Seven fundamentals to watch: US elections run-up, GDP and Nonfarm Payrolls mean a spooky Halloween

- Top-tier US data releases are set to rock markets around the turn of the month.

- Investors will also be watching last-minute opinion polls ahead of next week's US presidential election.

- The Bank of Japan will have its moment in the spotlight after the inconclusive Japanese elections.

- Volatility is set to be sky-high.

Spooked? Ahead of Halloween, markets opened with several gaps, most notably on Japanese Yen (JPY) charts, following the surprising election results in Japan. It is going to get even busier with the US presidential election coming soon – and a string of all-important macroeconomic data points.

Fasten your seatbelts.

1) Investors are paying attention to the election as control of Congress also matters

Will Vice President Kamala Harris win the world's top job? Or will former President Donald Trump make a comeback? The identity of the person who occupies the Oval Office is critical in many aspects, but for markets, control of Congress makes a big difference. The clock is ticking down to November 5.

Polls currently show a razor-thin edge in favor of Trump, but well within the margin of error. The 45th president promised high tariffs, which would be inflationary and cause higher interest rates. However, if his Republican Party wins control over both chambers of Congress, he would lower taxes, something markets love.

If Harris wins, it would set a historical precedent – the first woman president – but without control of Congress, it would represent a continuation of the current situation. A surprising victory for Democrats in both chambers of Congress would also be inflationary, as she promised big spending.

Investors will have to settle for opinion polls this week, and these could cause more confusion, especially those for swing states. The focus is on who leads the "Blue Wall" states of Pennsylvania, Michigan and Wisconsin. The second tier of states is in the south: North Carolina, Georgia, Arizona and Nevada.

Any poll from any of these states matters more than national ones.

2) JOLTS provide insights into the labor market in the absence of ISMs

Tuesday, 14:00 GMT. Every jobs-related report matters to the Federal Reserve (Fed) – which is focused on keeping it bustling after all but having declared victory on inflation. JOLTS matter, even though the data is for September, and not for October like the Nonfarm Payrolls (NFP).

JOLTS Job Openings surprised in August with a rise to 8.04 annualized million jobs, reflecting stability after the long decline from the recovery highs. Nevertheless, this is still a robust environment. A similarly strong figure would imply a higher path for rate hikes, weighing on Gold while boosting the US Dollar (USD) and stocks. A weak figure would do the opposite.

Another factor making JOLTs important is the fact that the ISM Purchasing Managers' Indexes are only published after Nonfarm Payrolls.

3) ADP to set the tone for Nonfarm Payrolls

Wednesday, 12:15 GMT. After shocking markets with weak data for August, America's largest payrolls provider surprised with an upbeat report for September – 143,000 private-sector jobs were created back then. The good news was followed by an even bigger surprise by the official Nonfarm Payrolls report. This is not always the case.

Despite having a weak correlation, ADP's report will likely shake markets, at least in the short term. Strong data is stocks and US Dollar bullish, Gold bearish. It later shapes NFP expectations. However, after the initial knee-jerk reaction – and unless there is a massive surprise – the move fades away. The release tends to provide an opportunity to go against it.

In this week's case, ADP's figure is quickly followed by another top-tier data point.

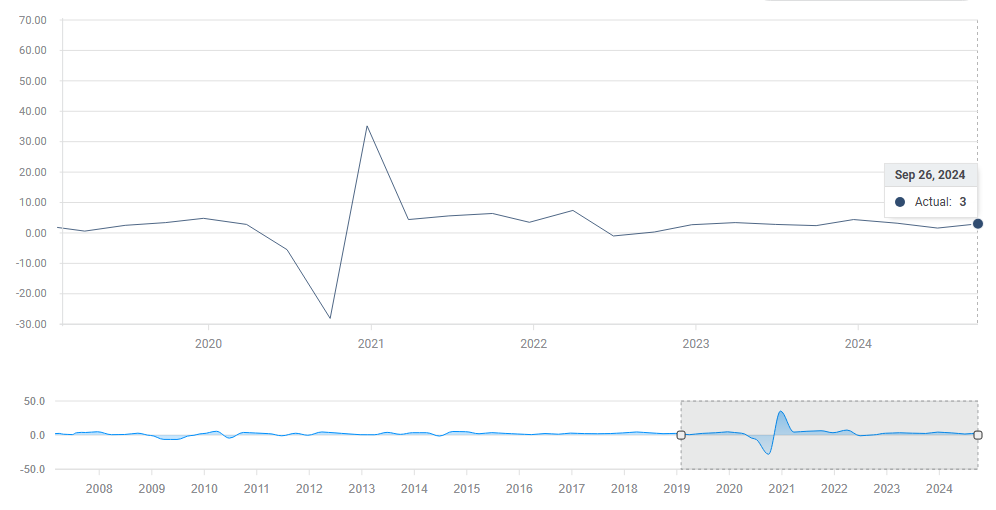

4) Advance Q3 GDP will likely show impressive US growth

US GDP. Source: FXStreet.

