Powell's dilemma: Fed's confidence against market skepticism

Outlook: We have a specific time today to gear up for—the 11 am start of Mr. Powell’s speech.

The WSJ judgment on the Fed comments so far this week: “Fed officials are increasingly confident that they don’t need to keep raising interest rates to defeat inflation. But they aren’t satisfied enough to declare an end to hikes—let alone start a discussion about easing.” Remember that a few weeks ago, Powell said the FOMC didn’t even mention easing.

That makes Powell’s words today even more critical. He probably wishes he could pour some cold water on the party crowd. But Powell has some street smarts and may not even try-- on the grounds that the crowd won’t believe him and there’s no benefit to letting it openly diss him. On the other hand, he may want to name core services inflation as not fixed by the supply chain fix and the relatively less rate-sensitivity of the US economy (except for housing).

Powell is going to dominate the outcomes in more than one market even with other fairly big data out today—the manufacturing PMI and ISM survey, construction spending, and auto sales (amid loud talk about the American buyer having lost interest in EV). The metric is going to be any softening in the current estimate of more than 50% in favor of the first cut by the end of Q1 2024.

It’s not only the dollar getting a respite, it’s also the euro getting a sell-off. This may have a fundamental side—the presumed earlier rate cut—but also the customary pushback when a currency gets so overbought. But we have a firmer dollar against other currencies, too, like the Swiss franc and somewhat weirdly, the USD/CAD, where the daily candlestick yesterday was an engulfing bull.

The dollar pushback is a bit puzzling, since the fresh data affirmed the “let’s party” story, even if that crowd has gotten a bit drunk and is overestimating the Fed’s readiness to cut. And chances are the market won’t stay in a state of confusion for long. But here’s the problem: the US and eurozone (or at least Germany) have almost identical breakevens. See the Bloomberg chart. This is not the only measure of interest, of course, but maybe explains reluctance to move much in either direction. Oh, rats. This could mean a return to range-trading and we trend followers tend to lose out shirts when that happens. We’d rather miss a breakout and join it a bit late than cope with ranginess.

Forecast: Yesterday we said don’t count your chickens and we still think that’s the best policy. The dollar pushback is pretty strong--and widespread—but it’s still only two days’ worth and still lacking a credible trigger that would promise more to come. In other words, it can end in a nonce. It can end today if Mr. Powell decides not to tell the tide to turn.

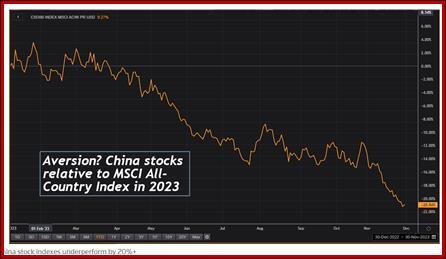

Tidbit: Today the Reuters columnist Dolan concentrates on the lousy outlook for investments in China. We recently had the drop in foreign direct investment –the first ever—by $11.8 billion in the July-September period.

Now we have “A survey by the Official Monetary and Financial Institutions Forum of 22 public pension and sovereign wealth funds managing $4.3 trillion in assets showed not one had a positive outlook for China's economy or saw higher relative returns there. Three-quarters of them cited regulation and geopolitics as chief deterrents.”

These big players prefer the US and Europe over any of the EM’s except some interest in India—and lack of interest extends to the once-favored Brazil.

Not only are they net sellers of Chinese assets, they are joined by Chinese investors. The press has them buying “Tokyo apartments and gold” to get out of town.

And the absence of the usual bottom-fishers is noteworthy. Morgan Stanley says the attitude won’t change the property sector gets repaired—and "There is no easy way out of the housing conundrum, or any deleveraging crisis: losses need to be recognised, bad debts need to be restructured and new equity support - or a bailout - might be needed to limit the scope of 'collateral damage' as some undershooting is often inevitable." So far the measures taken lack credibility.

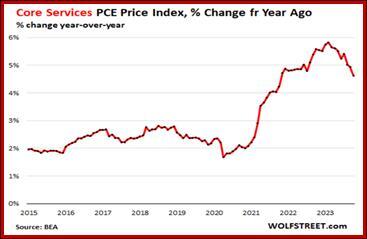

Tidbit: While the headline and core PCE prices look pretty good, Wolf Street reminds us that core services have been seesawing all year. “In August, it had decelerated to the slowest increase since 2020; in September it had spiked to the biggest increase since January; and in October, it decelerated again, increasing by 0.21%. There was a consistent deceleration earlier in the year, but the last four readings took turns spiking and dropping.” This time it’s still 4.6% y/y.

Core services exclude energy services but includes housing, insurance, healthcare, and transportation services (includes auto repair and air fares), all hot on the m/m basis. And “On a year-to-year basis most services remain in hot territory. These are the items that Powell has been talking about a lot during the FOMC press conference. This is where inflation has gotten entrenched.

Wolf Street is the only analyst focusing on core services. If you Google the term, you get zilch. Hmm.

Tidbit: As noted above, Brent oil fell $4 on the OPEC output cut of 900,000 bpd, a smaller cut than wanted and at least one country (Angola) rejecting its new quota. Bloomberg calls the talks “fractious.” This is always the problem with oligopolies—no enforcement capability.

Bloomberg also offers a partial explanation of why oil prices are sometimes so unrelated to the oil sector news—it’s those darn bot traders. Well, it had to be something like this. “An opaque group of algorithmic money managers have seized control of the oil market. Trading oil has perhaps never been more of a roller coaster ride than it is today.

“Just in the past two months, prices threatened to reach $100 per barrel, only to whipsaw into the $70s. On one day in October, they swung as much as 6%. And so far in 2023, futures have lurched by more than $2 a day 161 times, a massive jump from previous years.” The culprits are commodity trading advisors (CTAs) who are only 20% of participants in US oil, but nearly 60% of the trading volume (and they take huge positions).

Cries for more government regulation are getting louder. It was our experience as a currency CTA many moons ago that the CFTC pretty much ignores you if you are not doing something egregiously bad. And trading on algos is not forbidden.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat