September FOMC Preview: Projections, projections, projections

- Fed funds rate to be unchanged, pandemic relief programs to continue.

- Third set of 2020 economic projections due on rates, GDP, unemployment and inflation.

- June estimates were 0.1% fed funds and 5.5% unemployment at the end of 2022.

- Dollar has been susceptible to the Fed’s rhetoric on inflation and growth.

The Federal Reserve’s long standing failure to raise inflation to its target in the decade since the financial crisis has resulted in the new inflation averaging goal that is as much an admission as it is a policy.

Prices will now be permitted to run above target for long periods in order to bring the overall average up to 2%. This will permit the Fed to keep rates at the zero bound indefinitely as it seeks to revive the economy crippled by the pandemic shutdowns.

As a policy catalyst inflation has not been important since 2008 as the bank first worked to secure the US and global banking system and then restart the economy after the housing bubble and recession. The policy choice for the economy and inflation were the same then as they are now, zero rates. The only question was and is, for how long? After the 2008 collapse the Fed kept the funds rate at the 0.25% upper target for seven years.

With the most catastrophic economic event since the Depression in the forefront of business and government planning the Fed’s view forward is of prime importance. Even if their predictive success is no better and occasionally worse than the credit markets, the governors’ outlook can send traders running.

Projection materials and the dollar

The Fed’s economic estimates are normally updated four times a year but the March version was cancelled as was the scheduled meeting on the 18th and the materials were delayed until June. In the turmoil of the shutdowns it was a easy decision.

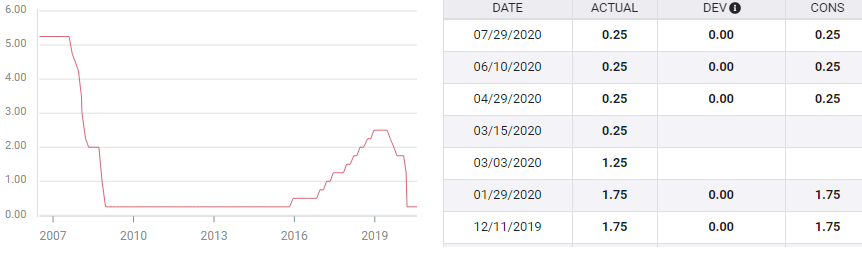

In the final projections of 2019 in December with the fed funds at 1.75% the bank predicted 1.6% at the end of 2020, 1.9% in 2021 and 2.1% in 2021. The final category called ‘longer run’ but without a specific time frame, saw rates at 2.5%, which we may take as the Fed’s neutral rate for the economy.

Fed funds rate

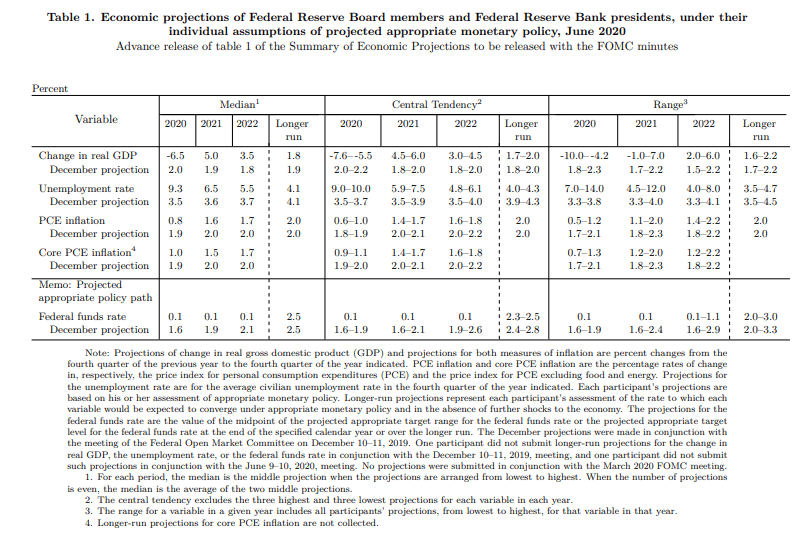

By June, after the closures and the precipitate plunge in GDP, employment and economic activity the rate estimates became 0.1%, through the end of 2022. The final long term prediction was unchanged at 2.5%.

It is on that longer term that the market will initially focus. Any drop in that rate will signal the Fed’s uncertainty over the recovery and will reinforce the weaker rate and dollar view inherent in the inflation averaging policy.

The projections for the core PCE inflation rate in June, 1.0% in 2020, 1.5% in 2021 and 1.7% in 2022 with no long term estimate, will be of secondary attention as the fed funds prediction incorporates the inflation outlook.

The projections for annualized GDP, currently -6.5% in 2020, 5% in 2021 and 3.5% in 2021 with 1.8% longer term, which again we may take as the Fed’s neutral estimate and unemployment, 9.3% this year, 6.5% next year and 5.5% in 2021 with 4.1% beyond will not to move markets.

Conclusion and the dollar

The Fed’s policy prescriptions are not available for change. Consequently it is the bank’s view forward that will have the most impact on markets.

Fed predictions come in two varieties, the Projection Materials that will be released at 2 pm EDT with the rate decision and Chairman Powell’s economic characterizations in his prepared remarks and news conference beginning at 2:30 pm. The chairman has been unduly cautious over the past several months warning that the recovery is dependent on the course of the virus. The new inflation averaging goal puts that caution into official policy.

Since early June the second wave of COVID-19 which seemed so threatening in the summer, has largely subsided with little increase in hospitalization or fatalities. The economy is expected to rebound sharply from its 31.8% lockdown crash, with the Atlanta Fed estimate for the third quarter at 30.8% as of September 10.

Economic statistics have been promising. Consumption, payrolls, business sentiment and manufacturing activity have been good even if initial jobless claims continue at nearly one million a week.

The brightening picture and the dollar would certainly be enhanced by some optimism from the Fed Chairman.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.