Risk negative bias threatens the nascent recovery with jobless claims eyed [Video]

![Risk negative bias threatens the nascent recovery with jobless claims eyed [Video]](https://editorial.fxstreet.com/images/Markets/Equities/DAX/dax-euro-concept-47253534_XtraLarge.jpg)

Market Overview

The US Senate has passed the massive $2 trillion stimulus bill aimed at mitigating the negative economic impact of the Coronavirus. Now the bill will move to the House of Representatives on Friday, with the bill expected to pass fairly comfortably. However, the positive sentiment arising from the US Congress seemingly able to agree on a fiscal package of such enormity, has dissipated overnight. Sentiment is looking more defensive with a negative bias once more today. This will be an important first test of the sustainability of the rebound we have seen in the past couple of sessions. The move back into safety comes ahead of the first big indication of how Coronavirus is impacting on the US economy. US Weekly Jobless Claims are expected to explode higher today, in what is likely to be well above 1.00m. Keeping in mind that at the height of the 2008 financial crisis, jobless claims peaked at 665,000 it could be a massive shock to markets and a wake up call as to just how big this economic shock is. For now though, we see Treasury yields being relatively settled, with volatility on bonds falling. This is beginning to pull a more settled look to major markets (even if they are trading back lower today). US futures are over -1% lower early today but at least the torrent of selling has calmed down. It will be interesting to see if this remains the case after jobless claims today. The UK’s Office of National Statistics is now releasing key UK data before the market opens (at 0700GMT) and so UK Retail Sales posted a mild downside surprise at -0.5% month on month on an ex-autos basis (-0.2% exp). This will not help what is looking to be a risk negative bias early in the European session.

Wall Street closed with gains last night (although off the highs of the session) with the SP 500 +1.1% at 2475. US futures are -1.4% initially today and this has seen a slip back on Asian markets, with the Nikkei -4.5% and Shanghai Composite -0.6%. In Europe, the FTSE futures are -2.2% and DAX futures -2.5%. In forex, there is a mild risk negative bias forming, with JPY and CHF being the standout performers, whilst AUD and NZD are slipping. In commodities, it is interesting to see gold still unable to act as a safe haven, trading -0.8% lower, whilst silver is around -1% down. Oil is around -3% lower.

The Bank of England is in focus on the economic calendar, but US employment will be a massive wake up call for markets. The Bank of England monetary policy decision is at 1200GMT but is not expected to show any further changes to the emergency rate cut back to +0.1% and asset purchases to £645bn. This is expected to be a unanimous decision from the 9 members of the MPC. The final reading of Q4 US GDP is at 1230GMT and is expected to be unrevised from the +2.1% of the Prelim read. This is likely to be the last quarter we see of growth like that for a while! However, it could be that Weekly Jobless Claims get the biggest attention of all today, also at 1230GMT. Jobless claims averaged a shade under 220k for several months before spiking to 281,000 last week. According to Reuters consensus estimates, claims are expected to explode to 1.00m last week. However, given that California alone has regionally announced claims of 1.0m, this could be considerably higher. Just how big the jump is could have a bearing on market sentiment into the US session.

