Rates spark: Rate cut expectations growing

Cut expectations are growing fast in the UK, and EUR rates are taking notice. 3m Euribor dipped below the ECB depo rate as excess liquidty pressures fixings lower. For a floor, look towards €STR. The Fed is on its perceived floor though; it would take quite a significant turn lower for the economy before the Fed dipped negative.

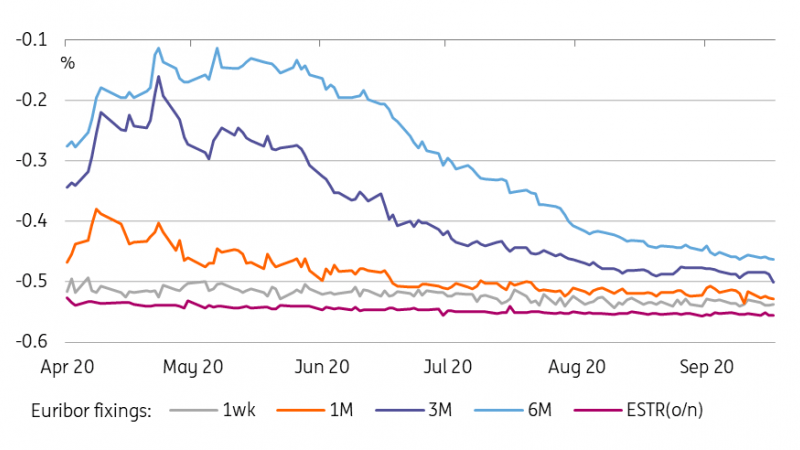

Source: EMMI, ECB, ING

Negative GBP rates: markets had already made up their mind

Yesterday’s BOE meeting is likely to leave an aftertaste beyond GBP rates. As we warned, it did not take much for the central bank’s communication to be construed as validating already high expectations of negative interest rates policy (NIRP) next year. Factually, the BOE’s communication said it is stepping up its operational readiness for negative interest rates, should they be required.

Looking at market reaction, it seems like that last part was lost in translation. The Sonia forward curve is now pricing almost 25bp of cuts by the middle of 2021. We think the abundance of downside risk to the UK economy (including the usual suspects Brexit and a second covid wave) explains in part the divergence between market pricing and BOE communication.

These same risks would likely prevent the BOE from leaning against such aggressive market pricing, so our assumption is that negative Sonia rates are here to stay. That is, at least until a trade deal is signed with the EU, or some good news materialise on the covid front. Tactically, the GBP curve steepening seen this week could be temporarily reversed if the BOE eases through QE first at the November meeting.

EUR front-end rallies further

Away from GBP, the strength of EUR 2Y was notable yesterday. It is possible that the BOE’s communication on NIRP has also landed a little bit of credibility to ECB doves talking up the odds of an additional deposit rate cut. Another factor has been the fresh drop in Euribor fixings.

3m Euribor is now fixed below the ECB’s deposit facility rate of -0.5%. However, we have stated earlier that the deposit facility rate should not be seen as the floor to Euribors but rather €STR, as banks will charge a bid/offer for the service of redepositing. €STR currently sees fixings below -0.55% with excess liquidity of almost €3tn flooding the system.

Yesterday the ECB announced that banks could deduct their holdings of deposits held at the central bank in current accounts and the deposit facility from the calculation of the leverage ratio. At the margin that may positively affect the willingness of banks to take on deposits from those without access to ECB facilities, but we believe the ultimate constraint remains “penalty” that has to be paid for redepositing at the central bank.

The Fed continues to make itself available, but is needed less

It's a stand-off now between the Fed and the rates market. The funds rate is at rock bottom, and barring the really unexpected, won't go lower. It can stay lower for longer through, which was the main theme out of the FOMC this week. Market rates continue to stubbornly range trade, with the 10yr regularly mean-reverting to sub-70bp territory.

The balance sheet data released overnight show another week of really subdued buying of corporate bonds - it remains in the USD 100m per week territory; so still little-toe-dipping. And it does not need to be more, as the corporate bond market is in rude health if primary activity and spread convergence is anything to go by.

The Fed's data show another large roll-off in Fed dollar swap lines to off-shore central banks, with a fall of some USD 17bn, bringing live swap lines down to around USD 55bn. At the height of the frantic demand for USD shorlty after the Covid crisis broke, this was up at USD 450bn. Things have clearly changed.

While the Fed's QE programme continues to add to it's balance sheet, the fall-off of other facilities mutes the rise. In consequence the balance sheet remains in the USD 7trn area. It's a relatively big balance sheet (the economy is around USD 20trn), but not as big as many had feared some months back.

The system is working, and the Fed is in the low rates business for the medium term, at the same time crossing its fingers that it does not need to do (much) more. If the BoE does dip negative, it would give the Fed pause for thought, but it would take a much more sinsiter prognosis to push the Fed there.

Today's Events: US consumer confidence, more ECB speakers

The main release today will be university of Michigan consumer sentiment.

There is another raft of ECB speakers: Hernandez, De Guidos, and Schnabel.

Read the original article: Rates spark: Rate cut expectations growing

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.