Reserve Bank of Australia Preview: To pause or not to pause

- The Reserve Bank of Australia is expected to stay on hold, however, a 25 bps rate hike is possible.

- Inflation slowed down in February, still above target.

- AUD/USD stabilizing, offering mixed signs.

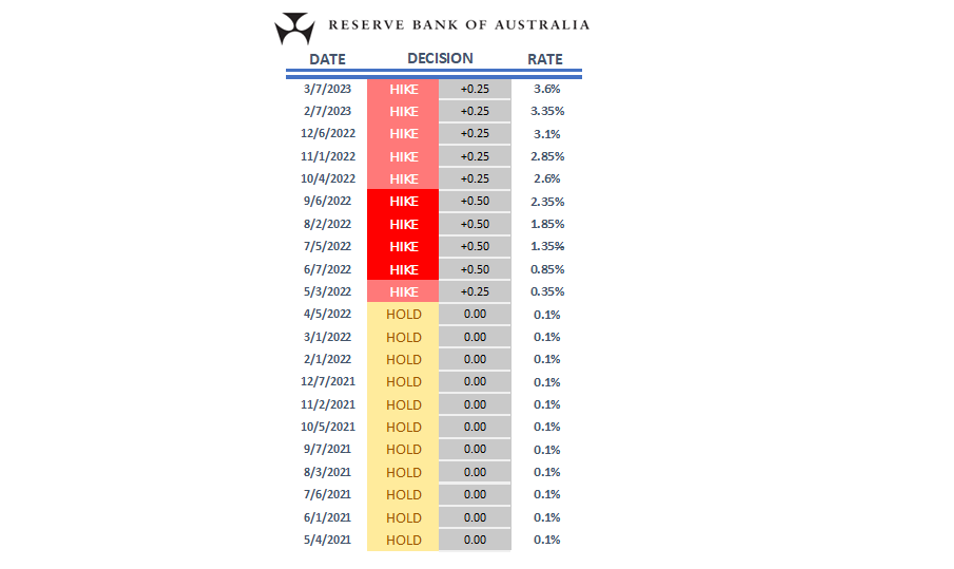

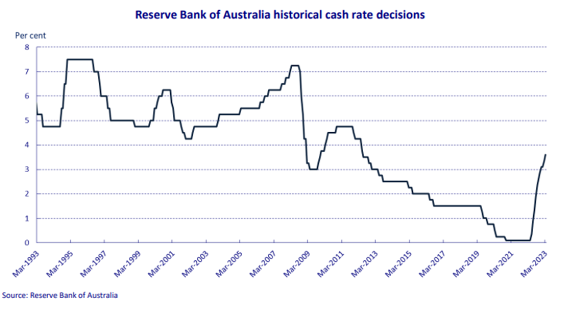

The Reserve Bank of Australia (RBA) will announce its monetary policy decision on April 4. The RBA has been raising the Cash Rate Target since March 2022 and, during the last five meetings, opted for 25 bps hikes. Back in February 2022, the rate was 0.1% and now stands at 3.6%.

On March 7, the RBA raised as expected and the Aussie dropped across the board. Governor Philip Lowe said, “the Board expects that further tightening of monetary policy will be needed to ensure that inflation returns to target and that this period of high inflation is only temporary,” and added that “in assessing when and how much further interest rates need to increase, the Board will be paying close attention to developments in the global economy, trends in household spending and the outlook for inflation and the labour market.”

According to the minutes of the meeting, Board members observed that inflation remained too high, the labor market was very tight and wage growth had picked up. Clearly, the RBA did not suggest the tightening cycle was over. As other central banks around the world, the RBA decisions are data-dependent. The day after the meeting Lowe said the central bank was closer to pausing rate hikes; also banking news started flooding headlines. The banking crisis appears to be contained for the moment, but added uncertainty to the global economic outlook.

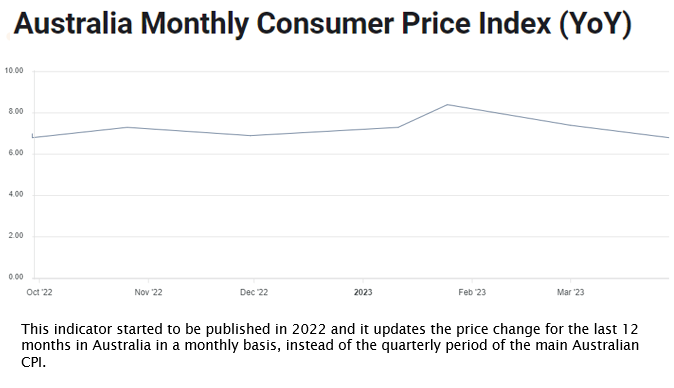

The latest Australian economic numbers offered arguments for a hike and also for a pause. The economy added 64,600 payrolls in February and the Unemployment Rate dropped from 3.7% to 3.5%. Retail Sales rose by 0.2% in February, in line with expectations. Sales have been around the same levels since November 22, a warning sign about consumer spending and an argument for a pause for the RBA. The Monthly Consumer Price Index (CPI) came in below expectations. The annual rate dropped to 6.8% in February from 7.4% in January. This marked the second decline in a row, but still above the 2-3% target range.

Many banks and analysts adjusted their forecasts for the RBA after the CPI data, from a 25 bps rate hike to no change, not only because of the lower inflation but also considering the impact of the banking turmoil.

A pause is coming at the RBA; however, April could not be the time. The European Central Bank and the Federal Reserve pushed with hikes despite recent developments. Inflation remains elevated and the labor market is tight. Nevertheless, it is worth adding that the economic outlook has worsened. All in all, there is still room for more rate hikes, while at the same time, a pause also seems prudent considering the inflation trend and the uncertainty.

AUD/USD sideways, undecided like market forecasters

Considering the current environment, with doubts about the future of the economy, the impact of the RBA could be short-lived, particularly if it proceeds without major surprises. What could impact the most is how officials see the economy and their outlook. The AUD/USD should benefit from an upbeat perspective. On the contrary, a cautious central bank opting to stay on hold and pointing out that it could stay that way for a while should be (very) negative for the Aussie.

The AUD/USD is moving sideways near 0.6700. The daily chart shows the 200-period Simple Moving Average waiting at 0.6770. A break higher should point to further gains over the medium term while, on the contrary, below 0.6630, to more losses to test March lows at 0.6560.

-638158836567386201.png)

AUD/USD daily chart

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Matías Salord

FXStreet

Matías started in financial markets in 2008, after graduating in Economics. He was trained in chart analysis and then became an educator. He also studied Journalism. He started writing analyses for specialized websites before joining FXStreet.