Risk appetite diminishes

Forex News and Events

Risk appetite and oil (by Peter Rosenstreich)

While the favorable conditions for further risk taking remain intact, financial markets have become more prudish with positioning. High-yielding assets, including EM and equity markets have generally slowed or paused further appreciation, while risk gauges such as oil and gold have fallen. Liquidity has tightened as risk seeking traders feel crowded and overvalued. It’s easy enough to play the Monday morning quarterback with no skin in the game. With expectations that Fed Chair Yellen will not provide a signal for a hike in September or additional clarity on the directional slope of interest rates, we anticipate that risk-appetite will return in the short term.

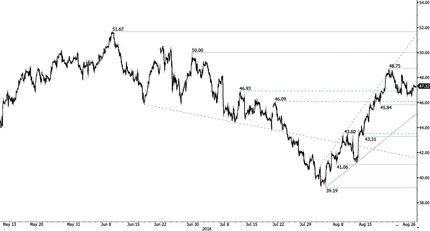

Yet, within the risky universe it’s unlikely that the oil price slide will stop. Saudi Arabian oil minister, Khalid al-Falih has stated that there has so far been no substantial discussion on any OPEC action to lower production. This news reversed yesterday’s price bounce based on reports that Iran would join an unofficial OPEC meeting in Algeria in September. Expectations that major oil producers will find an agreement to halt the supply glut have declined significantly. In addition, demand is unlikely to pick up past currently subdued forecasts, particularity in India and China (marginal improvement in demand could occur in core-Europe as Brexit fears prove unfounded). WTI traders should target $45 support defined by the 21d MA. In FX, oil-linked currencies such as NOK and CAD should continue to underperform as the weight of falling crude prices outweighs the improvement in risk appetite.

Yellen puts markets on hold (by Yann Quelenn)

Not much volatility is expected today on the financial markets before Fed Chair Janet Yellen’s speech at Jackson Hole. The odds that Yellen will give a hawkish signal for a September rate hike have increased and are now at pre-Brexit levels around 32%. It is clear that, once again Yellen will point out the better employment report, despite mixed and very volatile NFPs over the past few months.

Equity markets are also sidelined, as the S&P 500 closed in negative territory for the second day in a row. Yet, bearish moves were very light, indicating that markets refuse to go lower and now expect a dovish signal from the Fed, to pursue their path to new record-highs. We clearly believe that there is strong likelihood that this will happen. The bonds markets are also impatient for Yellen’s address as, for example, the generic 10-year US Government Bond yield has increased again over the last months and is now not far from 1.6%.

Currency-wise, the dollar should remain strong as long as there are still hopes about a rate hike this year. The Fed’s credibility is clearly at stake and we believe that a small increase in interest rates is possible if only for the sake of saving its integrity. Repeating over and over that a rate hike will happen and not doing anything is strongly damaging. In the event of dovish signals, the dollar may have further downside potential and this would also weigh on US yields. We are definitely not in a period of rate normalisation but rather in a fight for credibility.

Crude Oil - Setting Lower Highs.

