Risk positive on China trade data but dollar strength still looms

Market Overview

Markets are being pulled around by two forces at the moment, with the trade story being countered by dollar strength impacting across major markets. First of all there is a risk positive view being taken from the apparent progress of the trade negotiations between the US and China. The rhetoric in recent days has been constructive coming out of Beijing, whilst reports suggest a meeting between presidents Trump and Xi is in the offing (to presumably finalise a new relationship). Markets like this, with bond yields pulling higher and equities also stronger. However, the relatively stronger economic performance of the US is impacting through markets. Data out of the Eurozone continues to reflect a slowdown (and could show Germany moving into recession today), whilst the US is standing firm. Yesterday’s upside surprise on US inflation is driving traders to take a view on a continuation of the US dollar strength of the past couple of weeks. There will be further meat to the bones today for the US economic picture, with retail sales, but another strong number could really put the dollar on a strong footing. Confirming a move below $1.1300 on EUR/USD would be a real signal of continued gains for the dollar. In the meantime, there has been a mild risk rebound today which is coming on the back of some positive data out of China. The China Trade Balance came in much better than expected at +$39.2bn (+$33.5bn exp, +$57.1bn in December), whilst both exports and imports were also much stronger in January than they were 12 months ago. Chinese exports climbed by +9.1% (-3.2% exp, -4.4% last) whilst imports fell by just -1.5% (-10.0% exp, -7.6% last).

Wall Street closed higher again last night with the S&P 500 +0.3% at 2753 whilst US futures are similarly higher today. In Asian markets there has been a mixed session with the Nikkei all but flat, whilst the Shanghai Composite was -0.1% lower. In Europe, this theme of a mild risk positive move is coming with the FTSE futures and DAX futures both around +0.2% higher. In forex, the improved sentiment is showing through continued yen underperformance whilst the commodity currencies all perform well on the back of the China story. There is a mild rebound on sterling and the euro. In commodities there has been a rebound on silver after yesterday’s break below the $15.60 pivot support, whilst gold has also bounced. Oil continues its rebound climb of recent days.

In the morning of the European session, the focus for the economic calendar will be the Eurozone Flash Q4 GDP which is expected to be +0.2% for the quarter (+0.2% final Q3) whilst on a year on year basis this is expected to show +1.2% (+1.7% in Q3). Into the European afternoon the US data starts at 1330GMT with Retail Sales for December which is expected to show growth of +0.1% on an ex-autos basis (+0.2% in November), whilst January US PPI is expected to slip to +2.1% on headline PPI basis (from +2.5% in December), whilst core PPI is expected to drop to +2.5% (from +2.7% in December). Weekly Jobless Claims are expected to drop slightly to 225,000 (from 234,000 last week).

