Sentiment picks up on Trump’s 'productive' trade comments, but can it last?

Market Overview

Concerns surrounding the warning signals that bond markets are throwing off have not gone away, but they have been alleviated slightly in the past 24 hours. With the inversion of the US Treasury yield curve, traders have been grappling with the notion that the US economy could be headed for recession. However, strong US Retail Sales data has followed Tuesday’s positive read through of US inflation, and helped to eased as least some of this recessionary panic domestically. Furthermore, on the international stage, comments from President Trump about “productive” trade talks with China and a likely meeting in September have also calmed some nerves. A pick up in risk appetite has resulted, seen primarily through higher Treasury yields (the 2s/10s spread is now +3bps) and equities. However, the calm is unlikely to last and it is interesting to see that in the currency space, the yen continues to perform well. Gold is around half a percent off, but just unwinding yesterday’s gains and performance across the week remains positive. This suggests a cautious market and any recovery could be fragile. How traders respond to a rebound to this sentiment will be key. With the recovery in Treasury yields still very minor and China continuing to set a yuan mid-point ever weaker (with Dollar/Yuan) above 7.00, sentiment recoveries will be tentative.

Wall Street closed with minor gains, with the S&P 500 +0.2% at 2847, however, US futures are showing much better today with gains of +0.7%. In Asia the cautiously positive outlook continued, with the Nikkei +0.2% and Shanghai Composite +0.8%. European markets are following US futures higher, with the FTSE futures +0.7% and DAX futures +0.7% higher. In forex, the outlook is still fairly mixed across major pairs, with little real direction on EUR or JPY. GBP is once more building higher, but is it a move that can last this time? It is a mixed picture for the commodity majors, with AUD still doing well, but NZD lagging slightly. In commodities, there is a mild unwind of gold this morning, whilst oil has jumped higher on the improved risk sentiment today.

The US consumer is the main focus on a US centric day on the economic calendar today. However, first up is the US Building Permits at 1330BST which is expected to show at 1000BST which are expected to improve to 1.27m in July (from 1.23m in June), whilst Housing Starts are expected to improve marginally to 1.26m (from 1.25m). The first reading of August’s Michigan Sentiment at 1500BST will be key today. The prelim sentiment reading is expected to slip back to 97.2 (from 98.4 in July). This is expected to be driven by a sharp decline in the Michigan Expectations component back to 89.0 (from a final 90.5 in July) whilst the Michigan Current Conditions component is expected to drop back to 110.4 (from a final reading of 110.7)

Chart of the Day – EUR/JPY

Volatility has been a feature throughout this week, with the bulls failing to mount any serious recovery. This is leaving the yen bulls as the dominant force still, pulling EUR/JPY lower. Once more during yesterday’s move, an intraday rally failed and was simply seen as another chance to sell. With negatively configured momentum this is likely to continue. With another multi-year closing low, the bears are building at pressure on the support around 117.50 which has been tested on numerous occasions in the past two weeks. With downside potential on RSI, whilst MACD and Stochastics track lower and remain negatively configured, additional downside is likely. A close below 117.50 opens the April 2017 low at 114.80 as the next realistic support. The hourly chart shows resistance 118.40/118.95 to use as a chance to sell.

