Risk aversion raises its ugly head

Outlook:

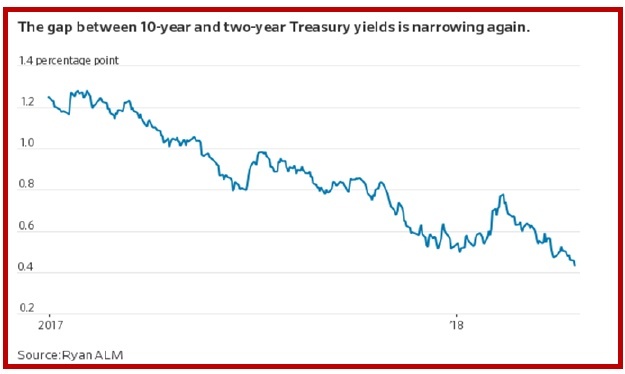

Today we get the usual Thursday jobless claims and three Fed speakers. But we are getting mixed and contradictory signals from various markets. Everybody and his brother is mightily confused. The WSJ notes (again) that the yield curve is at the flattest in more than a decade. Nobody really knows what it means, but one implication is that the bond gang doesn’t see infla-tion lurking in the bushes and doesn’t see a tax-cut driven investment boom, either.

As noted above, market players are ostriches with their heads in the sand. It’s naïve and ridiculous to see valid reasons for risk appetite to be on the comeback trail. The drawbacks are plentiful. N. Korea has broken every promise and even if Trump gets new promises, they can’t be relied upon. Trade rheto-ric has been absent for a few days, but to imagine the issue has gone away is just plain dumb. The Summit of the Americas was a total dud and while Nafta talks resume today, the outlook is not at all favora-ble.

Trump needs a constant supply of grievances with which to distract attention from the special prosecu-tor and now the legal hoopla in the New York courts over hush money to Trump’s dalliance ladies. Heaven only knows what distraction he will throw up next, but we can pretty much guarantee there will be a new distraction, and then another and another. Trump has narcissistic personality disorder. He is such an incompetent manager he took four of his businesses into bankruptcy. He lies. He is erratic, im-pulsive, and refuses to be taught critical background information and, you know, facts. What makes anyone think he can negotiate peace in Korea after 65 years of stalemate?

As for protecting the interests of the investing class, bah. Beyond a tax break for himself and his cro-nies, Trump knows nothing about stock and bond markets. He has never invested in equities. He wouldn’t know a P/E if it jumped up and bit him on the nose. Trump thinks stock market gains are like TV ratings, a vote on his performance. And here is the only ray of light—market players are willing to turn a blind eye to Washington shenanigans. Stupid, uninformed tweets about this company or that company, as we wrote about yesterday, are fleeting factors. Trump knows de-regulation is a good thing for his cronies because they told him so, and doesn’t care if they profit personally—but there is no grand plan to return to some pipedream of Adam Smith’s unfettered capitalism.

Here’s why Trump’s ignorance counts—if we were to get another financial crisis anywhere close to what we saw in 2008, what would be Trump’s response? He would not have one of his own because he has no beliefs or any coherent set of concepts about how the economy and financial markets work or should work. That means he would rely upon Kudlow, Ross, Mnuchin and others in his immediate cir-cle, and those guys do have an ideology—open it all up so the fat-cats can gorge. The comparison that comes immediately to mind is Pres Hoover, who said “let them all fail.” Hoover also favored the disas-trous Smoot-Hawley tariffs, bank expropriation of farmland, and many other policies that prolonged the Great Depression.

This is not to say government “should” step in a la TARP and the other programs that came hot on the heels of the 2008 crisis. That’s not the argument we should be having. Libertarians think the money, if any, should have gone to individuals, not to institutions… But to have an Administration with no plan at all, and a likely response of “let them all fail” in the event of another crisis, should frighten everyone. Trump and cronies literally care nothing about the average Joe. They care only about maintaining and increasing their personal wealth. When crisis hits an oligarchy, history teaches us what happens to the average Joe. He starves.

To change gears, yesterday we fulminated about the possibility of oil prices driving inflation through the expectations effect. And to be sure, Brent is now only 50¢ off the 52-week high. There’s another fundamental change starting to appear in the metals markets. Check out kitcometals.com. You can de-tect a bottoming in copper, aluminum, lead, nickel and zinc. Stocks are well drawn-down in everything except aluminum, where supply has accumulated. Bloomberg’s chart of industrial metals shows a wild rally. This is nice for producing countries like Australia and Canada, and not so hot for industrial coun-tries that use metals for inputs, which includes Germany, the US and of course, China.

