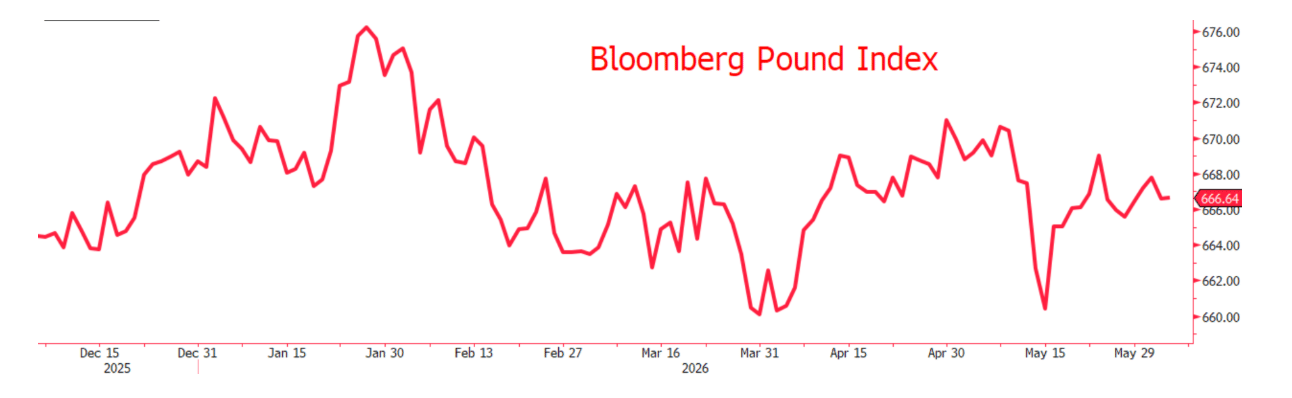

Prospect of no BoE cuts spells bad news for Sterling

The OECD printed their forecast for the Bank of England’s interest rate by the end of the year, suggesting no hikes this year and then cuts to follow in 2027. Whilst this may sound counterintuitive at first, with almost every other G-10 Central looking to raise rates to try and pre-empt rising energy prices, there is good reason to consider the viability of the suggestion.

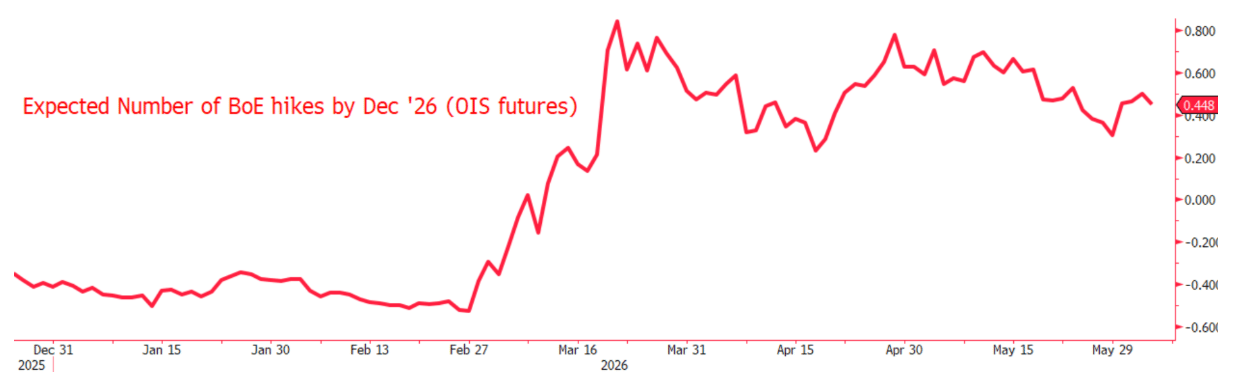

Futures pricing shows an expectation of nearly two interest rate hikes from the Bank of England this year, against just over one being expected from the Fed and nearly three from the ECB over the same period. The effects of higher energy prices are already being reflected in US and European CPI figures, with both seeing their highest inflation rates since 2023, whilst UK inflation fell to its lowest for a year.

OFGEM’s price cap, which will only be increased forward of July, does insulate UK consumers from these kind of short sharp shocks and with LNG prices, a more important figure for the UK given the heavier reliance on LNG, dropping sharply, it seems likely that we will land somewhere between Scenario A and B that the BoE laid out during their last interest rate meeting.

The dreaded Scenario C that briefly sent markets scarpering seems a remote possibility now, provided Iranian concerns regarding the invasion of Lebanon can be addressed soon. Most importantly regarding this point is that by the Bank’s own statement during the April 30th meeting, Scenario A and B do not necessitate interest rate hikes, the Taylor rule suggests that the Bank may consider 1 hike, but 2 would be overtightening.

Moreover, whilst the 100,000 net jobs lost in April figure will almost certainly be revised lower, the UK labour market has been in steady decline at least since 2024 and with recent Government changes to employee entitlements as well as the pressure of AI, the BoE has another reason to be cautious regarding raising rates.

Recent data also suggested that redundancy rates in the UK have hit their highest since 2020, exacerbating existing concerns of a more serious softening in the labour market.

The broad implication of this is that the Pound could be ripe for a correction if the BoE leans into the suggestions of keeping the base rate unchanged this year during their June 18th meeting. Whilst MPC members will likely play it safer than to openly suggest no hikes this year, the market will soon realise that the BoE is, and has been for some time, an unenthusiastic tightener of policy.

Author

David Stritch

Caxton

Working as an FX Analyst at London-based payments provider Caxton since 2022, David has deftly guided clients through the immediate post-Liz Truss volatility, the 2020 and 2024 US elections and innumerable other crises and events.