Nonfarm payrolls: Testing the limits of Fed policy patience

- US nonfarm payrolls for May due Friday at 12:30 GMT.

- Analysts forecast slower jobs growth but a resilient labor market.

- Upside surprises remain possible, threatening more gold pressure.

Nonfarm payrolls to extend slowdown through May

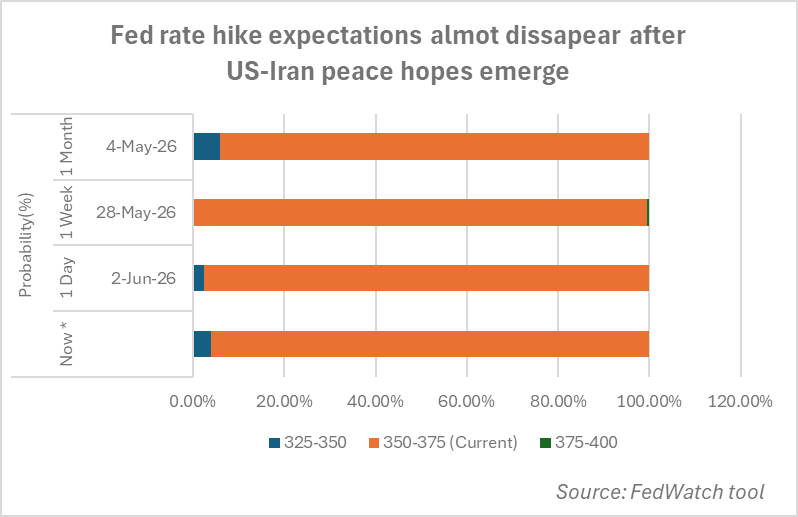

The upcoming nonfarm payrolls report for May will provide the final update on the US labor market before Kevin Warsh attends his first policy meeting as the new Fed Chair later this month. Traders are now forecasting a slowdown following two months of triple-digit employment increases, which had reinforced the perception of a resilient labor market despite a volatile geopolitical backdrop that continues to fuel concerns over persistent inflation and elevated global interest rates.

April’s report showed that 115k jobs were created, marking a slowdown from March’s robust 178k increase, though enough to keep the possibility of another Fed rate hike alive last month. However, in recent weeks, hopes for a US–Iran framework agreement, which could ease tensions around the Strait of Hormuz, alongside a stabilizing core PCE inflation reading, have shifted market expectations firmly toward steady interest rates, with the case for a rate hike now largely disappearing.

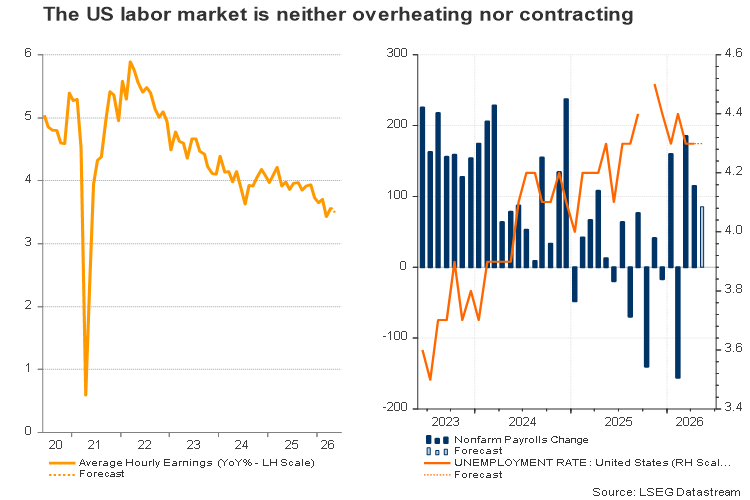

Investors expect jobs growth to slow further to around 85k in May, while the unemployment rate is projected to remain steady at 4.3%. Average hourly earnings are anticipated to rise by 0.3% month-on-month from 0.2% previously, while annual wage growth is expected to ease slightly to 3.5% from 3.6% previously.

Will a pullback in jobs growth stress markets?

The key question now is whether softer payroll growth would signal broader weakness in the labor market. Most likely, not yet. Investors may still interpret the data as consistent with a gradual normalization in hiring conditions rather than a sharp deterioration. Moreover, the possibility of another upside surprise cannot be ruled out, as graduation season and increased summer hiring activity could support fresh labor market entries.

How might Kevin Warsh react to the NFP report?

On the other hand, the latest decline in the quits rate suggests that labor market conditions are not entirely robust, as worker confidence appears somewhat cautious amid elevated geopolitical uncertainty. Even so, this environment could encourage Kevin Warsh to remain patient and closely monitor incoming economic data rather than pivot toward easing or tightening too quickly, especially with Treasury yields continuing to hold above 4.0%.