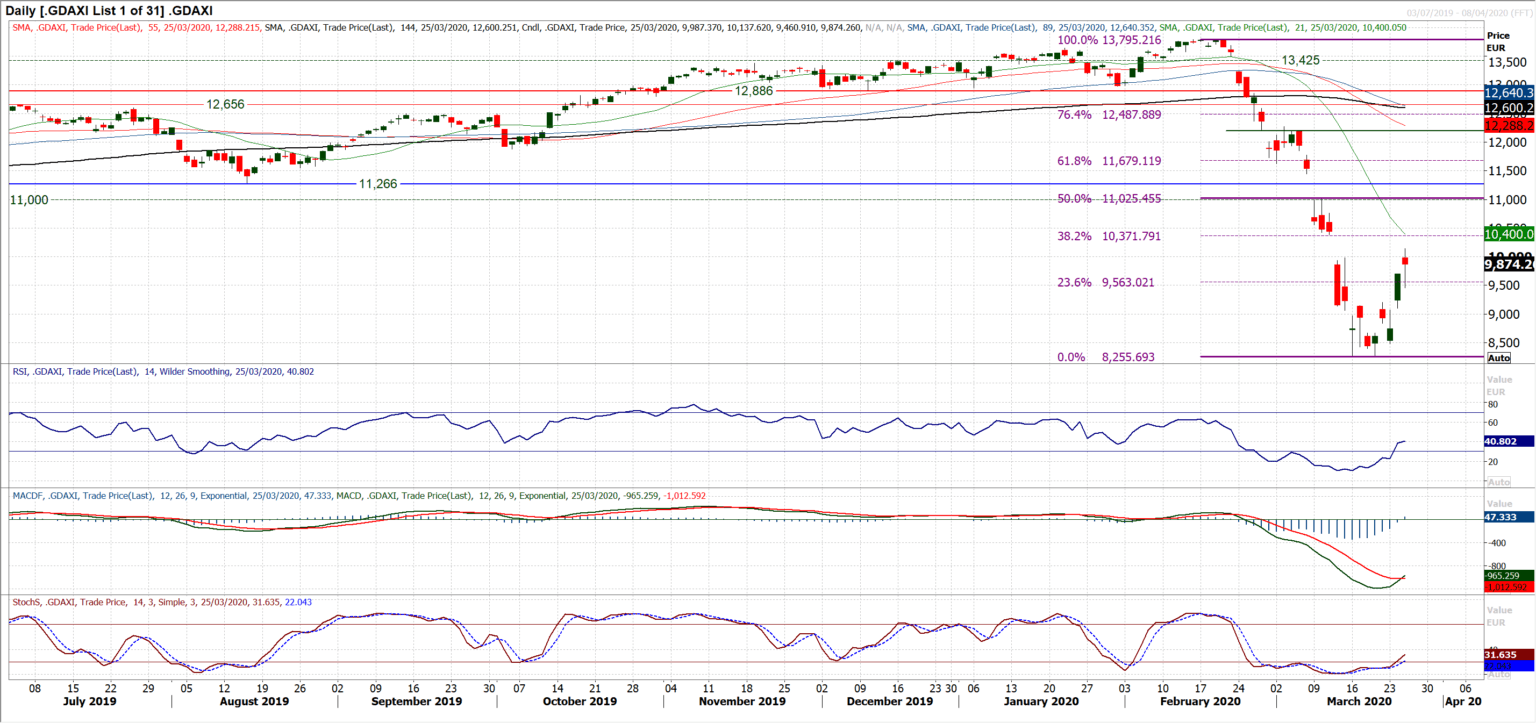

Chart of the Day – German DAX

Equities are on the rebound and many will be asking whether it is a key low that is now in place. Volatility is still massive with wild intraday swings, but there certainly seems to be a recovery forming on the major markets. The DAX is certainly regaining lost ground now and is incredibly now on the verge of officially being in a bull market (which would be great than +20% from the low of 8255). The technicals are improving, with the increased incidence of positive candlesticks (close above the open), even if yesterday’s gain of 174 ticks was slightly less than the opening move. What is encouraging though is that the market is moving higher following the closing of what looks now to have been an “exhaustion” gap, at 9065. The move is also decisively clear of the 23.6% Fibonacci retracement (of the bear market 13,795/8255) at 9563. This opens the 38.2% Fib retracement around 10,370 which also happens to be just around what would be the next gap fill at 10,390. This is therefore the next target of a recovery. Momentum is certainly on a recovery, with Stochastics confirming a bull cross buy signal, along with a bull cross on MACD and RSI rising back above 40. There is clearly plenty of volatility still to play out, but the way this move is shaping, weakness is now being bought into. Even yesterday, the opening bull gap was filled to leave good support 9460/9700 and with futures looking initially lower this morning, this will become an early important gauge. The hourly chart shows neckline support of a base pattern at 9200 with the pattern implying an upside target at 10,150. Hourly RSI holding above 35/40 will maintain the recovery momentum.