Bloomberg reports today “The turmoil in metal markets unleashed by U.S. sanctions on Oleg Deri-paska’s United Co. Rusal has spread far beyond the aluminum price. While the latter has rallied more than 30 percent since the start of this month, concern over further actions from U.S. officials has seen nickel surge to a three-year high in recent days, helping to push Bloomberg’s commodity index to the highest level since 2015. Rusal, meanwhile, is in discussions with the Chinese on a deal that would al-low it to buy and sell aluminum in the Asian country as it seeks to mitigate the fallout from sanctions, according to people familiar with the talks.”

Good grief! Trump has caused a rapprochement between Russia and China!

The WSJ selects from the otherwise tedious Fed minutes that regional Feds are starting to get freaked out by metals prices. “Fed officials are getting an earful from companies in their districts about trade policy and its fallout—both good and bad. Businesses across the U.S. reported rising metal prices in recent weeks due to recent steel and aluminum tariffs, according to a Fed report on business conditions. Prices generally increased at a moderate pace, through there were also some more dramatic moves… “ For example, the St. Louis district reports “Some steel and aluminum manufacturers announced plans to reopen facilities and call back workers.”

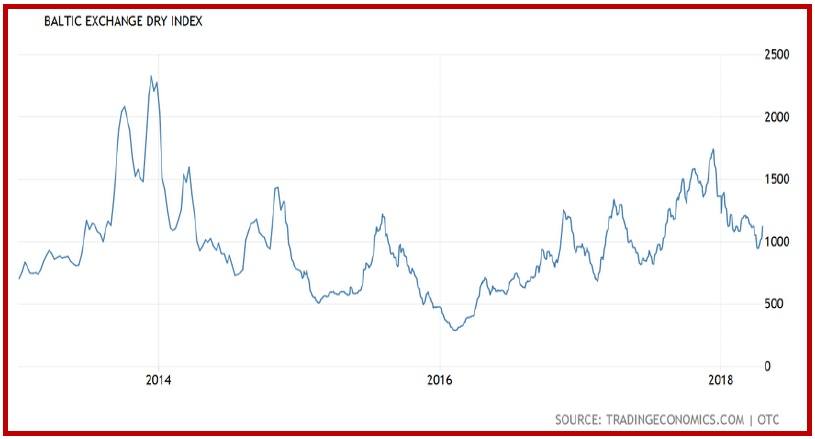

Metals may be aberrant moves quickly altered, but metals are not like financial assets—they take years and years to discover and set up production, as self-styled “investment biker” Jim Rogers wrote about so many time. They also cost a fortune to transport and the logistics are horrible. That is going to make interpreting the Baltic Dry Index harder than ever. The Baltic Dry is a general (very general) indicator of the health of the global economy. It measures the volume and price of shipping goods internationally in one indicator. We had to remove our version of it because of trouble with our Reuters data feed (and if you think talking to the IRS is hard, try talking to Reuters).

The version here is from tradingeconomics.com. The Baltic Dry was falling hard off the peak last De-cember and has only just started to turn around. This may show that just as Trump was taking office, the global economy was already slowing down, something nobody commented on at the time. Weirdly, the Shanghai stock index chart looks correlated with the Baltic Dry, too, but that’s an eyeball compari-son over just a few months, not a statistical deduction. See the Shanghai in the Chart Package.

What does it mean, if anything? First, the Trump tax cuts have a lot of heavy lifting to rescue the global economy from a slowdown, something that is not really likely. Second, if there is a crisis looming in rare materials, whether oil or metals or both, nobody is in charge. China may be stockpiling but we never heard of any other country holding reserves of (say) iron, as we have a Strategic Petroleum Re-serve. This is not to say a crisis is definitely coming. But it is to say the supply chain disruptions started by the financial crisis of 2008 and China’s massive rise over the same last decade have not yet peaked, let alone been resolved. Gee, there must be an ETF for industrial metals.

As before, whenever we expect disruptions of any importance, risk aversion raises its ugly head, and risk aversion generally leads to favoring the dollar even if the disruption itself is a negative for the US economy. We wish we could away from this inference but it keeps returning like the bad penny.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes. To see the full report and the traders’ advisories, sign up for a free trial now!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat