September CPI preview: Better late than never

Summary

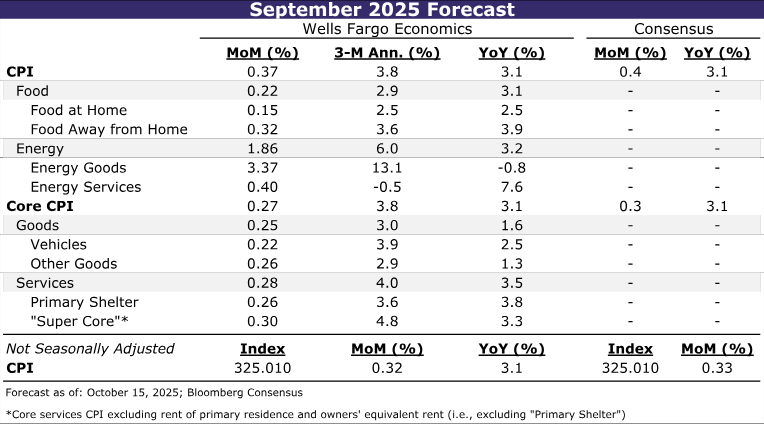

The government shutdown may have altered the September CPI release date, but it hasn’t changed the stubborn state of inflation. We estimate headline CPI rose 0.4% last month, underpinned by a jump in energy prices, which would lift the year-over-year rate to a 16-month high of 3.1%. Core inflation likely rose 0.3% for the third consecutive month, holding the year-over-year rate steady at 3.1%. Beneath the surface, we expect goods inflation to stay elevated due to continued tariff pass-through, while an easing in primary shelter costs should help cool services inflation.

We are not concerned about the federal government shutdown affecting the quality of the September CPI data since BLS collections proceeded through the end of the month, as scheduled. But as the shutdown drags on with no end in sight, risks are mounting for October’s report. At a minimum, collection rates stand to be lower with data gathering still suspended, and the risk is rising that the publication of the October CPI report could be skipped entirely.

Setting aside the near-term data challenges, sticky inflation persists. We expect inflation to hold near a 3% annualized pace through mid-2026, as the full brunt of tariffs has yet to feed through to goods prices and consumers' general resilience limits a further slowing in services inflation.

Source: U.S. Department of Labor, Bloomberg Finance L.P. and Wells Fargo Economics

Author

Wells Fargo Research Team

Wells Fargo