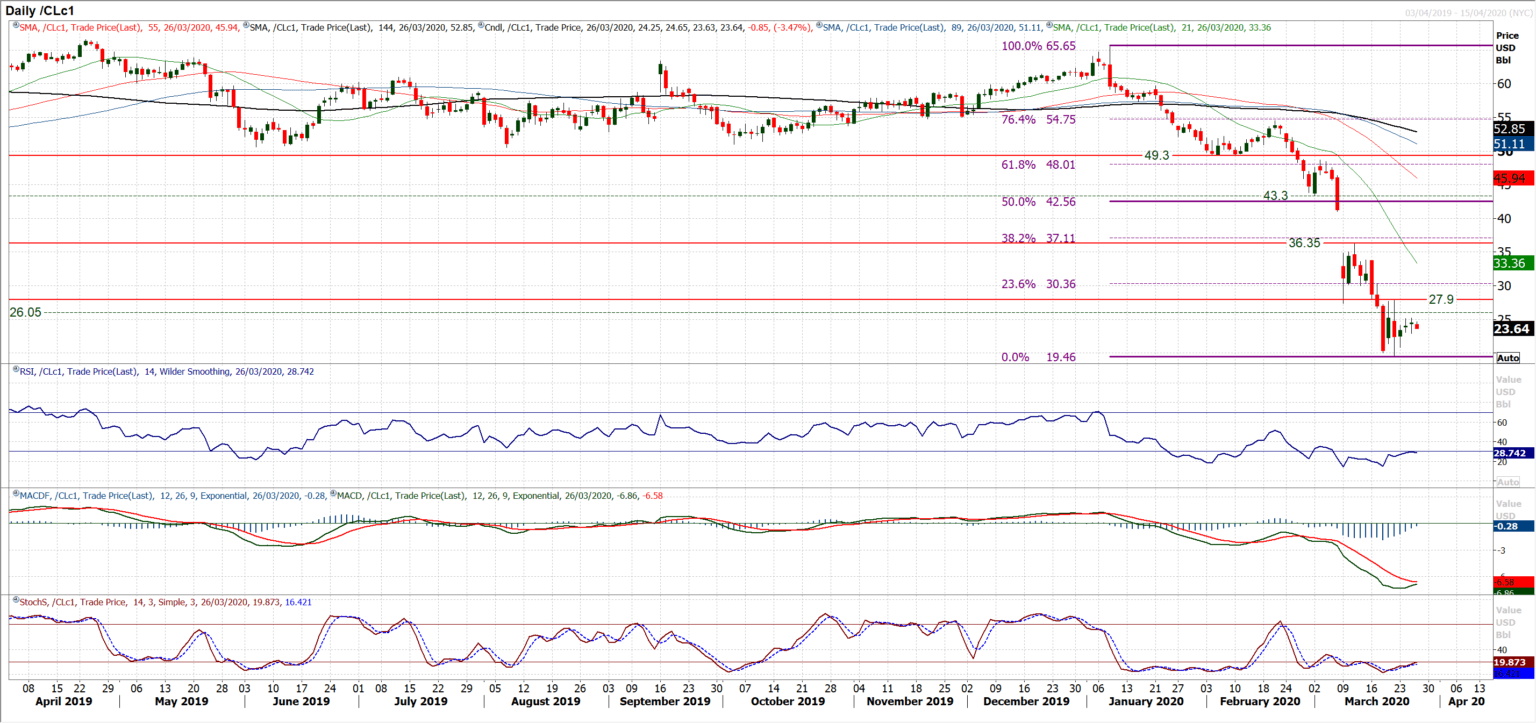

WTI Oil

A rare moment of calm. The first thing to say is that oil has stemmed the flow of huge selling pressure. A pick up from $19.45 in the past few sessions has settled the nerves that we might be looking at single digit oil. However, even with three positive closes in a row now, the prospect of recovery is not seemingly going to be “v” shaped. The past few sessions have seen a consolidation develop. This is shown with the reduced daily trading ranges and small candlestick bodies. Hourly technical indicators are moderating, with the hourly RSI between 40/60 for the past few days, hourly MACD settling around neutral and hourly moving averages all converging to flatten together. The rebound has begun to struggle under $25.25 resistance and the bull dream of a breakout above $27.90 to complete a base pattern still seem a long way off. Support around $23.10 needs to hold today to maintain any sense of recovery momentum, whilst the higher low at £21.80 is key to preventing a retest of the $19.45 low.