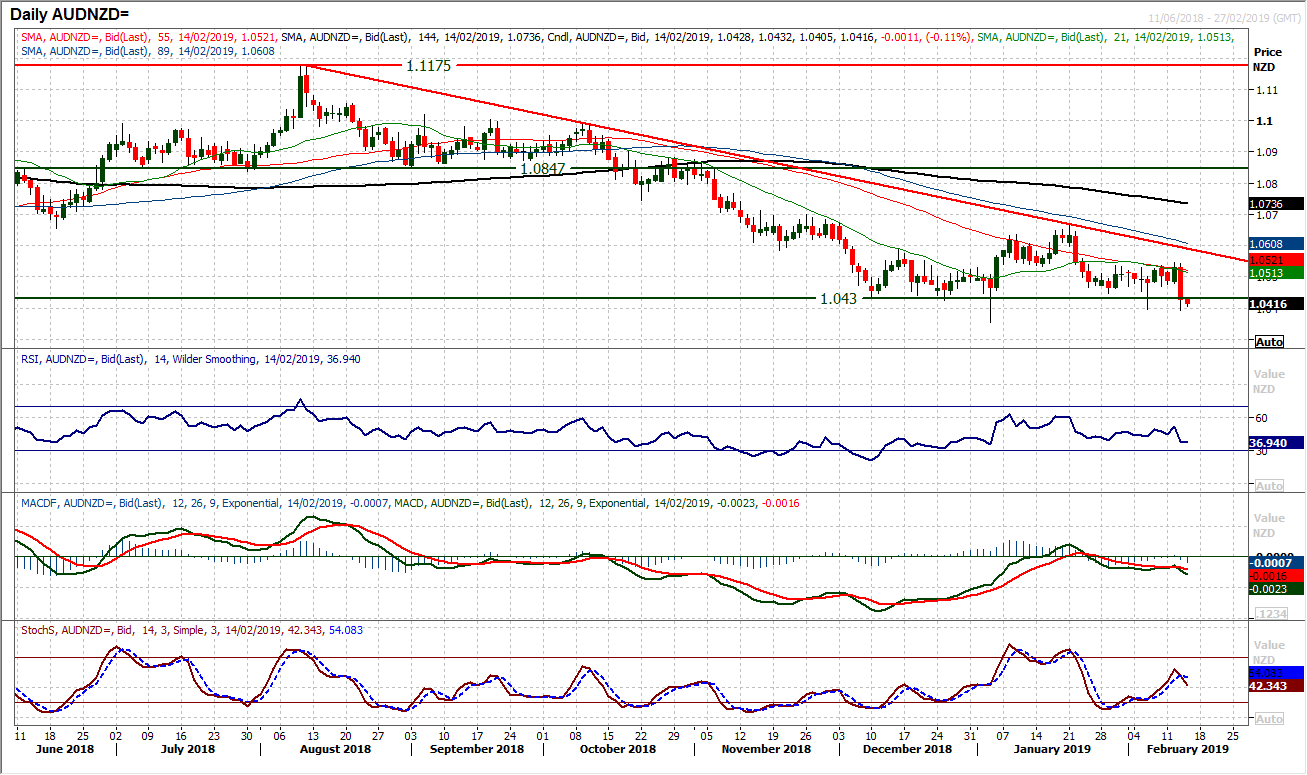

Chart of the Day – AUD/NZD

The bear trend of Aussie/Kiwi since August 2018 remains on track but in the wake of the surprisingly upbeat RBNZ yesterday this may not have been given extra momentum for the next leg lower. Since hitting a low of 1.0430 in December there has been a consistent retreat to test this support. For the most, this support has held (aside from a couple of intraday spikes), but now the market looks set to breakdown. The decisive bear candle yesterday breached the support at 1.0430 and had the lowest close on Aussie/Kiwi since July 2017. However, it is the negative configuration on momentum which is the real concern for the bulls. The RSI is falling below 40 again with downside potential, whilst the MACD lines have formed a “bear kiss” lower and the Stochastics are crossing back lower. The hourly chart shows negative configuration with overhead supply now in the range 1.0430/1.0470 to be used as a chance to sell. Consistent closing below 1.0430 will add conviction to a breakdown and below 1.0395 would open the downside towards a test of the old key 2017 lows of 1.0365 and 1.0320. Rallies now seem to be a chance to sell, with a key lower high at 1.0545.

EUR/USD

The pair has been very choppy over recent sessions. It had looked as though the euro bulls had reacted positively to the breach of $1.1300, but the relative underperformance of the Eurozone economy, coupled with the US inflation upside surprise, drove EUR/USD back for another close below $1.1300 on a huge bear candle. This is a trading range which is now creaking. For months, $1.1300 has tempted the buyers but they now seem to be accepting this new pressure below $1.1300. A test of the key November low at $1.1215 looks imminent. Now, keeping in mind how volatile the swings of the past few sessions have been, the move below $1.1300 has not been confirmed yet, but another session trading below today would increase conviction that this is a market ready to break below $1.1215 and its lowest level since June 2017.

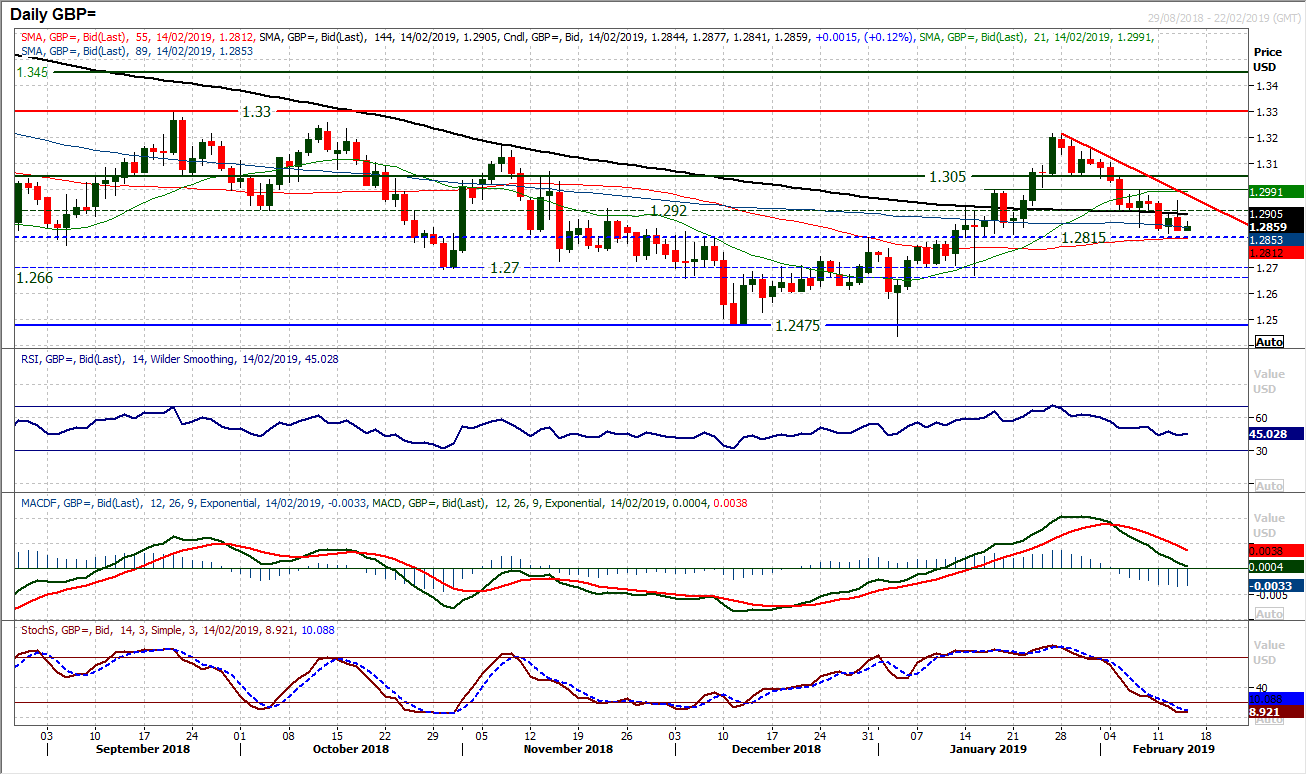

GBP/USD

Cable is still tracking with lower highs as rallies continue to be sold into. The trend lower over the past few weeks is tracking at $1.2980 today and yesterday’s rejection of a rally shows that the dollar strength is a key factor near term. The key level to watch in this is the old breakout support at $1.2815 which also comes with the 55 day moving average support. A closing breach of here would open the downside within the range towards $1.2660/$1.2700 but also put a far more negative configuration to the range again. The momentum indicators have unwound back to neutral points on RSI and MACD but these would turn negative again below 40 on RSI and below neutral on MACD. The Stochastics falling below 20 is a warning. The hourly chart does at least show that the initial support at $1.2830 has held overnight and hourly momentum comes into the European session relatively stable. However, the bull failure at $1.2955 yesterday and continued consideration of the pivot at $1.2920 as resistance will keep the pressure on.