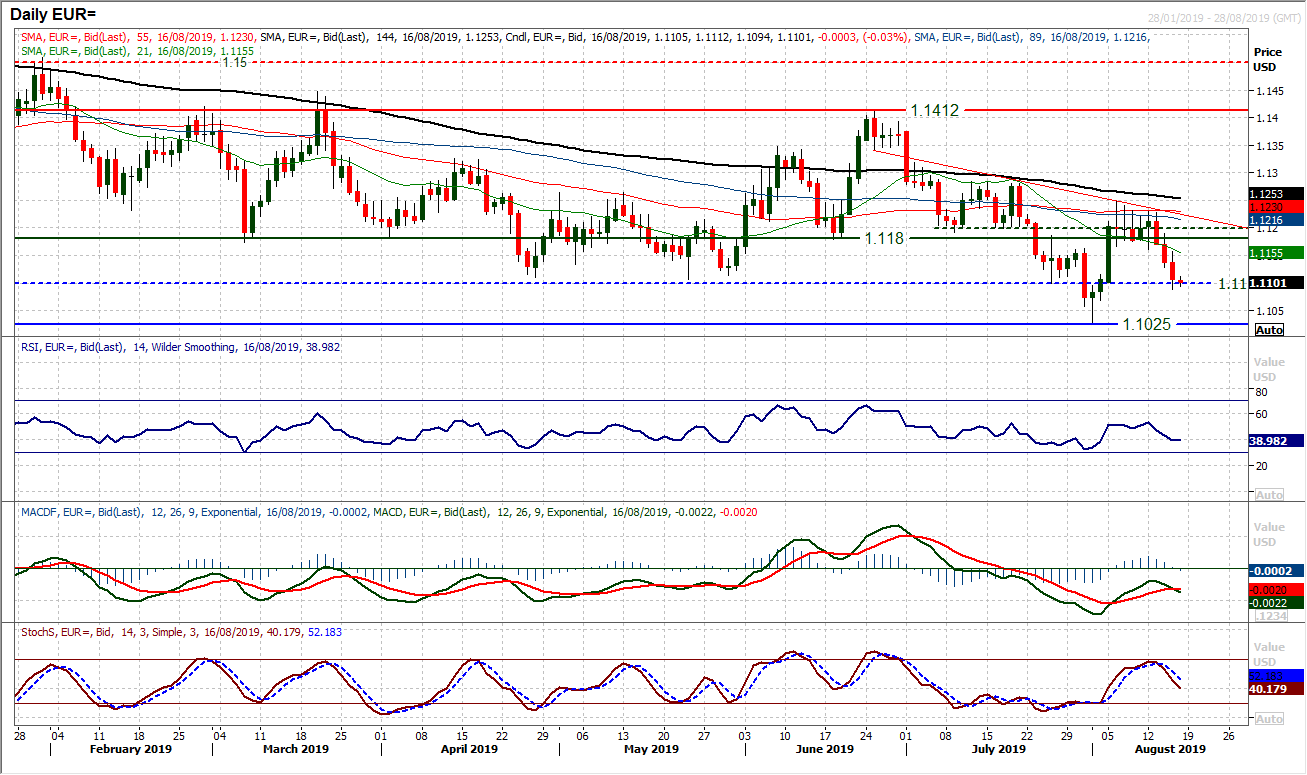

EUR/USD

The negative candles are beginning to build up again on EUR/USD. A period of consolidation is now being replaced by renewed negative bias. The resistance band of the pivot between $1.1180/$1.1200 has been bolstered and the market is now testing the old $1.1100 low again. Momentum indicators have rolled over and reflect a market seeing intraday rallies as a chance to sell. The Stochastics bear crossed earlier this week and the MACD lines are now crossing back lower below neutral. The hourly chart shows near term overhead supply has formed around $1.1160/$1.1165 from last week’s mini range, an area that captured yesterday’s high. Hourly indicators are also pointing to selling into near term strength, with the hourly RSI failing between 50/60 and MACD lines consistently under neutral. A close below yesterday’s low at $1.1090 opens the key low at $1.1025.