| Today's Key Issues | Country/GMT |

| Jul Retail Sales YoY, last 6,00% | EUR/07:00 |

| Jul Retail Sales SA YoY, exp 4,30%, last 5,60% | EUR/07:00 |

| Jul M3 Money Supply YoY, exp 5,00%, last 5,00% | EUR/08:00 |

| Aug 19 Money Supply Narrow Def, last 8.72t | RUB/08:00 |

| 2Q Manufacturing Wage Index QoQ, last 0,70% | NOK/08:00 |

| Aug 23 FIPE CPI - Weekly, exp 0,02%, last 0,05% | BRL/08:00 |

| Riksbank I/L Bond Purchase Results | SEK/08:10 |

| 2Q P GDP QoQ, exp 0,60%, last 0,60% | GBP/08:30 |

| 2Q P GDP YoY, exp 2,20%, last 2,20% | GBP/08:30 |

| 2Q P Private Consumption QoQ, exp 0,80%, last 0,70% | GBP/08:30 |

| 2Q P Government Spending QoQ, exp 0,30%, last 0,50% | GBP/08:30 |

| 2Q P Gross Fixed Capital Formation QoQ, exp 0,40%, last -0,10% | GBP/08:30 |

| 2Q P Exports QoQ, exp 0,70%, last -0,40% | GBP/08:30 |

| 2Q P Imports QoQ, exp 0,80%, last 0,10% | GBP/08:30 |

| Jun Index of Services MoM, exp 0,10%, last -0,10% | GBP/08:30 |

| Jun Index of Services 3M/3M, exp 0,40%, last 0,30% | GBP/08:30 |

| 2Q P Total Business Investment QoQ, exp -0,90%, last -0,60% | GBP/08:30 |

| 2Q P Total Business Investment YoY, last -0,80% | GBP/08:30 |

| Aug FGV Construction Costs MoM, exp 0,26%, last 1,09% | BRL/11:00 |

| Jul Advance Goods Trade Balance, exp -$63.0b, last -$63.3b, rev -$64.5b | USD/12:30 |

| Jul P Wholesale Inventories MoM, exp 0,10%, last 0,30% | USD/12:30 |

| 2Q S GDP Annualized QoQ, exp 1,10%, last 1,20% | USD/12:30 |

| 2Q S Personal Consumption, exp 4,20%, last 4,20% | USD/12:30 |

| 2Q S GDP Price Index, exp 2,20%, last 2,20% | USD/12:30 |

| 2Q S Core PCE QoQ, exp 1,70%, last 1,70% | USD/12:30 |

| Fed Chair Yellen to Speak at Jackson Hole Policy Symposium | USD/14:00 |

| Aug F U. of Mich. Sentiment, exp 90,8, last 90,4 | USD/14:00 |

| Aug F U. of Mich. Current Conditions, last 106,1 | USD/14:00 |

| Aug F U. of Mich. Expectations, last 80,3 | USD/14:00 |

| Aug F U. of Mich. 1 Yr Inflation, last 2,50% | USD/14:00 |

| Aug F U. of Mich. 5-10 Yr Inflation, last 2,60% | USD/14:00 |

| BOE's Shafik Speaks at Jackson Hole | GBP/14:50 |

| Jul Federal Debt Total, last 2959b | BRL/22:00 |

| Jul Eight Infrastructure Industries, last 5,20% | INR/22:00 |

| SURVEY: Private Capital Expenditure 2016-17 A$97b | AUD/22:00 |

The Risk Today

Yann Quelenn

EUR/USD is well into a bullish momentum. Uptprend remains strong. Key resistance is given at 1.1352 (23/08/2016 high) then 1.1428 (23/06/2016 high). Hourly support can be found at 1.1245 (24/05/2016 low). Expected to increase again. In the longer term, the technical structure favours a very long-term bearish bias as long as resistance at 1.1714 (24/08/2015 high) holds. The pair is trading in range since the start of 2015. Strong support is given at 1.0458 (16/03/2015 low). However, the current technical structure since last December implies a gradual increase.

GBP/USD's buying interest is growing even if the pair fails to go above former resistance implied by the top of channel. For the time being, the medium-term bearish momentum is lively. Hourly resistance can be found at 1.3372 (03/08/2016 high). Hourly support can be found at 1.3024 (19/08/2016 low). The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY is trading above the 100-mark without much volatility. The technical structure suggests that the pair is consolidating before a further head lower. Strong support is given at 99.02 (24/06/2016 low). Hourly resistance is given at 102.83 (02/08/2016 high). Selling pressures should continue. We favour a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

USD/CHF is trading around former resistance at 0.9659 (09/08/2016 high) after a pickup in short-term buying interest. Hourly support given at 0.9522 (23/06/2016 low) is on target. The road is wide-open for further strengthening. In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

| EURUSD | GBPUSD | USDCHF | USDJPY |

| 1.1616 | 1.3981 | 1.0093 | 109.14 |

| 1.1479 | 1.3534 | 0.9956 | 107.9 |

| 1.1428 | 1.3372 | 0.9775 | 102.83 |

| 1.1291 | 1.3225 | 0.9654 | 100.47 |

| 1.1046 | 1.2851 | 0.9522 | 99.02 |

| 1.0913 | 1.2798 | 0.9444 | 96.57 |

| 1.0822 | 1.188 | 0.9259 | 93.79 |

Author

Peter A Rosenstreich

Swissquote Bank Ltd

Peter Rosenstreich is Swissquote Bank’s Head of Market Strategy and manages the global strategy desk; he has held various positions in several banking institutions in the United States, Europe & Asia.