Risk aversion grows as Trump discusses increasing tariffs again [Video]

![Risk aversion grows as Trump discusses increasing tariffs again [Video]](https://editorial.fxstreet.com/images/Macroeconomics/Countries/America/UnitedStatesofAmerica/Trump1_XtraLarge.jpg)

Market Overview

Risk appetite has taken a hit as President Trump has discussed the prospect of raising tariffs further on China if there is no agreement reached on “phase one”. This could still be part of his carrot and stick approach to negotiation, but it is spooking markets which had been positioning towards the two countries coming towards a deal. Treasury yields are falling, whilst the yen is taking renewed strength and gold is also edging higher. Watching the Dollar/Yuan rate pulling back higher again decisively higher from 7.00 again shows the concern is growing. Equity markets are also starting to feel the pinch of some profit-taking after some strong runs higher in recent days/weeks. The reaction to these moves will be very interesting now. If there is a containment to the flow into safe havens, then it would suggest that once the initial knee jerk response is factored in, there would still be an expectation that the US and China will be working to a deal. Aside from this, tonight we get the FOMC minutes. It will be interesting to see how cautious (or not) the Fed was at a meeting of a -25bps rate cut. The market seems fairly set in its assessment that the Fed is now on hold for the foreseeable future.

Wall Street closed lower with the SP 500 -0.1% at 3120 whilst US futures are another -0.2% back today. Asian markets have been broadly corrective today with the Nikkei -0.8% and Shanghai Composite -0.7%. In Europe there is a less corrective but still cautiously negative open, with FTSE futures -0.1% and DAX futures -0.4%. In forex, there is a mild risk negative and dollar positive theme, with JPY, USD and CHF all performing well. In commodities, the mild drift higher on gold continues, whilst there is little sign of any rebound on oil after the selling pressure of the past couple of days.

It is another quiet European morning on the economic calendar, and in fact, it pretty much stretches into the US session too. Very light data with just Canadian inflation at 1330GMT which is expected to remain at +1.9% in October (+1.9% in September). The EIA oil inventories are expected to show crude stocks building by +1.1m barrels (+2.2m barrels last week), whilst distillates are expected to drawdown by -0.5m barrels (-2.4m barrels) and gasoline stocks to build by +0.7m barrels (+1.8m barrels last week). The key announcement of the day is with the FOMC minutes for the meeting on 30th October. There is a widespread expectation of the Fed now being on hold for now for some time to come, so any hawkish or more likely dovish deviation in message from the minutes could be market moving.