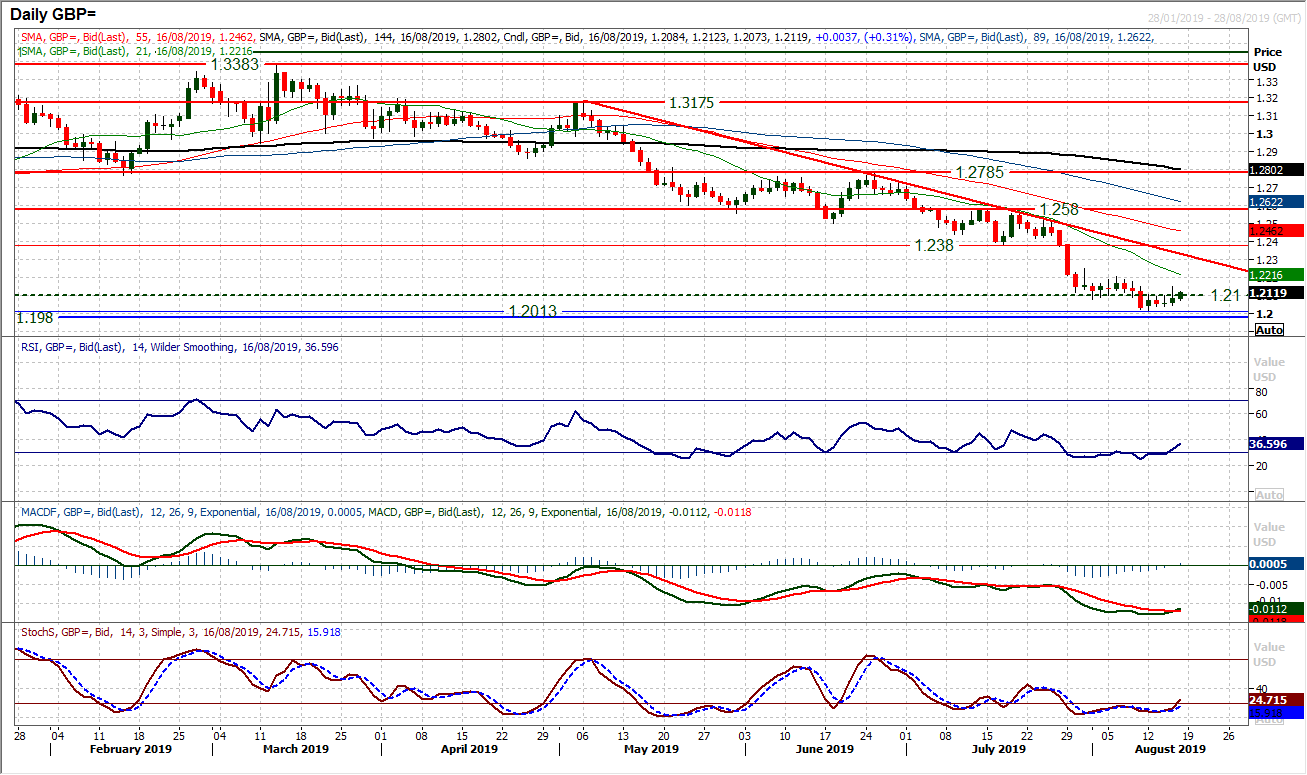

GBP/USD

Although sterling has picked up marginally in the past few sessions, it is still difficult to see any path towards a sustainable recovery at this stage. The selling pressure has seemingly dissipated, for now, at this week’s low of $1.2013 in a move that has completed three positive closes in the past four sessions. Momentum indicators are threatening to tick higher, but this is all still just playing out within strongly negative medium term configuration. Rallies are still a chance to sell. This was seen in yesterday’s failure at $1.2150 to close back under the old support around $1.2100 again. Resistance is building between $1.2150/$1.2250 now, comprising of highs of the past couple of weeks. The falling 21 day moving average which has been a gauge for resistance in recent months is also now at $1.2215. We continue to expect rallies to be short-lived and further pressure on $1.2013, with the crucial low at $1.1980.