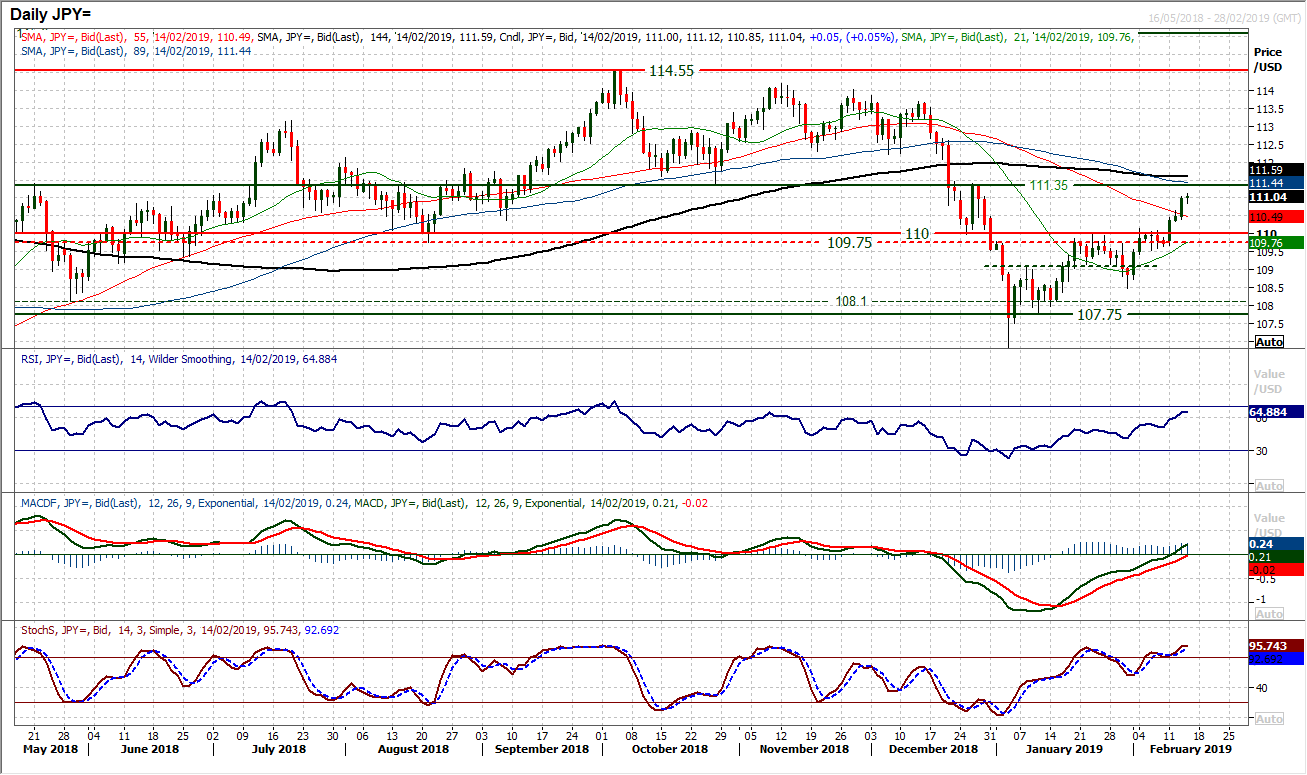

USD/JPY

As the dollar continues to strengthen and risk appetite remains positive there is a continued move higher on Dollar/Yen. Another decisive bull candle yesterday is pulling the market on course for a test of the 111.35 medium term pivot which is the next resistance. Momentum indicators are increasingly positively configures, with the RSI into the mid-60s, MACD lines set to rise above neutral for the first time in ten weeks, and Stochastics strong. Intraday weakness is a chance to buy. The hourly chart shows consistent positive configuration on momentum and a basis of initial support at 110.30/110.60 above the key near to medium term breakout support at 110.00. The pivot at 111.35 is next resistance but a breach would open 112.25 as subsequent resistance.

Gold

It looked yesterday afternoon as though gold was finally positioning for a near term break higher and a resumption of bull control. However, the briefest move above $1316 (a near term pivot) was sold into and the market quickly dropped back into the consolidation of the past week. There is however, still a basis of support in the $1300/$1310 long term pivot and corrections within the 12 week uptrend are a chance to buy. Yesterday’s session turned into a bear candle (in isolation looks like a shooting star candlestick) but coming as part of a consolidation is not a signal to necessarily shift the outlook. Whilst the support at $1302 remains intact the bulls will be confident. However, the legacy of this one day bear candle is that the Stochastics are now swinging lower and the RSI is slipping again. The bulls need to hold the initial rebound higher today, whilst psychologically a move back above $1310 would improve sentiment. The big uptrend comes in to support at $1300 today, adding to the confluence of support building in the pivot band $1300/$1310. The hourly chart shows that $1316 is still a basis of resistance that needs to be overcome to open $1326.

WTI Oil

Another positive session has pulled the buyers back into the driving seat within the trading range of the past five weeks. The more encouraging outlook comes with an improved configuration on RSI (ticking higher above 50 again), MACD lines (steady above neutral) and Stochastics (crossing higher for the first time since the December low). The hourly chart shows there is now a bullish configuration within the $50.40/$55.75 range, with a move that is now finding support above a pivot at $53.00 which is now posting intraday higher lows and higher highs. Moves to unwind the hourly RSI towards 50 and hourly MACD lines consistently above neutral will help to maintain an improving outlook.

Dow Jones Industrial Average

Wall Street continued higher yesterday as the move to multi week highs gathered pace. Leaving the 61.8% Fibonacci retracement behind the Dow is well on its way to the 76.4% Fib level at 25,715. Momentum indicators are set up nicely for the move, with RSI rising in the mid-60s, MACD lines still tracking higher and Stochastics turning up once more. Yesterday’s session was solid, if a little unspectacular and the hourly chart shows there is a little room for an intraday unwind, but corrections remain a chance to buy. The breakout above 24,439 in the past couple of sessions means there is a basis of initial support above the main higher low around the 618% Fib at t 25,333. The key November high at 25,980 is the next major resistance.

Author

Richard Perry

Independent Analyst