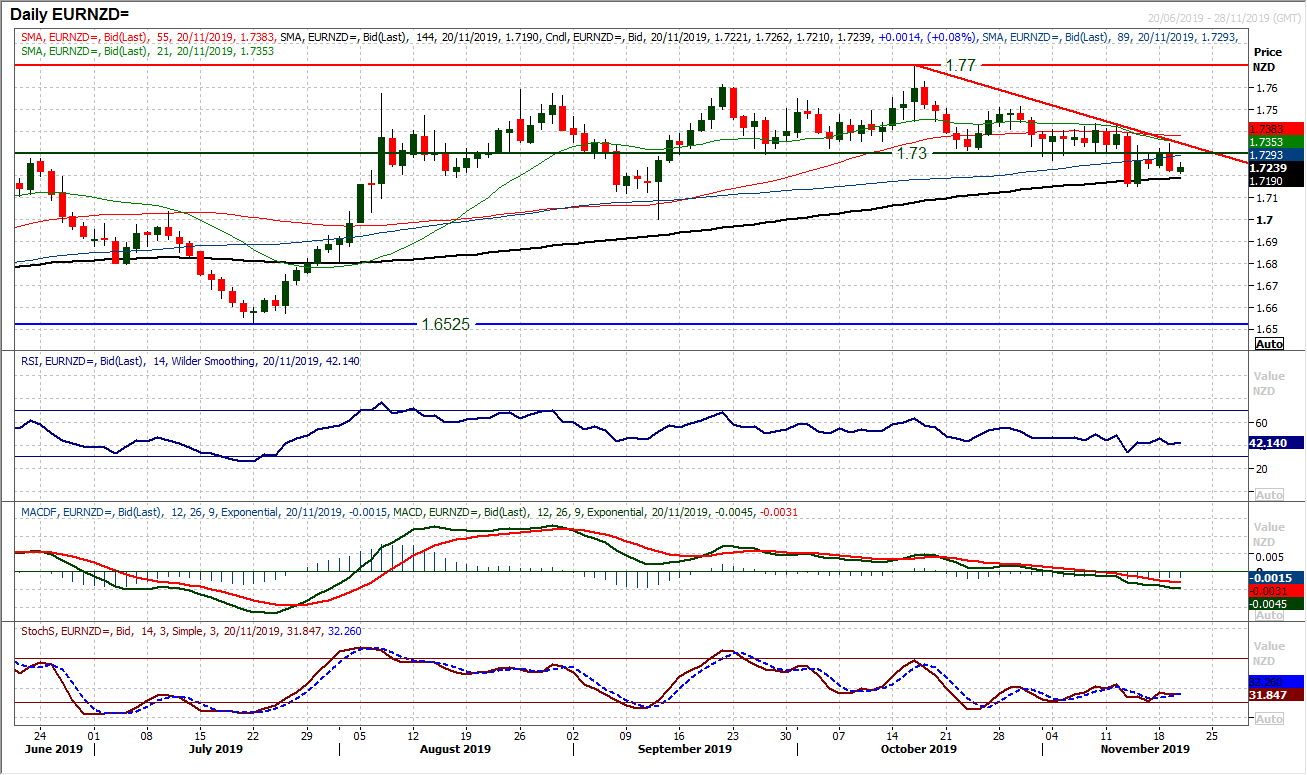

Chart of the Day – EUR/NZD

We have seen the euro relative performance through major cross pairs suffering in recent weeks. With the RBNZ holding back from an expected cut the Kiwi has strengthened in a move that has broken EUR/NZD below the old pivot band support at 1.7300. With yesterday’s session forming a bearish engulfing candlestick, this looks to be a renewed sell signal. Forming a one month downtrend, following the breakdown, the now falling 21 day ma (around 1.7350) is a basis of resistance. The old support at 1.3700 is also a basis of resistance in recent days. With momentum indicators taking on an increasingly corrective configuration, rallies into the resistance area 1.7300/1.7350 are a chance to sell. The RSI continues to fall over at lower levels, whilst the MACD lines are falling at three and a half month lows. We see pressure for a retest of the recent low at 1.7150 whilst the September low at 1.7000 is also back within range. The bulls would need a close above resistance at 1.7435 to regain positive momentum.

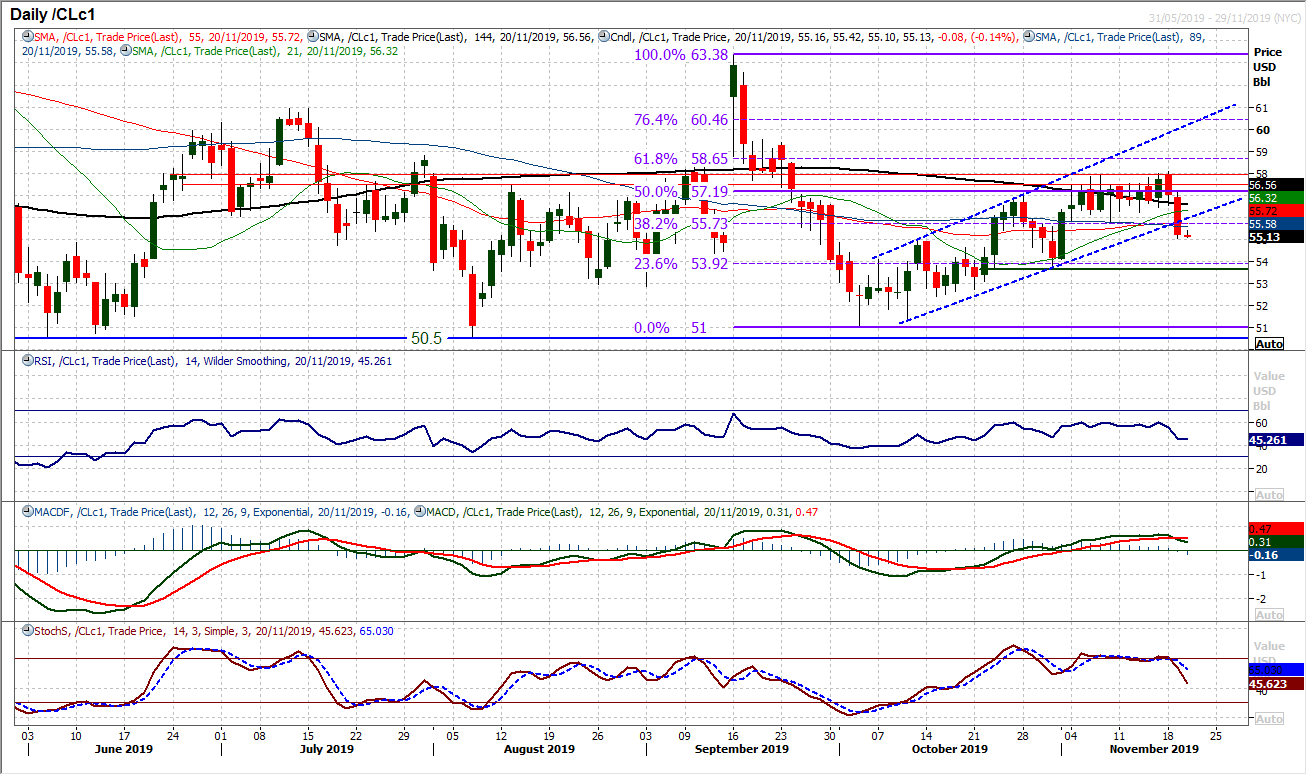

WTI Oil

Has the outlook on oil changed again? A suggestion that Russia would not agree to further OPEC production cuts has driven the price of oil lower. A second decisive negative candle has not only broken the uptrend channel of the past five weeks, but also the support at $55.75. It comes also with sell signals on momentum, with a MACD bear cross and Stochastics also crossing lower. The reaction today will be key. If the old support band $55.75/$56.20 now becomes a basis of resistance, then this could quickly turn into a sustaining move to test the support of the key higher low at $53.70. The RSI moving below 40 would also be a corrective signal.