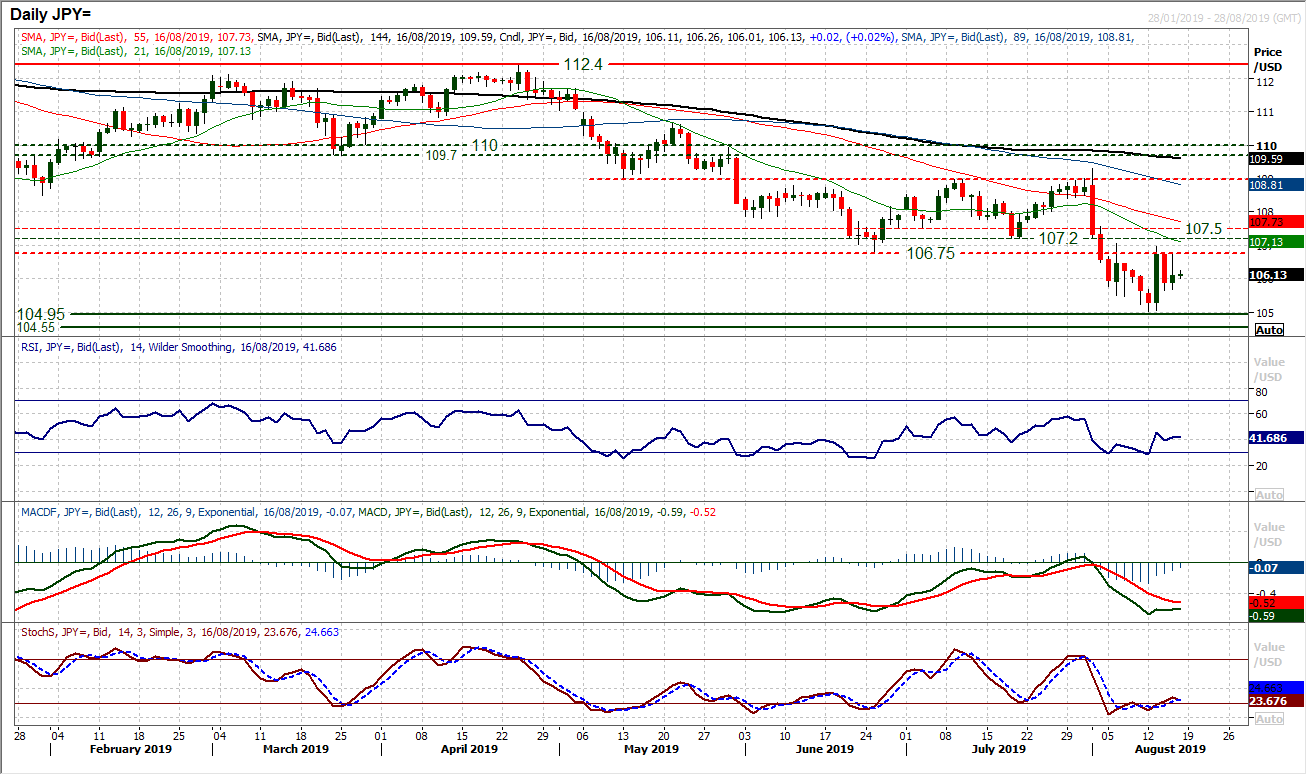

USD/JPY

With the dollar seeing a pick up yesterday, the reaction of the bulls around the 106.75 old low seems to be increasingly important for the near term outlook. This marks the beginning of a band of overhead supply 106.75/107.50 which has been restricting the recoveries in the past couple of weeks. Once more we saw this yesterday in what has been a continuation of elevated volatility in recent sessions. The bulls need to drive a close above 106.75 to get any realistic footing in this market now. Momentum for a recovery remains subdued and we continue to see near term strength as a chance to sell. A close above 106.75 would begin to question this outlook, but a bull failure in the 106.75/107.50 band would continue the negative outlook. The hourly chart looks increasingly settled as consolidation builds above initial support 105.50/105.70.