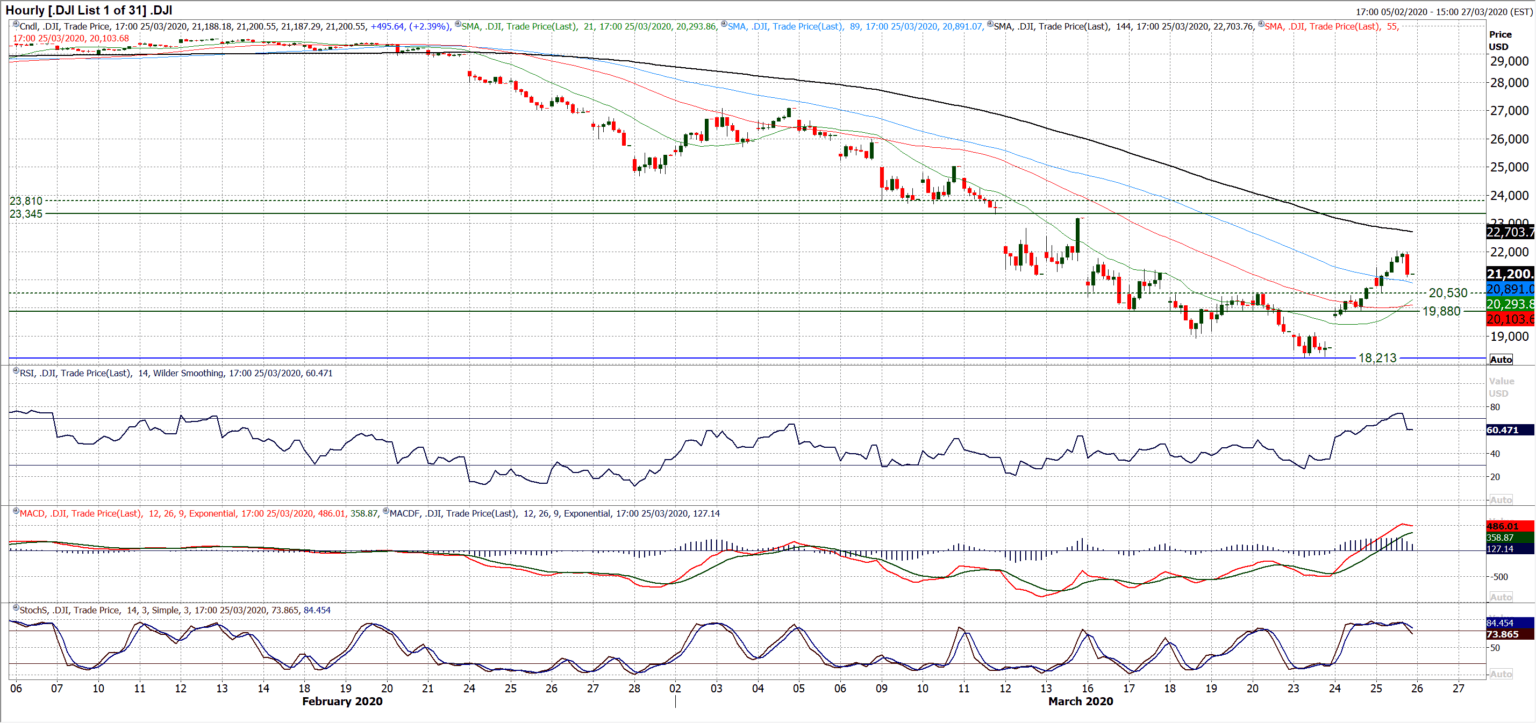

Dow Jones Industrial Average

A second day of gains for the Dow. This is the first time of this happening since the massive sell-off began in mid-February. There will be talk of a sustainable recovery now and perhaps even “the low” having been formed. It is still way too early to say that and how the market responds to the next negative shock/session will be an important gauge. For the Dow, we spoke recently about a breakout above 20,530 which had been a high left on Friday before the culmination sell-off kicked in. It was good to see this 20,530 breakout being used as aa basis of support yesterday. It now means that there is initial support 20,530/20,735. With futures ticking back lower this morning, how this support band reacts will be interesting. Closing back under 20,530 would also be a decisive close back under the 23.6% Fibonacci retracement (of the massive 29,568/18,213 sell-off) at 20,893. It would suggest the bulls losing confidence in the recovery. The hourly chart shows good recovery momentum having built up, so the hourly RSI holding above 40 along with hourly MACD above neutral would be encouraging. A move back under 19,880 would effectively confirm an aborted recovery.

Other assets insights

EUR/USD Analysis: read now

GBP/USD Analysis: read now

USD/JPY Analysis: read now

GOLD Analysis: read now

Author

Richard Perry

Independent Analyst