Revisionist mystery: Buckle up for a blowout in Q1 PCE

Summary

A revision to January lifted real spending enough to put PCE on track for an annualized growth rate of 4.5% in Q1. But a slowing in February may be more emblematic of the current state of the consumer. Meanwhile, PCE inflation is still hot enough to warrant another rate hike in May.

January's gain sets the stage for Q1 PCE

The latest data on personal income and spending reflect the crosscurrents presently influencing the consumer and reveal the difficulty faced by everyone from policymakers to businesses as both struggle to divine how long consumers' staying power will last amid rate hikes and tighter credit.

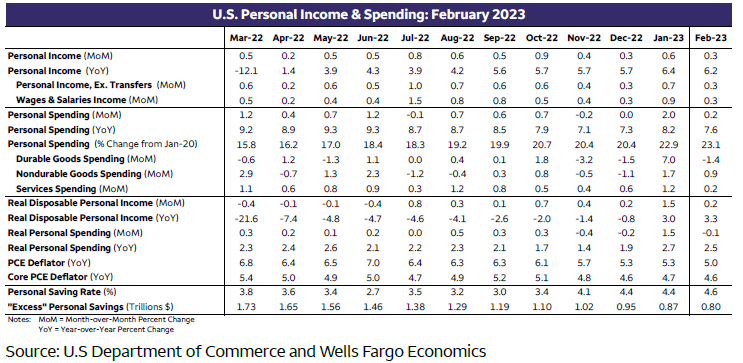

Real personal consumer spending has now contracted in three out of the past four months and yet today's report will likely have many forecasters penciling in even stronger Q1 PCE growth. Why? Mostly because January's initially reported 1.1% increase in real spending was revised higher to a gain of 1.5%. That is an absurdly large monthly increase (chart). The pandemic shutdowns and stimulus checks injected some major volatility into the monthly changes in spending in recent years, but consider this: a 1.5% monthly increase in real spending is almost twice as strong as any monthly gain reported throughout the prior expansion between 2009-2020. If real spending is flat in March, real PCE would rise at an annualized pace of 4.5% in the first quarter.

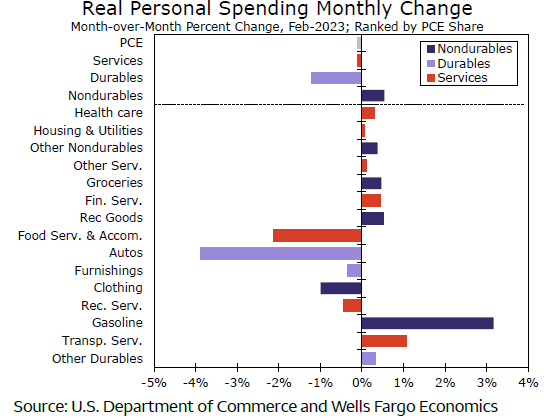

So yes, in February we lost some spending momentum as real spending posted a scant 0.1% decline after the surge in January. Had it not been for a 3.9% real drop in the notoriously volatile motor vehicle category, real spending would have been positive (chart). In short, after a curiously strong January, the consumer is evidently losing momentum.

It bears noting that real services spending did notch its first monthly decline in 13 months, but the giveback in February was less than a sixth of January's gain. We may have some concerns about goods spending, but we are not concerned this is the beginning of a broader services retrenchment.

Author

Wells Fargo Research Team

Wells Fargo