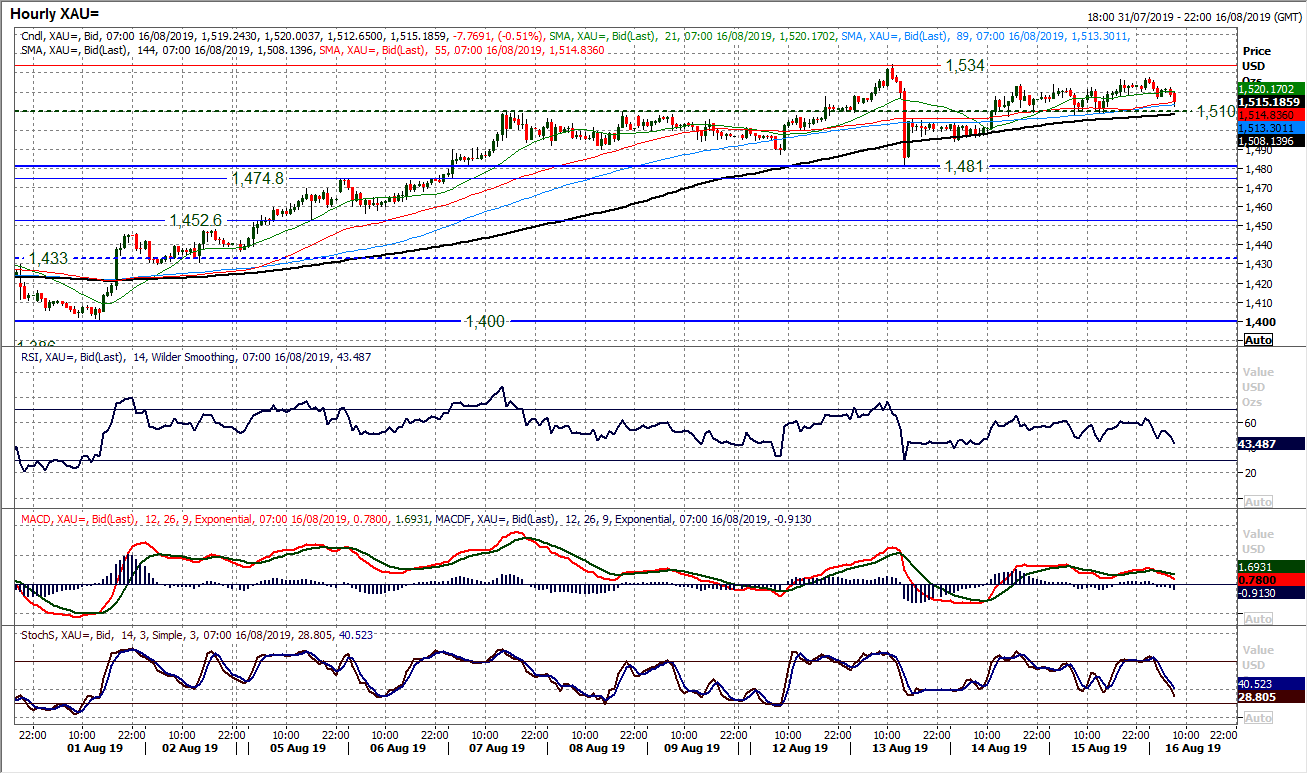

Gold

It is interesting to see that in spite of what was a broad improvement in risk appetite yesterday along with support for the dollar, we continue to have a gold price that manages to keep the profit-takers largely at bay. There has been a sense that gold is showing a mildly positive bias but there is potential that it is developing a near term consolidation. After Tuesday’s volatile session the market is beginning to settle down a bit more. Leaving support at $1481 a couple of positive candles have pulled the market back higher and maintains the outlook that weakness is a chance to buy. Looking on the hourly chart, the market is holding above $1510 which is a near term pivot and there is a slight positive bias. However, this is more of a drift higher than a decisive trend, whilst the market remains under the resistance at $1534. Continued trading above $1510 will maintain this positive bias for pressure on Tuesday’s multi-year high of $1534. There would be a sense of loss of momentum should $1510 be decisively broken as support, with the psychological $1500 and then $1481 being key near term.

WTI Oil

A downtrend since April links a run of lower highs and given the negative medium term configuration on momentum indicators, the outlook remains one to sell into strength. Since that April high, the signals on MACD lines have been reliable indicators, so the latest coming together of the lines needs to be watched. However, the Stochastics have just bear crossed and this is a concern. This week’s high at $57.45 has threatened to pull the market back lower again, with the weight of momentum suggesting that this early bounce this morning will be seen as another opportunity to sell. The old 38.2% Fibonacci retracement at $55.55 is a basis of resistance today. We expect another lower high formation and further pressure back on the support $53.50/$53.75.