The world's largest economy grew at a fast clip of 3% annualized in the second quarter, and a similar expansion is expected for Q3. A small miss – which cannot be ruled out given the high expectations – would boost Gold while weighing on the US Dollar and stocks. A beat would do the opposite.

The impact on markets will likely be greater if both ADP and GDP go in the same direction – either beating or missing estimates. Otherwise, it will likely be messy.

5) BoJ will likely hide after the elections, weighing on the Yen

Thursday, early in Asia. Political instability has hit Japan's shores – the long rule of the Liberal Democratic Party (LDP) is in doubt after the party lost its majority in parliament for the first time since 2009. Even when adding its longstanding coalition partner, there is no clear majority. The opposition parties are fragmented as well, implying a long period of negotiations and political paralysis.

Under these conditions, the Bank of Japan (BoJ) may refrain from rocking the boat – which means no rate hikes, nor any hint of a change. That is bearish for the Japanese Yen. With no determined leaders in government willing to strengthen the Yen, the currency may suffer fresh falls.

6) Core PCE could have political implications

Thursday, 12:30 GMT. The core Personal Consumption Expenditures (core PCE) gauge is what the Fed targets. The central bank wants it to hover around 2%. The goal has almost been met, but the battle is not fully over yet.

While the earlier Consumer Price Index (CPI) report was published before the PCE one, this release for September impacts both the Fed and also the electorate. A weak report would benefit Harris, while high figures would boost Trump, whose campaign focused on inflation.

After a meager increase of 0.1% last month, a strong number is likely, given CPI and other figures. However, expectations of a 0.2% increase may be too much. A small miss would weigh on the US Dollar and boost Gold.

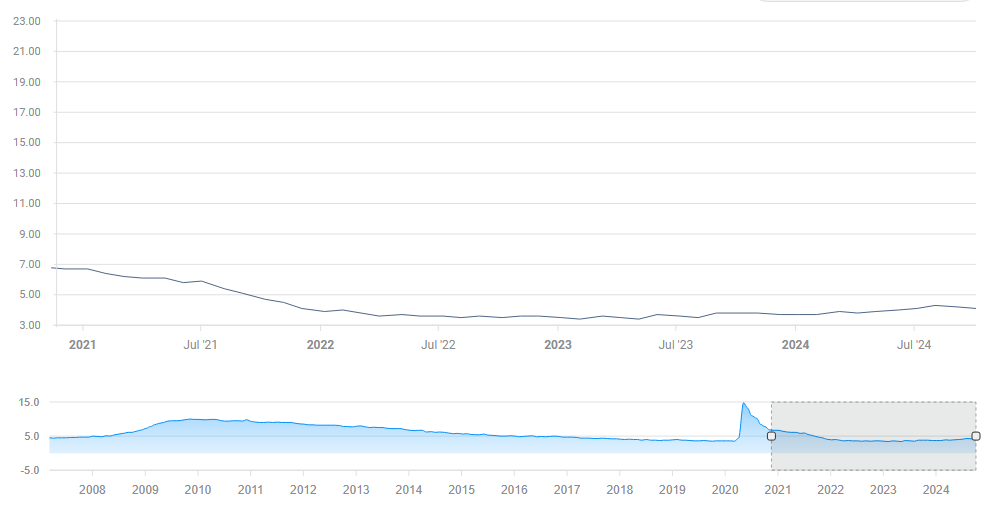

7) Nonfarm Payrolls have an outsized impact this time

Friday, 12:30 GMT. Just as Americans wake up after the Halloween parties, they might be spooked by October's Nonfarm Payrolls report. After a leap of 254K jobs in September, the NFP is expected to barely exceed 100K.

Why? There are several factors, from back-to-back hurricanes in the Southeast to a strike at Boeing and the volatility of the data. A better headline would support the US Dollar and stocks, while a weaker one would propel Gold higher.

The Unemployment Rate is of high importance as well. It retreated to 4.1% in September after peaking at 4.3% in July. A repeat of that 4.1% level is on the cards for October, but anything could happen.

US Unemployment Rate. Source: FXStreet

A disappointing increase would improve Trump's chances of winning the close contest, while a drop to 4%, and especially below, would support the Harris campaign. The economy is the #1 issue for Americans.

Final thoughts

The seven points above are all important, and several others did not make the cut, such as ongoing geopolitical tensions in the Middle East. These have dropped following the Israeli attack on Iran, which was seen as limited.

Another factor worth mentioning here is end-of-month flows around Halloween, but with so much economic data and opinion polls, the normally erratic flows might fail to stand out. Volatility is set to be high with or without these erratic moves on October 31.

Trade with care.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.