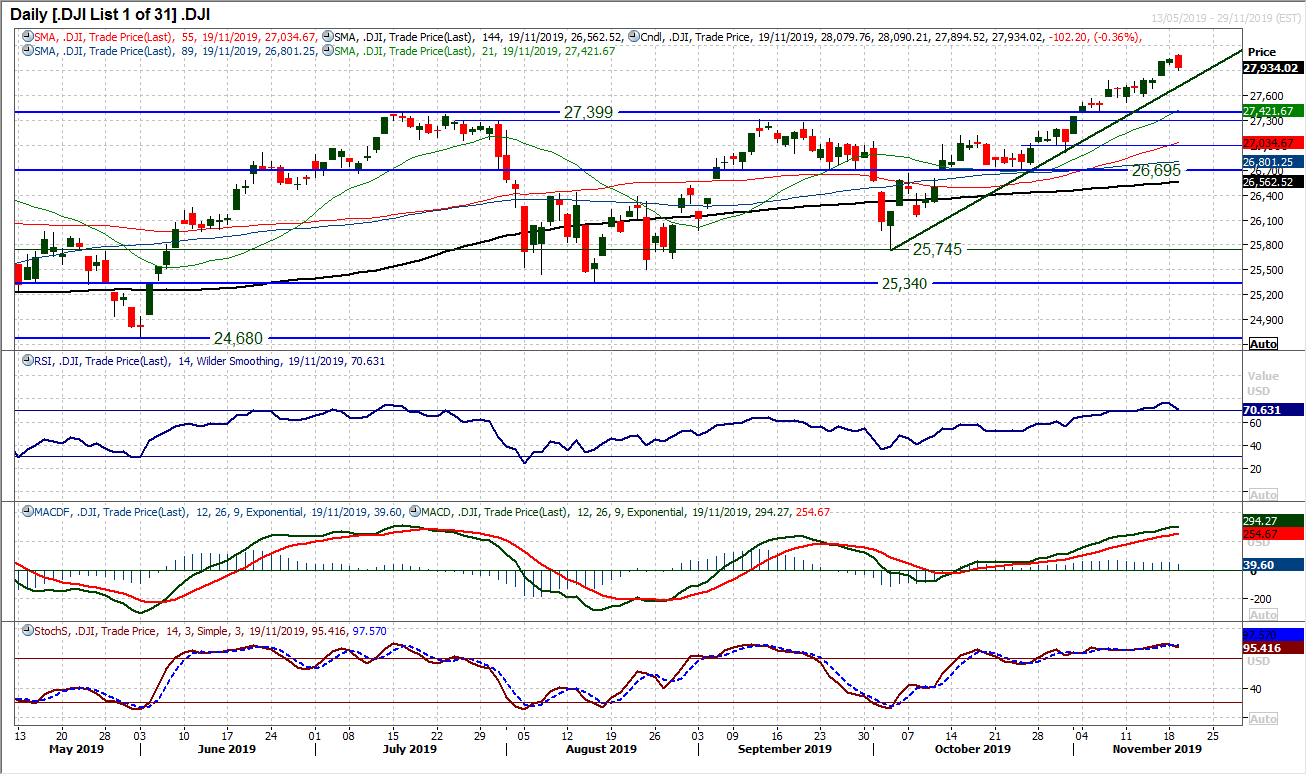

Dow Jones Industrial Average

After the first really negative candlestick on the Dow for more than a few weeks, market reaction will be key. Yesterday’s bearish engulfing candle (bear key one day reversal) is an exhaustion candle. We discussed previously that the trend higher (which comes in at 27,765 today) was pretty relentless, however there has not been two consecutive negative closes in around six weeks. That makes the reaction today important, as a second negative candle today could suggest a corrective phase starting to develop. Previous closes lower have been met with near immediate buying pressure again. We noted yesterday that the initial support was 27,775/27,800. Momentum has slipped mildly (RSI back towards 70) but no sell signals yet. Resistance is now key at yesterday’s high of 28,090. We are still buyers into support within the uptrend, however, we were cautious bulls yesterday and even more so today.

Other assets insights

EUR/USD Analysis: read now

GBP/USD Analysis: read now

USDJPY Analysis: read now

GOLD Analysis: read now

Author

Richard Perry

Independent Analyst