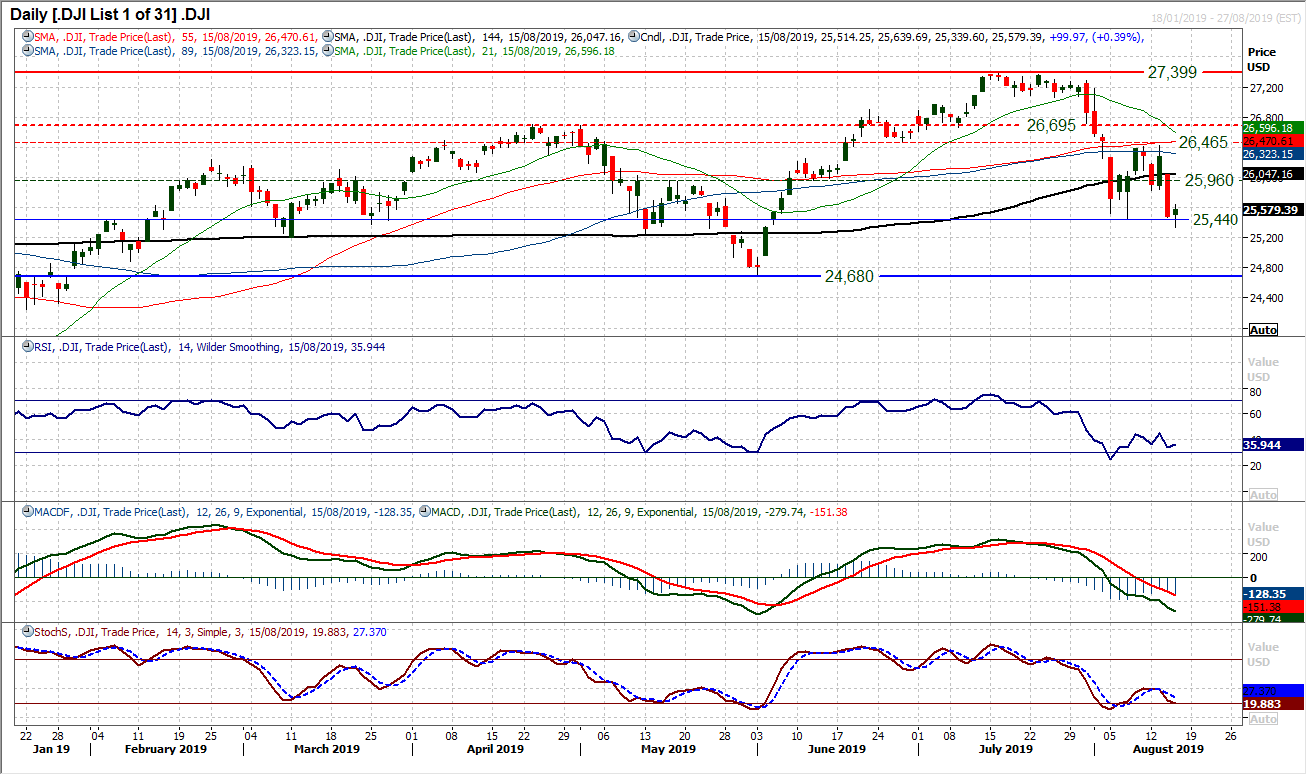

Dow Jones Industrial Average

After the rather tumultuous past week on Wall Street, yesterday’s mild positive session will have come as something of a relief. Although an intraday breach of support at 25,440 was seen, a close higher on the session has added a degree of calm to proceedings. A rally into the close helps with momentum too, with the Stochastics just looking to bottom out again. However, MACD lines are still falling and RSI is still subdued. There is an improvement also threatening on the hourly chart, with the RSI up off 30 as hourly MACD and Stochastics look to bull cross. With futures pointing to a decent open today the prospect of a rally to test initial resistance at 25,825 is growing. Key resistance is up at 26,400/26,425. The key for the bulls will now be looking to form a higher low above 25,340.

Author

Richard Perry

Independent Analyst