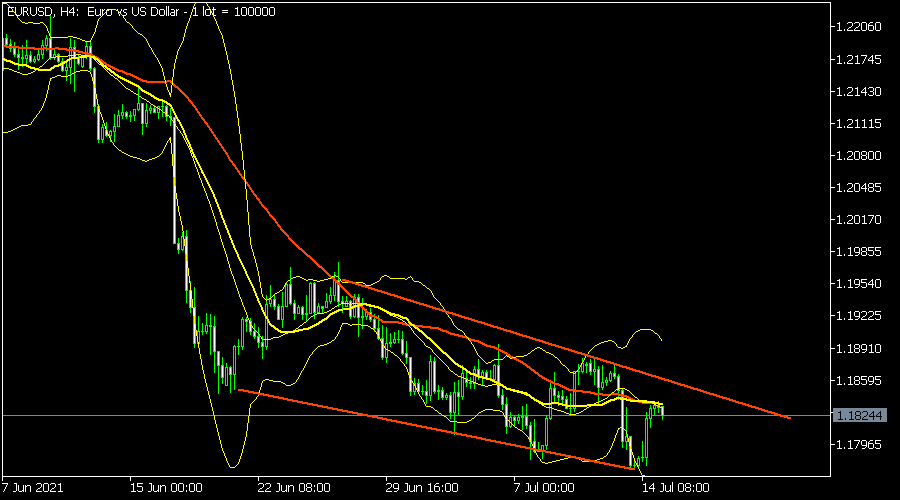

EUR/USD

The EURUSD pair rose to 1.1825, which was modestly higher than this week’s low of 1.1711. The pair is trading at 1.1825, which is a few pips below the 50-day and 25-day moving averages. It is also slightly below the upper side of the descending channel shown in red. The price is also along the middle line of the Bollinger Bands. Therefore, the pair will likely remain at this range ahead of the US manufacturing data.

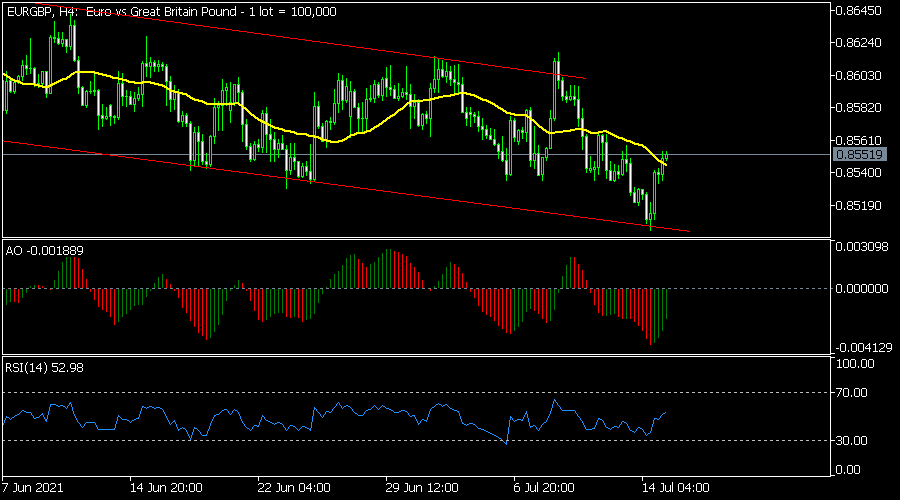

EUR/GBP

The EUR/GBP pair rose to 0.8552, which was higher than this week’s low of 0.8500. On the four-hour chart, the pair rose above the lower line of the descending channel. It also rose slightly above the 25-day moving average while the awesome oscillator is below the neutral line. The Relative Strength Index (RSI) has also risen to 53. Therefore, the pair will likely keep rising ahead of UK employment data.

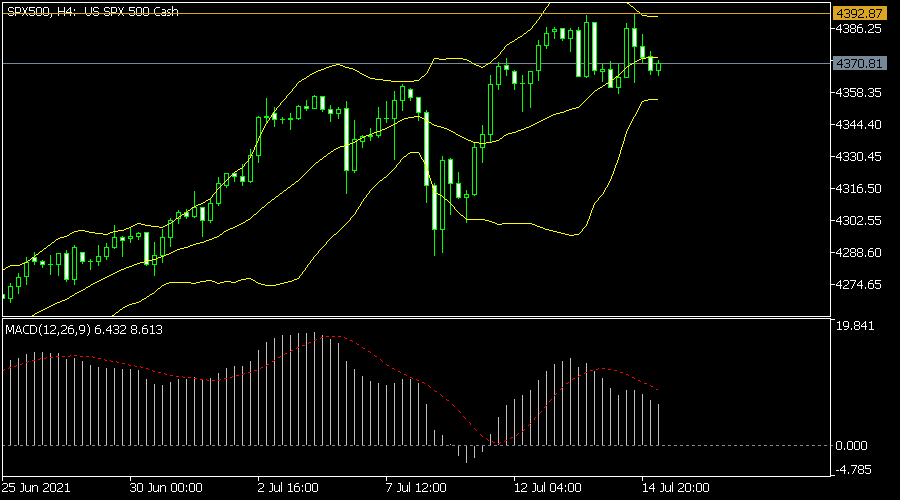

S&P 500

The S&P 500 index was little changed as the earnings season continued. The index is trading at $4,370, which is along the middle line of the Bollinger Bands. The stock is also slightly below the all-time high of $4,392. The histogram and line of the MACD have also moved above the neutral line. Therefore, the index will likely remain in this range as more earnings come in.

Author

OctaFx Analyst Team

OctaFX

OctaFX is a market-leading forex broker, providing personalised forex brokerage services to customers in over 100 countries worldwide.