Furthermore, delivering immediate rate cuts in line with President Trump’s calls may prove difficult given the hawkish tone of the latest Fed minutes and the need for broader committee support. Such a move could also raise concerns over the Fed’s independence and potentially undermine the Chair’s credibility.

Conversely, a stronger-than-expected triple-digit payroll print could revive expectations for another rate hike or strengthen the case for continued quantitative tightening, an issue Kevin Warsh previously emphasized during his Senate hearing.

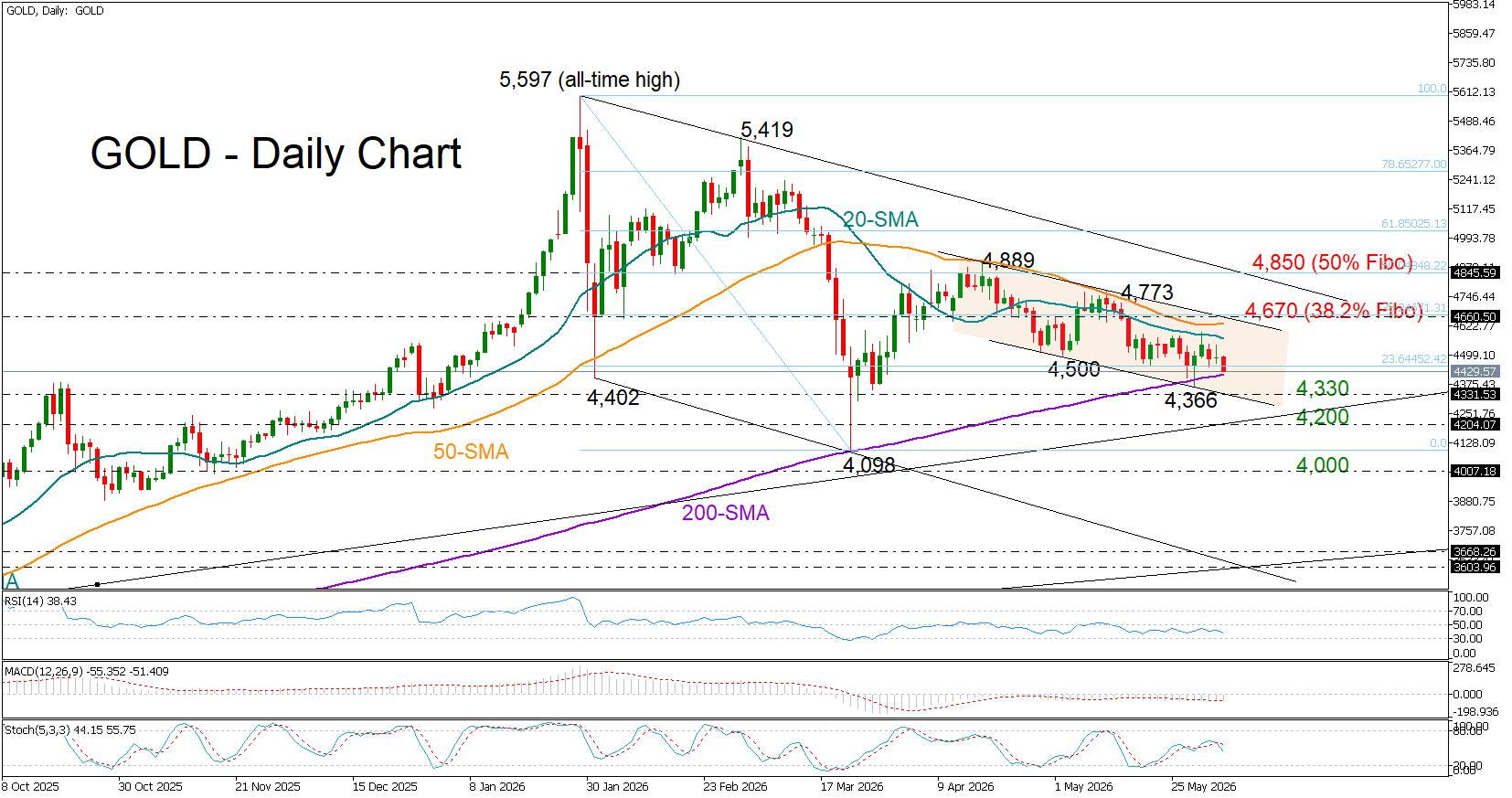

Gold levels to watch

If the data beats expectations by a wide margin, Treasury yields could rebound again, putting additional pressure on gold and potentially pushing the metal below its 200-day simple moving average (SMA). In that case, initial support may emerge near $4,340/ounce, while a deeper correction could target the $4,220 region.

Alternatively, a weaker-than-expected employment report may still leave the Fed on hold for the foreseeable future, as policymakers continue to balance softer growth signals against persistently elevated inflation pressures.

Author

Christina joined Trading Point in May 2017. She holds a master degree in Economics and Business from the Erasmus University Rotterdam with a specialization in International economics.